Stimulus Worked

Finance & Development, December 2010, Vol. 47, No. 4

Alan S. Blinder and Mark Zandi

Without the quick and massive policy response, the Great Recession might still plague the United States

THE U.S. economy has come a long way since the dark days of the Great Recession. Less than two years ago, the global financial system was on the brink of collapse, and the United States was suffering its worst economic downturn since the 1930s. At its worst, real gross domestic product (GDP) appeared to be in free fall, declining at nearly a 7 percent annual rate, with job losses averaging close to 750,000 a month. Today, the financial system is operating much more normally, real GDP has grown by more than 3 percent during the past year, and job growth has resumed, although at an insufficient pace.

From the perspective, say, of early 2009, this rapid turnabout was a surprise. Maybe the country and the world were just lucky. But we take another view: the Great Recession in the United States gave way to recovery as quickly as it did largely because of the unprecedented responses by monetary and fiscal policymakers.

The Federal Reserve (Fed), the Bush and Obama administrations, and the U.S. Congress pursued the most aggressive and multifaceted fiscal and monetary policy responses in history. While the effectiveness and/or wisdom of any individual element can be debated, we estimate that if policymakers had not reacted as aggressively or as quickly as they did, the financial system might still be unsettled, the economy might still be shrinking, and the costs to U.S. taxpayers would have been vastly greater.

That said, almost every policy response remains controversial, with critics accusing them of being misguided, ineffective, or both. Resolution of this issue is crucial because, with the durability of the economic recovery still uncertain, there may be need for further stimulus.

Policy responses

Broadly speaking, the U.S. government set out to accomplish two goals: to stabilize the sickly financial system and to mitigate the burgeoning recession and restart economic growth. The first task was necessitated by the financial crisis, which struck in mid-2007 and spiraled into a financial panic in late 2008. After the bankruptcy of the investment banking firm Lehman Brothers, liquidity evaporated, credit spreads ballooned, stock prices fell sharply, and a string of major financial institutions failed. The second task was required because of the devastating effects of the financial crisis on the real economy, which began to contract at an alarming rate after the Lehman collapse.

The Fed took a number of extraordinary steps to quell the financial panic. In late 2007, it established the first of what would eventually become an alphabet soup of new credit facilities designed to provide liquidity to financial institutions and markets. The Fed lowered interest rates aggressively during 2008, adopting a near-zero interest rate policy by year’s end. It also engaged in massive quantitative easing to bring down long-term interest rates, purchasing treasury bonds and Fannie Mae and Freddie Mac mortgage-backed securities in 2009 and 2010. The Federal Deposit Insurance Corporation increased deposit insurance limits and guaranteed bank debt. Congress established the Troubled Asset Relief Program (TARP) in October 2008, part of which was used by the U.S. Treasury to inject much-needed capital into the nation’s banks. The Treasury and the Fed ordered 19 large financial institutions to conduct comprehensive stress tests in early 2009 to determine whether they had sufficient capital—and to raise more if necessary. The stress tests and subsequent capital raising seemed to restore confidence in the banking system.

The fiscal (that is, taxing and spending) efforts to end the recession and jump-start the recovery were built around a series of stimulus measures. Income tax rebate checks were mailed to households in early 2008; the American Recovery and Reinvestment Act (ARRA) was passed in early 2009; and several smaller stimulus measures became law in late 2009 and early 2010—such as the Cash-for-Clunkers tax incentive for auto purchases, the extension and expansion of the housing tax credit through mid-2010, the passage of a new jobs tax credit through year-end 2010, and several extensions of emergency unemployment insurance benefits. In all, close to $1 trillion, roughly 7 percent of GDP, will be spent on fiscal stimulus. We do not believe it was a coincidence that the turnaround from recession to recovery occurred in mid-2009, just as ARRA was providing its maximum impact.

The emergency measures included rescuing the nation’s housing and auto industries. The housing bubble and bust set off a vicious cycle of falling house prices and surging foreclosures, which policymakers appear to have broken with an array of efforts, including the Fed’s actions to bring down mortgage rates, an increase in limits on the size of loans that conformed to government standards, a dramatic expansion of Federal Housing Administration lending, a series of tax credits for home buyers, and the use of TARP funds to mitigate foreclosures. While automakers General Motors (GM) and Chrysler eventually went through bankruptcies, TARP funds made the process relatively orderly—and GM is a publicly traded company again.

Withering criticism

The response to the crisis sounds like a success story to us. Yet nearly all aspects of the government’s response have been subjected to intense criticism. The Fed has been accused of overstepping its mandate by conducting fiscal as well as monetary policy. Critics have attacked efforts to stem the decline in house prices as inappropriate, claimed that foreclosure mitigation efforts were ineffective, and argued that the auto bailout was both unnecessary and unfair. Particularly heavy criticism has been aimed at the two biggest programs: TARP and the Recovery Act.

The Troubled Asset Relief Program was controversial from its inception. Both the program’s $700 billion headline price tag and its goal of “bailing out” financial institutions—including some of the institutions that had triggered the panic—were hard for citizens and legislators to accept. To this day, many believe TARP was a costly failure. In fact, however, TARP has been a substantial success, helping restore stability to the financial system and end the free fall in housing and auto markets at an ultimate cost to taxpayers that will be a small fraction of the headline $700 billion figure.

Criticism of ARRA has also been strident, focusing on the high price tag, the slow delivery, and the fact that the unemployment rate rose much higher than the Obama administration predicted in January 2009. While we would not defend every aspect of the stimulus, we believe this criticism is largely misplaced. The unusually large fiscal stimulus is consistent with the extraordinarily severe downturn and the limited ability to use monetary policy once interest rates neared zero. Regarding speed, spending surged from nothing at the start of 2009 to over $100 billion (over $400 billion at an annual rate) in the second quarter—which is a huge change in a short period. (But soon the stimulus will end, with a resulting drag on economic growth.)

Critics who argue that ARRA failed because it did not keep unemployment below 8 percent ignore that unemployment was already above 8 percent when ARRA was passed (which we learned only later because of lags in the data) and that most private forecasters also misjudged how serious the downturn would be. If anything, this forecasting error suggests the stimulus package should have been even larger.

Quantifying the economic impacts

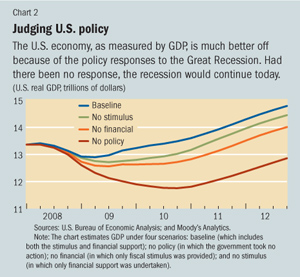

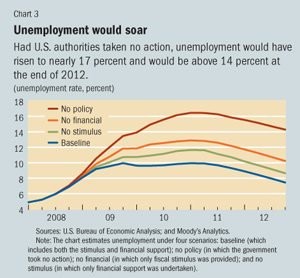

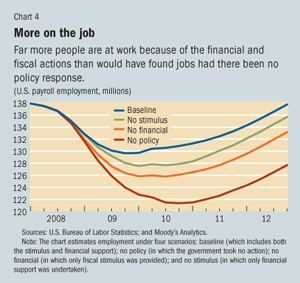

To quantify the economic impacts of the fiscal stimulus and the financial market policies such as TARP and the Fed’s quantitative easing, we simulated the Moody’s Analytics model of the U.S. economy under four scenarios:

• No. 1, with all the policies pursued;

• No. 2, which includes the fiscal stimulus but excludes the financial policies;

• No. 3, with the financial policies but without fiscal stimulus; and

• No. 4, which excludes all the policy responses.

The differences between the baseline and what would have happened with no policy response provide our central results: estimates of the impacts of the entire menu of antirecession policies. Scenarios 2 and 3 enable us to decompose this overall impact into the components stemming from the fiscal stimulus and financial initiatives. All simulations begin in the first quarter of 2008, with the start of the Great Recession, and end in the fourth quarter of 2012. The impact on the U.S. economy of the substantial policy efforts implemented in much of the rest of the world in response to the global downturn was not explicitly considered.

Estimating the economic impact of the policies is a counterfactual econometric exercise. Outcomes for GDP, employment, and other variables are estimated using a statistical representation of the U.S. economy based on historical relationships—in particular, the Moody’s Analytics model, which is used regularly for forecasting, scenario analysis, and quantifying the impacts of fiscal and monetary policies.

The modeling techniques for simulating the fiscal policies were straightforward and have been used by countless modelers over the years. While the scale of the fiscal stimulus was massive, most of the instruments themselves (tax cuts, spending) were conventional.

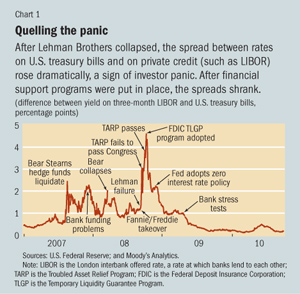

But modeling the vast array of financial policies, most of which were unprecedented and unconventional, required some creativity and forced us to make some major simplifying assumptions. Our basic approach treated these policies as ways to reduce credit spreads, particularly the three credit spreads in the model: between the three-month London interbank offered rate (LIBOR)—at which banks lend money to each other—and three-month U.S. treasury bills; between fixed-rate mortgages and 10-year U.S. treasury bonds; and between below-investment-grade corporate bonds and U.S. treasury bonds. All three of these spreads rose alarmingly during the crisis, but then came tumbling down once the financial medicine was applied (see Chart 1). The key question for us was how much of the decline in credit spreads to attribute to the policies, and here we tried several different assumptions.

The simulation results

Under the baseline scenario, which includes all the financial and fiscal policies, the recovery that began over a year ago is expected to remain intact. Real GDP, which declined 2.4 percent in 2009, expands 2.7 percent in 2010 and 3 percent in 2011, with monthly job growth averaging near 75,000 in 2010 and 175,000 in 2011. Unemployment is still close to 10 percent at the end of 2010, but closer to 9.5 percent by the end of 2011.

With no policy responses, the downturn is estimated to continue into 2011. The decline in real GDP is stunning, falling peak-to-trough by close to 12 percent—compared with an actual decline of about 4 percent. By the time employment hits bottom, some 16.6 million jobs are lost, about twice as many as actually were lost. The unemployment rate peaks at 16.5 percent. With outright deflation in prices and wages during 2009–11, this dark scenario would constitute a 1930s-like depression.

The differences between the baseline scenario and the scenario with no policy responses are huge (see Charts 2–4). By 2011, real GDP is $1.8 trillion (15 percent) higher because of the policies, there are almost 10 million more jobs, and the unemployment rate is about 6½ percentage points lower. The inflation rate is about 3 percentage points higher (roughly 2 percent instead of –1 percent). That’s what averting a depression means.

How much of this gigantic effect was due to the government’s efforts to stabilize the financial system and how much was due to the fiscal stimulus? The other two scenarios are designed to answer those questions.

We find that the financial policy responses were more important than the fiscal policies. In the scenario without them but including the fiscal stimulus, the recession would only now be winding down, the peak-to-trough decline in real GDP and employment would be about 6 percent and 12 million respectively, and the unemployment rate would peak at about 13 percent.

The differences between the baseline and the scenario with no financial policy responses represent our estimates of the combined effects of the various policy efforts to stabilize the financial system. They are very large. By 2011, real GDP is almost $800 billion (6 percent) higher because of the policies, and the unemployment rate is almost 3 percentage points lower. By the second quarter of 2011—when the effects are at their largest—the financial rescue policies are credited with saving almost 5 million jobs.

In the scenario that includes all the financial policies but none of the fiscal stimulus, the recession ends in the fourth quarter of 2009 and expands very slowly through mid-2010. The peak-to-trough decline in real GDP is over 5 percent, and employment declines by more than 10 million. The economy finally gains some traction by early 2011, but by then unemployment is peaking at nearly 12 percent.

The differences between the baseline and the scenario with no fiscal stimulus represent our estimates of the effects of all the fiscal stimulus efforts. Because of the fiscal stimulus, real GDP is about $460 billion (more than 6 percent) higher by 2010, when the impacts are at their maximum; there are 2.7 million more jobs; and the unemployment rate is almost 1.5 percentage points lower.

The combined effects of the financial and fiscal policies exceed the sum of the financial policy effects and the fiscal policy effects, each taken in isolation. This is because the policies tend to reinforce one another. As one simple example (there are many others), by holding interest rates constant, the Fed increases the fiscal multiplier.

Laissez-faire: not an option

The financial panic and the ensuing Great Recession were massive blows to the U.S. and world economies. Employment in the United States is still some 7.5 million below where it was at its prerecession peak, and the unemployment rate remains over 9 percent. The hit to the nation’s fiscal health has been equally disconcerting, with budget deficits in fiscal years 2009 and 2010 of close to $1.4 trillion. These unprecedented deficits reflect both the recession itself and the costs of the government’s multifaceted response to it.

It is understandable that the still-fragile economy and the massive budget deficits have fueled criticism of the government’s response. No one can know for sure what the world would look like today if policymakers had not acted as they did. Our estimates are just that: estimates. It is also not difficult to find fault with aspects of the policy response. Were the bank and auto industry bailouts necessary? Was the housing tax credit a giveaway to buyers who would have bought homes anyway? The questions go on and on.

Although these—and other—questions deserve careful consideration, we believe that laissez-faire was not an option. Not responding would have left both the economy and the government’s fiscal situation in far graver condition. We conclude that U.S. Federal Reserve Board Chairman Ben Bernanke was probably right when he said, “We came very close in October [2008] to Depression 2.0” (Wessel, 2009).

While TARP has not been a universal success, it was instrumental in stabilizing the financial system and ending the recession. The fiscal stimulus also fell short in some respects, but without it, the economy might still be in recession. When all is said and done, the panoply of policy responses will have cost taxpayers a substantial sum, but not nearly as much as most had feared and not nearly as much as if policymakers had not acted at all. If the comprehensive policy responses saved the economy from another depression, as we estimate, they were well worth their cost. ■

Alan S. Blinder is a Professor of Economics at Princeton University and Mark Zandi is Head of Moody’s Analytics.

This article is based on the authors’ paper “How the Great Recession Was Brought to an End,”

released July 28, 2010, and available at www.dismal.com/mark-zandi/documents/

End-of-Great-Recession.pdf

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org