Too Much of a Good Thing?

Finance & Development, September 2013, Vol. 50, No. 3

For natural resource riches to drive growth and reduce poverty, countries must balance spending now with investing in the future

Uganda discovered 3.5 billion barrels of oil in the past few years. And Mozambique recently confirmed huge amounts of coal and natural gas reserves, with further discoveries expected in the near future. Will these countries be able to reap the benefits from their newfound natural resource wealth? Or are they bound to fall prey to the same failed policies that have too often plagued other resource-rich developing countries? Those failures underscore a hard reality: without good policy frameworks, especially for taxing and spending, resource-rich countries can easily squander their natural riches. Many developing countries are endowed with exhaustible natural resources—such as oil, gas, minerals, and precious gems—that, if properly managed, could help them reduce poverty and sustain growth.

In some countries, like Nigeria, oil extraction has been a source of economic activity and fiscal revenues for several generations, while others, like Timor-Leste, rich in oil and gas, are relative newcomers to the practice. Yet others have recently discovered resources, such as Uganda, or will soon see an increase in extraction, for example, of iron ore in Guinea and Liberia. In some countries extraction will decline significantly within a couple of decades as the resource is exhausted, while in others the current rates could continue for many generations.

Natural resources are a critical component of many countries’ export and government revenues. For example, they account for an important share of total exports in nearly half of the countries in sub-Saharan Africa (IMF, 2012a). But, despite their resource abundance, these countries’ economic growth performance has been mixed.

Various arguments have been made to explain the disappointing performance in some countries with abundant natural wealth. One is that the natural resource sector chokes off other export sectors by driving up prices and undermining competitiveness (this is known as the Dutch disease effect; see “Dutch Disease: Wealth Managed Unwisely,” in F&D’s compilation of Back to Basics columns—www.imf.org/basics). Another is that the economy’s exposure to volatile prices exacerbates the difficulties of economic policymaking. Yet another explanation is that easy money from the natural resource sector creates governance challenges and could contribute to weak institutions, a risk of conflicts, and an adverse investment climate.

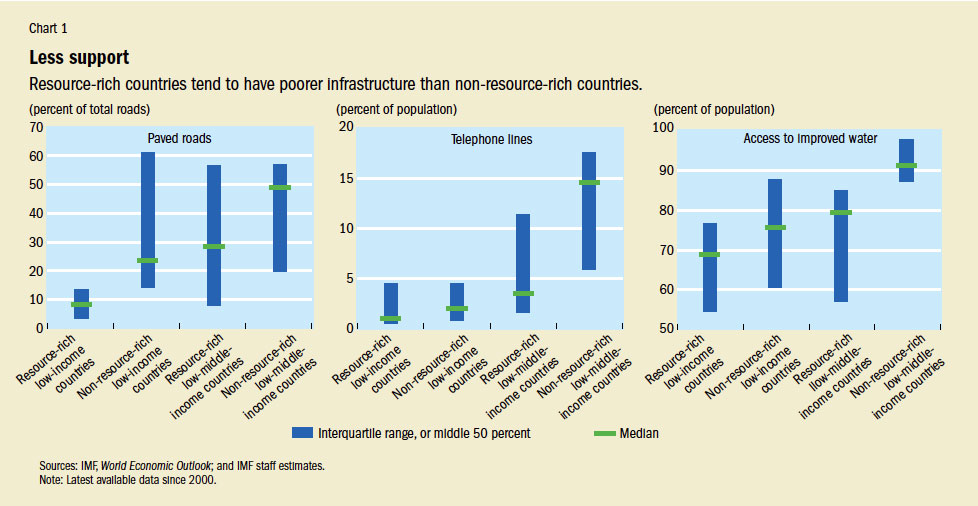

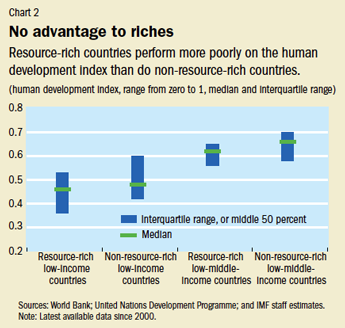

The fundamental goal of resource-rich economies should be to transform their exhaustible natural resources into assets—human, domestic, and private capital and foreign financial assets—that will generate future income and support sustained development. But the record is mixed. Several of these countries lack such basic infrastructure as roads, railways, ports, and electricity as a result of insufficient and inefficient investment spending (see Chart 1). And a number of resource-rich countries have saved relatively little of the income from their natural resources and, after adjusting for the depletion of these resources, may indeed have negative net saving rates. Partly as a result of low savings, investment, and growth, many resource-rich developing countries face endemic poverty. Indeed, they often do less well than non-resource-rich developing countries when assessed against standard poverty and other social indicators (see Chart 2).

In addition, countries that export natural resources, particularly oil, must deal with considerable volatility in export prices. The transmission of these swings to the local economy can be averted through good fiscal frameworks (such as Chile’s fiscal rule), hedging instruments, well-developed domestic financial markets, and access to international financial markets. Absent these conditions, fiscal policy tends to swing in sync with commodity prices. The result is that government revenues have, on average, been 60 percent more volatile in resource-rich countries, and spending volatility has been even greater.

Recently, however, the growth rate of natural resource exporters in the developing world has caught up with that of their non-resource-rich counterparts, reflecting the boom in commodity prices, new discoveries, and improved economic policies (see Chart 3).

Spend or save?

New approaches to resource management—using the revenues to boost domestic savings and investment, and avoiding boom-bust cycles by smoothing spending from volatile revenues—can help countries avoid the policy mistakes of the past. Recent improvements in macroeconomic management, combined with fresh analytical thinking that takes account of the specific circumstances of developing countries, offer hope that natural resource revenues can drive poverty reduction and growth.

The decision of how much of their resource revenue flow to consume and how much (and where) to save and invest saddles resource-rich developing countries with difficult trade-offs.

For advanced economies rich in natural resources, it may be optimal to save or invest resource revenues in financial assets abroad and then to consume a constant portion of resource wealth each period, equal to the implicit return (permanent income) on their total resource wealth. This is known as the “permanent-income” approach.

This approach has at times been prescribed to developing countries, even though their large investment requirements and lack of access to international capital markets for loans make it less suitable for them. For those countries, a new analytical approach to managing natural resource revenues is called for.

On the one hand, these countries’ pressing development needs, which make it difficult for them to overcome endemic poverty, call for spending more up front, including on such immediate needs as school and hospital supplies, malaria nets, and vaccination campaigns. On the other hand, to ensure sustained growth, these countries must save and invest a substantial portion of their resource revenues. Poor countries also have large unmet investment needs, and with capital scarcity come high potential returns to domestic investment. Although it may be optimal to increase current spending somewhat to alleviate pressing poverty needs, experts say poor countries should save the bulk of their resources and invest them in the domestic economy (Collier and others, 2010).

But it may be unwise for these countries to boost domestic spending rapidly because doing so could lead to macroeconomic instability. The increase in domestic demand from higher consumption and investment spending may create short-term supply bottlenecks that in turn push up domestic prices, with the inflationary pressures hurting overall competitiveness.

Ramped-up investment spending may also exacerbate bottlenecks at the microeconomic level. Weaknesses in project selection, implementation, and budgeting may make investment spending less efficient and lead to wasted resources. Therefore, a more gradual increase in spending may be advisable, with an initial focus on investing resources to remove existing bottlenecks—a process sometimes called “investing in investing”—for example, expanding teaching centers to train teachers and nurses or hiring civil service staff with the technical expertise necessary to select and manage complicated infrastructure investment projects. While this investment is under way, resource flows could be parked temporarily in external financial assets, even if the yields are relatively low.

Countries rich in natural resources also face the challenge of managing their economy when resource flows are highly volatile. Because commodity price swings can be large and long lasting, it is hard to forecast prices and decide whether to ride out changes in prices by smoothing spending or adjusting spending plans. In countries where market-based instruments such as commodity hedges are not readily available or are too costly, prudent policymakers may wish to curb spending somewhat to build up a rainy-day liquidity fund in good times that can be tapped when revenue inflows fall short. The optimal size of such a safety net is larger in countries whose resources will not be depleted for a long time (because such countries are likely to consume more of their resource revenues), where revenue volatility is greater and more persistent, and where the general public is more averse to swings in consumption. However, it may be impossible (or at least too costly, when weighed against development needs) to insulate spending fully from price swings. In practice, policymakers need to make a decision based on a tolerable degree of uncertainty (see “Extracting Resource Revenue,” in this issue of F&D).

The IMF has developed a set of tools for practical policy analysis that takes into account the specific characteristics of resource-rich developing countries (IMF, 2012b). These tools take into account the use of fiscal rules that help smooth revenue volatility and assess long-term fiscal sustainability, the impact of natural resource flows on a country’s balance of payments, and the macroeconomic implications of saving-investment scaling-up scenarios. These implications include the growth- and revenue-enhancing effects of public investment, movements in the real exchange rate—especially the real appreciation (or Dutch disease) associated with spending or investing natural resource windfalls domestically—and the effects on other key macroeconomic variables, such as private consumption, investment, and traded-sector output.

Sustainable investing tool

One tool, designed to help policymakers determine how much and how quickly to scale up public investment, is the “sustainable investing tool” proposed by Berg and others (2013). The tool takes into account the linkage between investment and growth and makes such assumptions as the rate of return on public capital.

By analyzing alternative policy scenarios for planned public investment—using both optimistic and pessimistic projections of expected resource revenues—policymakers can make more informed decisions about how to allocate those revenues between external savings and domestic investment. Because long-lasting development gains are a central policy goal of resource revenue investment, the tool can also help assess whether planned public investment is sustainable in the long run or whether it will require too much expenditure to maintain capital built with the resource revenues.

This tool captures the key macroeconomic issues facing resource-rich developing countries by weighing several factors that can undermine the growth benefits of public investment. First, it assumes that one dollar of investment expenditure can translate into much less than one dollar of installed capital if the investment process is inefficient. Second, if investment spending is ramped up too quickly, the process will be even less efficient as a result of “absorptive capacity constraints” caused by supply bottlenecks, limited management capacity, and weak institutions. Third, given that volatile flows of resource income may lead to stop-and-go investment spending, which could cause recurrent maintenance and operating requirements to suffer, installed public capital may depreciate faster and thus be less durable.

The sustainable investing tool has been applied in several countries, including Angola, Azerbaijan, Kazakhstan, Mozambique, and Turkmenistan. Although the tool is designed to capture country-specific characteristics, the results can inform general policy discussions on macroeconomic stability while countries are investing volatile resource revenues (see box for the Angola example). The purpose of the tool is to help resource-rich developing countries avoid the pitfalls of investing resource revenues and, ultimately, escape the “natural resource curse” that has plagued many resource-rich developing countries.

Opening the toolbox

In a pilot project, IMF staff used the sustainable investing tool to design a strategy that aims to close Angola’s infrastructure gap by investing its abundant oil-generated wealth (Richmond, Yackovlev, and Yang, 2013). They used two oil price projections to compare the macroeconomic outcomes of a spend-as-you-go policy, Angola’s practice before 2009, to the outcomes of a policy of more gradual investment. The results showed that when oil prices are less volatile, non-oil GDP under a spend-as-you-go policy can outperform GDP under a policy of a more gradual scaling up of investment in the short and medium term. If, however, a large negative oil price shock hits the economy—similar to that of 2008–09—both the pace of public investment and non-oil GDP growth could be seriously disrupted under a spend-as-you-go policy.

A gradual scaling up of investment gives economies with limited absorptive capacity time to improve that capacity. Meanwhile, a stabilization fund can be built up to prevent the need for sizable investment cuts when large negative oil price shocks hit. Although growth benefits are more visible when investment is increased more rapidly, the historical volatility in commodity prices means that a fiscal buffer is essential to avoid the boom/bust cycles often observed in resource-rich developing countries and to maintain steady and sustained growth in nonresource economies.

As countries like Uganda and Mozambique develop their new discoveries, they can learn from other countries’ challenges managing the volatile revenues generated from abundant natural resources. Policymakers can spur growth and fight poverty by ramping up investment spending as long as they are mindful of their economy’s capacity to absorb such investment. And spending carefully combined with saving part of resource windfalls can avert future drastic spending cuts and instability. ■

Chris Geiregat is a Deputy Division Chief in the IMF’s Finance Department, and Susan Yang is a Senior Economist in the IMF’s Research Department.

This article is based on the 2012 IMF Board paper “Macroeconomic Policy Frameworks for Resource-Rich Developing Countries,” by an IMF staff team led by Dhaneshwar Ghura and Catherine Pattillo, and on the IMF Economic Review article “Public Investment in Resource-Abundant Developing Countries,” by Andrew Berg and others.

References

Berg, Andrew, Rafael Portillo, Shu-Chun Yang, and Luis-Felipe Zanna, 2013, “Public Investment in Resource-Abundant Developing Countries,” IMF Economic Review, Vol. 61, No. 1, pp. 92–129.

Collier, Paul, Frederick (Rick) van der Ploeg, A. Michael Spence, and Anthony J. Venables, 2010, “Managing Resource Revenues in Developing Economies,” IMF Staff Papers, Vol. 57, No. 1, pp. 84–118.

International Monetary Fund (IMF), 2012a, Regional Economic Outlook: Sub-Saharan Africa, Sustaining Growth amid Global Uncertainty (Washington).

———, 2012b, “Macroeconomic Policy Frameworks for Resource-Rich Developing Countries” (Washington).

Richmond, Christine, Irene Yackovlev, and Shu-Chun Yang, 2013, “Investing Volatile Oil Revenues in Capital-Scarce Economies: An Application to Angola,” IMF Working Paper 13/147 (Washington: International Monetary Fund).

Earth's Rich Resources

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org