Extracting Resource Revenue

Finance & Development, September 2013, Vol. 50, No. 3

Philip Daniel, Sanjeev Gupta, Todd Mattina, and Alex Segura-Ubiergo

![]() Undoing the natural resource curse

Undoing the natural resource curse

For countries with abundant oil, gas, and mineral deposits, formulating tax and spending policies can be tricky

Being well endowed with resources may be beneficial for a developing country, but an abundance of resources can make it difficult for policymakers to design and implement spending and tax policies.

Authorities in these resource-rich economies must contend with several issues:

• Nonrenewable resources—including oil, gas, and minerals—are exhaustible and, as a result, so are the exports on which the countries depend.

• The prices of the commodities they export are unpredictable, so a large proportion of their revenues is often volatile, which can cause swings in government spending.

• Policy frameworks are often not strong enough to support the implementation of sound tax and expenditure (that is, fiscal) policies. The countries may have limited capacity to undertake long-term revenue forecasts and implement high-quality public investment projects.

These issues affect the design of appropriate fiscal policy, including ensuring sound decision making so that any increase in public spending is productive.

Resource horizon

Before making decisions about fiscal policies, a country’s authorities should assess the number of years that natural resources can be expected to generate revenues. Calculating a resource horizon for these extractive industries can be difficult, however, because new discoveries can be made and technological changes can affect the market value of natural resources by making them easier to extract or by increasing the portion that can be recovered.

But a reasonable estimate of whether resources are likely to be long lasting (say, for more than 30 to 35 years) is important because exhaustibility should play a key role in the determination of fiscal policy. While sustainability is an important concern for all countries, adjusting fiscal policy to an environment without resources is less of an immediate worry for those with long resource horizons. For them, the main challenge is likely to be how to manage revenue volatility as the price of the resource fluctuates. This is the case, for example, for Saudi Arabia and Russia—countries with very long resource horizons, given their enormous oil reserves. In contrast, countries whose more limited oil reserves give them a shorter resource horizon—such as Cameroon and Yemen—should focus on how government expenditures can be sustained once resource revenues end.

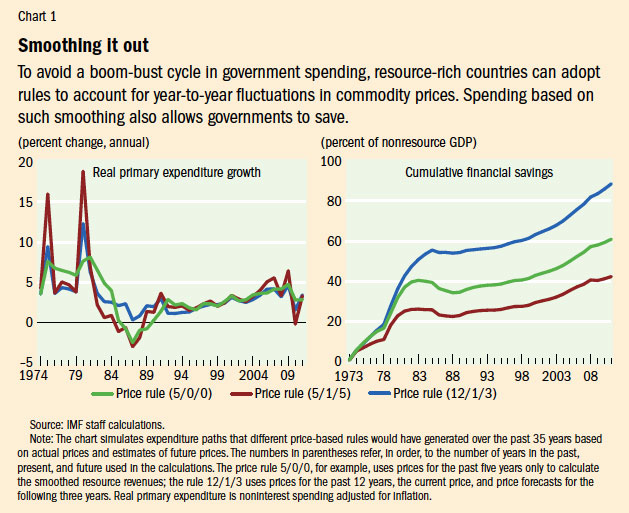

Thus, managing resource price volatility is the most important objective of fiscal policy in countries that have long resource horizons and that depend heavily on revenue from those resources. To ensure that spending and tax policies reflect long-term average revenues, the authorities can adopt rules to account for year-to-year fluctuations in resource prices. Such smoothing in estimating the structural (or normal) revenues that can be anticipated in an average year allows the authorities to determine how much of their resource revenues they can safely spend through the annual budget. Estimates of structural resource revenues use both a price-smoothing formula and production forecasts and are based on past, current, and expected future prices. Chart 1 shows how different variations of the rule (such as the number of years given to past, current, and expected prices to calculate structural revenues) produce different projections for primary expenditure growth and the accumulation of financial assets.

The choice of a price formula reflects a trade-off a country makes between a preference for smoothing expenditures and adjusting to changes in price trends. Budgets that rely on price formulas with a short backward-looking horizon will better track changes in prices, but the formulas may result in more volatile spending that could fuel an unwelcome tightening in fiscal policy when commodity prices are weak. In contrast, budgets that rely on price rules with long backward-looking formulas will have smoother expenditure paths but might systematically under- or overshoot actual revenues if the price trend changes.

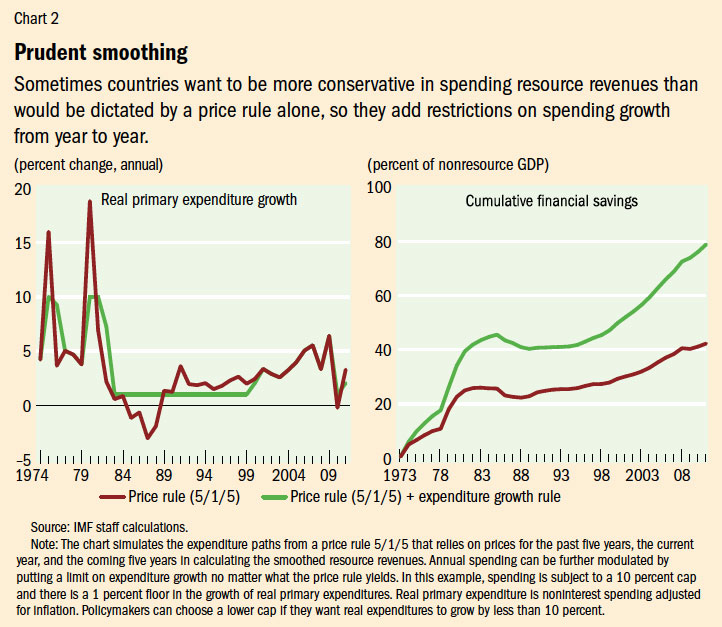

Even under smoothing rules, however, structural revenues may still jump sharply following large and abrupt changes in resource prices. For instance, the oil price spikes in 1974 and 1979 would have increased structural oil revenues by more than 15 percent with a price-smoothing rule that included forward-looking prices (such as the one represented by the red line in Chart 1). This can lead to a corresponding large increase in government expenditures despite the price-smoothing rule, which may be difficult for an economy to absorb. To control spending volatility further, the smoothing framework can be complemented by a rule that puts additional restrictions on spending growth from one year to the next (see Chart 2). The green line shows a much smoother expenditure path once this complementary rule is added.

In practice, price smoothing formulas vary. Mongolia, for example, uses a 16-year moving average of mineral prices (prices of the past 12 years and projected prices for the current and the next three years). The formula attaches a large weight to previous prices, providing stability in the revenue forecast while allowing for a gradual incorporation of forward-looking price expectations. Mexico adopts a smoothing rule based on the 10-year historical average of oil prices (25 percent weight), the short-term futures price of oil (50 percent weight multiplied by a “prudence” factor), and medium-term oil futures prices (25 percent weight). This specification is more responsive to changes in expected price trends, but the revenue forecasts it generates are less smooth. The prudence factor reduces the structural fiscal balance, which makes the rule more conservative and tamps down the spending level.

In countries with shorter resource horizons and greater uncertainty about production volumes, an alternative approach to control for resource price volatility is to base the pattern of government expenditures on a target of the fiscal balance that excludes resource revenues. The level of the nonresource fiscal balance is based on the capacity of the economy to absorb the resource revenues without causing inflation and a large current account deficit. This approach provides a direct link to fiscal sustainability by setting the target on the nonresource fiscal balance at a level that can be maintained after resource revenues run out. Because the nonresource fiscal balance gradually converges to the overall balance as resource revenues decline, calibrating fiscal policy in this way avoids the need for abrupt breaks in government expenditures or tax increases after the natural resources have been depleted. The fiscal policy design under these conditions is similar to what a country dependent on foreign aid must plan for when aid is expected to taper off in the medium to long term.

When resource revenues are higher than budgeted, the excess is saved rather than spent. Similarly, the government can draw down its financial assets when budgeted revenues are lower than expected. The fiscal frameworks in Norway, Timor-Leste, and Papua New Guinea are broadly based on this approach. In this way, governments can avoid boom-bust swings in spending driven by fluctuations in global commodity prices.

Ensuring government solvency

While sustainability issues are important for all countries, running out of resources is less of a concern in countries with a long resource horizon, because their governments are not immediately confronted with the question of whether government spending can be sustained. As noted earlier, in these countries, structural resource revenues tend to be a large and lasting share of overall government revenues. In contrast, in countries with relatively short resource horizons, it is crucial to assess how government budgets might be affected when natural resources run out and structural revenues gradually decline.

One option for ensuring sustainability is to save the resource revenues and spend only the return generated by those savings—the so-called annuity approach. In Norway, for example, the government budget every year receives about 4 percent of the value of the saved oil revenues. The approach has served Norway well, but it is not necessarily optimal for developing countries with large development needs.

One alternative to the annuity approach is to use oil wealth to buy physical assets and to improve the health care and education of citizens (in economic parlance, to invest in human capital). In countries with massive infrastructure and human capital needs, the rate of return of productive public expenditures is likely to be substantially higher than the rate of return on financial assets. In the case of infrastructure, for example, the government increases public investment for, say, 10 to 15 years by drawing down its financial savings. If the government uses resource revenues for high-quality public investment projects, economic growth is likely to increase, thereby producing an increase in nonresource revenues. Of course, this outcome requires effective public spending. If spending is poorly directed, the country and its future generations will be worse off. This underscores the importance of extensive public discourse on the choice of public projects and how they will affect growth and nonresource revenues.

The effectiveness of public investment depends on institutional factors, such as the capacity to select, implement, and evaluate projects. It is essential, then, to have strong public financial management systems, including the ability to provide reasonable forecasts of resource revenues; the capacity for medium-term budgeting; good cash and liability management; and transparency in the collection and utilization of natural resource revenues through appropriate accounting, reporting, and auditing. There is also a need for indicators to track the use of resource wealth. Two possible indicators are the share of public investment in total spending and the ratio of the increase in public investment to the increase in resource revenues.

Fiscal transparency and good governance through strong fiscal institutions should be a priority in resource-rich developing countries. Scaling up government expenditure entails a decision about the use and allocation of a country’s resource wealth. For countries to achieve fiscal transparency, it is important that they follow good practices, including a clear assignment of roles and responsibilities of different government entities, establishment of an open budget process, publicly available information, and assurances of data integrity.

Revenue policies

Revenues from extractive industries are important for financing productive expenditures on infrastructure and social spending. However, resource revenues are often disappointing in practice because the accompanying revenue and fiscal policies are not effectively designed and implemented. Recent discoveries in many developing countries, such as Ghana and Sierra Leone, lend new urgency to the design of such fiscal policies.

The policies must maximize resource revenues without creating disincentives for production. Moreover, while revenue objectives are important, other factors—such as generating employment in related activities and environmental and social effects of the industries—must also be weighed.

Still, revenue is often the main benefit to the resource-rich country, and, because investors can earn returns that far exceed what they require to stay in business (so-called economic rents), these industries are especially attractive as a potential revenue source. That is, governments can extract a large share of the economic rents, and investors will still do well.

Fiscal regimes around the world offer governments, on average, about half of the rents generated by mining, and two-thirds or more from petroleum—perhaps because petroleum usually generates more rent. Actual collections may be lower if there are loopholes or inefficiencies in collection. Fiscal policies that raise less than these benchmark averages may be cause for concern.

Governments have a variety of tax instruments at their disposal to extract resource rents, including competitive bidding, royalties, explicit rent taxes, and state participation through national resource companies. Some of the key considerations in the mix of these tax instruments are the desired timing of tax receipts; the extent to which the government wishes to take a larger share of resource rents as prices increase, which enhances revenue volatility; and the capacity to administer taxes and ensure compliance. Country circumstances vary, but policies that combine a royalty and an explicit tax on excess profits (along with the standard corporate income tax) have appeal for many developing countries. The combination ensures that some revenue (such as that from royalties) begins with the start of production and that the government’s revenue rises as excess profits increase with higher commodity prices or lower costs.

Many countries have made, or are making, major changes in the design of their fiscal approach to extractive industries, ensuring a steady flow of revenue from royalties compatible with continued investment and also targeting excess profits. Examples are Guinea, Liberia, and Sierra Leone in their mining industries.

Resource funds

As we discussed, when resource revenues are higher than budgeted, they should be saved. They could be saved in resource funds—which go by such names as sovereign wealth funds, stabilization funds, and funds for future generations. But resource funds should complement fiscal policy; their funding should come from actual fiscal surpluses and not from borrowing. They should be integrated into the broader budget process to enable governments to ensure effective resource allocation when setting spending priorities. Resource funds should not, consequently, have independent spending authority. While resource funds can have different mandates—such as stabilizing government expenditures or providing a vehicle for intergenerational savings—countries whose institutional capacity is weak should have just one resource fund.

The resource horizon and the volatility of natural resource prices influence the design of fiscal frameworks in resource-rich developing countries. Frameworks should be sufficiently flexible that they can be adapted to the varying institutional capacities and preferences of the resource-rich countries. Using the flexible framework outlined above, these countries can scale up public spending financed from rising natural resource revenues and facilitate an effective and transparent use of natural resource revenues without jeopardizing macroeconomic stability and sustainability. ■

Philip Daniel is an Adviser, Sanjeev Gupta is Deputy Director, and Todd Mattina and Alex Segura-Ubiergo are Deputy Division Chiefs, all in the IMF’s Fiscal Affairs Department.

This article is based on two IMF board papers issued in 2012: “Macroeconomic Policy Frameworks for Resource-Rich Developing Countries” and “Fiscal Regimes for Extractive Industries: Design and Implementation.”

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org