Up or Down

Finance & Development, March 2011, Vol. 48, No. 1

Some have predicted postcrisis deflation in advanced economies, others high inflation. Worries about either are probably exaggerated.

ALTHOUGH the world is recovering from the global financial crisis, that recovery will likely be relatively slow in many advanced economies, with demand for goods and services in the euro area, Japan, and the United States falling short of potential supply for several more years (IMF, 2010).

Many economists and policymakers are concerned that if an economy operates well below capacity for an extended period—with accompanying high unemployment and idle factories—one consequence could be very low growth of prices and wages. Indeed, economic theory suggests that spare capacity will push down inflation rates (disinflation) or even cause overall price levels to fall (deflation). That, in turn, could extend the economic malaise as consumers, anticipating lower prices, postpone spending and borrowers suffer an increasingly heavy real debt burden.

But that is hardly a universal view. In fact, some observers have voiced exactly the opposite concern, predicting a period of sustained high price increases. They argue that any disinflationary effect from spare capacity will be overwhelmed by the inflationary consequences of the policies employed to fight the global recession. In this view, policymakers have sown the seeds of inflation by running high fiscal deficits and adopting unconventional monetary policies. The ongoing debate, then, is not so much over different cyclical assessments—most observers agree that there is still sizable slack in many advanced economies—as over the moderating impact such slack has on inflation.

To shed some light on this issue, I studied consumer price index (CPI) inflation dynamics in advanced economies during past periods in which output remained at least 1.5 percent below potential for more than eight consecutive quarters. Those situations are similar to what is thought to have occurred since late 2008 in most advanced economies. Although the historical sample can be only a rough guide to the present, it provides a broad empirical perspective on inflation outcomes during episodes of persistent large output gaps (PLOGs).

Tracing inflation

I analyzed 25 PLOG episodes in 14 advanced economies over the period 1970–2007 using data from the Organization for Economic Cooperation and Development (OECD, 2009). Among the key findings:

•There is a clear and pervasive pattern of disinflation during PLOG episodes, with the rate of inflation falling during the overwhelming majority. Moreover, in the two cases where inflation failed to decline, the increases were negligible and started from exceptionally low rates of inflation (see Chart 1).

•The disinflation appears to be supported by weak labor markets, with high and/or rising unemployment and falling nominal wages and real unit labor costs. This pattern points to the expected relationship between spare capacity and diminished cost pressures facing firms.

•In several cases, falling oil prices further helped the decline in inflation. Nominal exchange rates showed no uniform trend during PLOG episodes, but in economies with appreciating currencies, disinflation tended to be faster. Perhaps surprisingly, the growth rate of broad monetary aggregates (cash and bank deposits) appears unrelated to the strength of disinflation across episodes.

•Overall, the relationship between initial and final inflation rates seems roughly proportional, suggesting that countries with high initial rates of inflation experience greater disinflation in absolute, but not relative, terms. That finding continues to hold when we adjust for the different length of individual PLOG episodes by considering annualized changes in inflation rates.

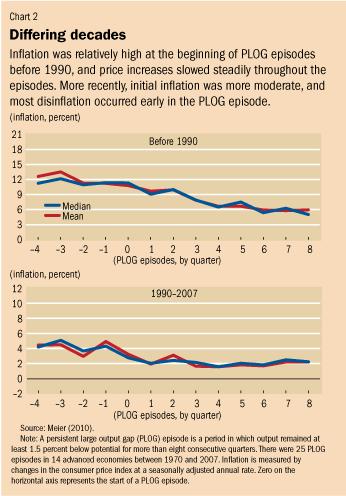

Differing dynamics

Still, the dynamics differ somewhat across time periods (see Chart 2). During episodes before 1990, which were marked by relatively high initial inflation, disinflation tended to proceed rather steadily throughout the episode. But during the more recent episodes, when initial inflation was more moderate, most of the disinflation occurred early on, followed by a bottoming-out of inflation at a new lower rate. Indeed, inflation generally stopped falling, and instead stabilized or even increased, once it had reached a low positive rate.

Why might disinflation peter out at low positive rates of inflation rather than evolving into outright deflation? Two explanations, in particular, come to mind.

First, the literature has emphasized the enhanced credibility of central banks in preserving price stability in recent years. Such credibility would be apparent not only in low average rates of inflation, but also in a strong anchoring of inflation expectations. If the public trusts the central bank’s commitment to price stability, short-term variation in the cost of production should have little effect on general price-setting behavior. The result would be a weaker relationship between output gaps and inflation in general that some studies have documented (for example, Kleibergen and Mavroeidis, 2009).

Second, disinflation might run out of steam at near-zero rates if there are strong formal or informal barriers to outright wage or price declines. Such downward rigidities appear to be common in the labor market, where nominal wages do not normally fall even during bad years (for example, Akerlof, Dickens, and Perry, 1996; and Benigno and Ricci, 2010). Labor accounts for the largest share of production costs, so any resistance to nominal cuts in wages may also explain the scarcity of sustained CPI declines in the sample. It apparently takes truly exceptional circumstances—perhaps epitomized by Japan’s experience during the past two decades—to turn disinflation into outright deflation.

What does it all mean for today?

The historical evidence points to a clear disinflationary effect from persistent large output gaps, at least until inflation has declined to very low positive rates. For countries currently facing protracted economic slack, this would suggest limited upside inflation risk. However, such a conclusion must be taken with a bit of caution, mainly for three reasons.

First, historical experience, especially from the 1970s, shows that real-time assessments of spare capacity may be subject to large revisions down the pike. Similarly, economists might be overestimating the extent of slack in advanced economies today. It is worth noting, however, that economists are keenly aware of the lessons of the 1970s. For example, typical assessments of spare capacity today allow for the possibility that the global financial crisis not only depressed demand, but also curtailed potential supply.

Second, stable relationships are scarce in macroeconomics, and even patterns reliably documented in the past might not persist. Those who worry about high inflation today often cite the exceptional policy responses to the recent crisis as a game changer. Indeed, with policy rates essentially at zero, several central banks have resorted to such unconventional policies as quantitative easing—that is, issuing central bank reserves to buy bonds (Meier, 2009). Yet it is important to recognize that there is no mechanical link between these policies and high inflation. The popular argument that more reserve money must cause runaway inflation is at odds with theory, as central banks have several tools to rein in the effect of excess liquidity. It also disregards the experience of Japan, where inflation has stayed close to zero despite massive expansions of reserve money since 2001.

Third, although PLOGs clearly appear to bear down on inflation, they are not the only influence at play. The historical pattern shows, in particular, that changes in oil prices and exchange rates can cause significant fluctuations in overall (so-called headline) inflation rates. Still, to the extent that economic slack keeps wage increases in check, higher import prices per se need not lead to generalized inflation pressure.

The most significant, if low-probability, risk concerns an extreme scenario in which unconventional monetary policy interacts with fears about high public debt to the point of undermining trust in the currency. To alleviate this risk, policymakers in many countries have already laid out plans to reduce public deficits and restore fiscal sustainability. As a result, in the period ahead, fiscal policy appears likely to support, rather than counteract, disinflation in most advanced economies. Meanwhile, inflation expectations have shown no signs of being unhinged by quantitative easing.

Recent inflation trends

With these considerations in mind, it is worth turning to the empirical evidence of the present. Indeed, actual inflation trends through the end of 2010 are not very different from the historical pattern. Applying the same criteria I used for the historical sample, I identified 15 ongoing PLOG episodes in advanced economies, based on more recent OECD data (OECD, 2010). Most of these episodes started as the global crisis worsened in the last quarter of 2008 and are expected to extend at least through the end of 2011.

Compared with the historical episodes, the decline in output is unusually large this time, although labor markets have held up better in relative terms. In fact, widespread labor hoarding—companies were reluctant to lay off workers despite the sharp downturn—initially drove up average unit labor cost in many countries, even as nominal wage growth started easing. Another striking feature is the roller-coaster ride of oil (and other commodity) prices, which first fell precipitously, but then recovered much of the lost ground. These swings had a considerable impact on headline inflation, including in recent months. Nonetheless, a general decline from precrisis rates is apparent (see Chart 3).

When food and energy prices are stripped from the CPI, the decline in inflation rates appears steadier but relatively modest. Yet this stickiness is actually consistent with the historical pattern. Core inflation started from a relatively low base in the latest PLOG episodes, at just about 2 percent on average. Since then, it has generally fallen by about 0.4 percentage point annually (or some 20 percent of the initial annual rate), matching the relative pace of disinflation in earlier PLOG episodes. Cross-sectional data confirm, moreover, that the extent of disinflation across countries remains closely correlated with the rise in unemployment.

The bottom line

Historical episodes of persistent large output gaps in advanced economies show a clear pattern of disinflation, supported by weak labor markets and low wage growth. However, declines in inflation appear to become more modest when the initial rate of inflation is already quite low, suggesting some combination of better-anchored inflation expectations and downward nominal rigidities, such as resistance to outright wage cuts. Moreover, fluctuations in oil prices and exchange rates can introduce significant short-term volatility in inflation outturns.

Developments since the beginning of the global financial crisis are consistent with this pattern. Despite large swings in headline rates, underlying inflation in advanced economies has generally declined, with many core measures reaching the very low rates at which disinflation typically petered out during past PLOG episodes. Thus, while upside inflation risks should be limited in countries facing continued economic slack, a slide into outright deflation does not seem very likely either. ■

References:

Akerlof, George, William Dickens, and George Perry, 1996, “The Macroeconomics of Low Inflation,” Brookings Papers on Economic Activity, Vol. 27, No. 1, pp. 1–76.

Benigno, Pierpaolo, and Luca Antonio Ricci, 2010, “The Inflation-Output Trade-off with Downward Wage Rigidities,” NBER Working Paper 15672 (Cambridge, Massachusetts: National Bureau of Economic Research).

International Monetary Fund (IMF), 2010, World Economic Outlook (Washington, October).

Kleibergen, Frank, and Sophocles Mavroeidis, 2009, “Weak Instrument Robust Tests in GMM and the New Keynesian Phillips Curve,” Journal of Business and Economic Statistics, Vol. 27, No. 3, pp. 293–311.

Meier, André, 2009, “Panacea, Curse, or Nonevent? Unconventional Monetary Policy in the United Kingdom,” IMF Working Paper 09/163 (Washington: International Monetary Fund).

———, 2010, “Still Minding the Gap—Inflation Dynamics during Episodes of Persistent Large Output Gaps,” IMF Working Paper 10/189 (Washington: International Monetary Fund).

Organization for Economic Cooperation and Development (OECD), 2009, Economic Outlook 86 Database (Paris).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org