A Bumpy Road Ahead

Finance & Development, September 2013, Vol. 50, No. 3

Sebastián Sosa and Evridiki Tsounta

Latin America needs large and sustained productivity gains to maintain its recent strong growth

Latin America has enjoyed strong GDP growth in the past decade. The region grew 4 percent a year, almost twice the rate it recorded in the 1980s and 1990s. The strong growth was accompanied by declining inequality, poverty, and public debt levels. The improvement in the region’s living standards was unprecedented—in the past decade, real GDP per capita increased by more than 30 percent, about two times faster than in prior decades.

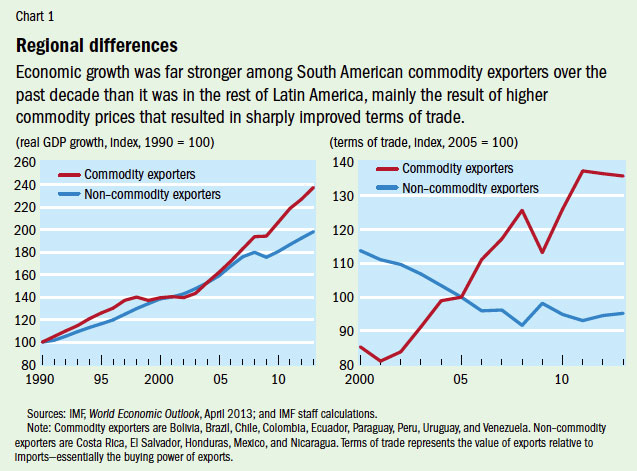

The strong growth, however, masks important differences within the region (see Chart 1). The net commodity exporters—that is, the South American countries, which exhibited increasing commodity dependence and an export base highly concentrated in primary goods—have grown, on average, 4.5 percent a year since 2003. But the rest of the region—Mexico, Central America, and the Caribbean—was much less buoyant, growing only about 2.5 percent a year.

South America benefited from an unprecedented improvement in its terms of trade because of the commodity boom of the last decade. Moreover, the financially integrated economies of this group—Brazil, Chile, Colombia, Peru, and Uruguay—which have close links to international financial markets, also benefited from the favorable external financial conditions. Large capital inflows in search of higher returns entered these countries in recent years as monetary policies in advanced economies flooded global financial markets with large amounts of liquidity.

The more northern countries, however, had stronger links to the advanced economies and were hit hard by the global financial crisis and the subsequent lackluster performance in the United States and the euro area. These links include tight commercial ties, in both goods and services (mainly related to tourism), and heavy dependence on remittances from the advanced economies. Moreover, this part of the region includes mostly net commodity importers; the surge in commodity prices added to their problems.

Cooling off

Recent data, however, suggest that growth in the region as a whole is cooling off, in some cases quite rapidly. Current conditions raise a number of questions. Is the slowdown a sign of a bumpy road ahead for the region, or is it temporary? As global financial conditions normalize and commodity prices stabilize—or even decline—will South America continue to enjoy the recent brisk growth rates, or will it revert to its past, subdued growth performance? Why have Central America, Mexico, and the Caribbean performed worse than the South American countries, and will they start to catch up?

The signs that an economic slowdown is emerging in China add to the rising concerns about growth prospects in Latin America. The region is now China’s second-largest trading partner and second-largest foreign investment destination.

A useful first step is to identify the proximate causes of Latin America’s recent strong growth performance and to estimate potential growth rates—using a simple accounting framework that breaks down output growth into the contributions from capital and labor (factor accumulation, as economists call it) and changes in productivity. Indeed, although there is a consensus that the robust growth performance in Latin America in recent years has been driven largely by favorable external conditions that fueled external and domestic demand, the main supply-side drivers are harder to identify. Has the region taken advantage of the tailwind from benign external conditions to increase its productive capacity?

Engines of growth

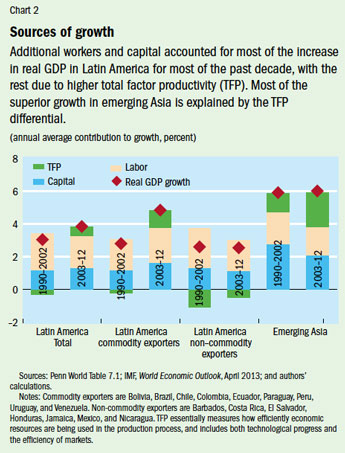

Among the commodity exporters of the region, labor accumulation has been the main driver of growth since 2003, along with growth in the capital stock (Sosa, Tsounta, and Kim, 2013). Labor and capital accumulation together accounted, on average, for 3 3/4 percentage points of annual GDP growth in the last decade, or 80 percent of the growth in output (see Chart 2).

Employment gains explain the high labor contribution to growth, consistent with near-record-low unemployment rates in many countries. The strong employment growth reflects both a cyclical increase in demand for workers as the economies grew and structural factors, including the dynamism of such labor-intensive sectors as services. Employment gains in services have been impressive, with this sector now accounting for more than half of the employed population in the region. In Brazil, for example, private employment in the services sector increased by almost 13 million between 2004 and 2012, out of a total employment increase of 16 million.

Large amounts of capital have also been flowing into South American commodity exporters amid abundant external liquidity and a tripling in commodity prices during the past decade. The financially integrated economies have benefited the most. For example, the capital stock in Chile has increased by 60 percent since the end of 2002, more than doubling in the mining sector.

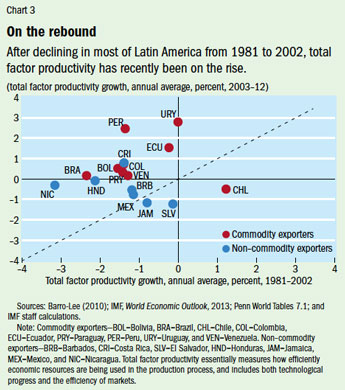

While factor accumulation has been the main driver of growth over the past 10 years, the recent pickup in output growth is explained largely by higher productivity—or, more precisely, total factor productivity (TFP)—which essentially measures how efficiently economic resources are used in the production process and includes both technological progress and the efficiency of markets. After declining in most of the region in previous decades, TFP has recently been on the rise (see Chart 3). Such a rise usually occurs during the type of good economic times that South America has been experiencing. Changes in productivity are highly correlated with changes in output.

But improvements in TFP also reflect some structural (that is, permanent) factors, such as the movement of economic activity away from the less efficient informal sector. For example, half of the salaried workers in Peru are currently employed in the informal sector, according to the Socio-Economic Database for Latin America and the Caribbean—a large decline from the early part of the century when three-fourths of total employment was informal.

Underperformers

While growth in non–commodity exporters was similar to that in commodity exporters in previous decades, non–commodity exporters underperformed in the last decade. There are several reasons for the disparity.

First, capital accumulation has been higher among commodity exporters. This reflects, in part, high local and foreign direct investment in the primary sector (mainly agriculture and mining), associated with the commodity price boom. But it also reflects the easy global financing conditions. With the exception of Mexico, non–commodity exporters could not fully benefit from these favorable foreign factors because of their limited links to international financial markets.

Second, and more important, the worse performance reflects lagging TFP in Mexico, Central America, and the Caribbean. In fact, with the exception of Costa Rica—a country with relatively strong institutions and one of the first in the region to introduce economic reforms—TFP performance in these economies has been disappointing over the past 30 years. The large informal sector, the large number of small firms, and barriers to competition—for example, in the telecommunications sector—are often cited as reasons for Mexico’s weak TFP performance (Busso, Fazio, and Levy, 2012). In most Central American countries and in the Caribbean, the absence of well-developed domestic financial markets and barriers to competition in the agriculture and electricity sectors also are at play (Swiston and Barrot, 2011).

To understand productivity growth differentials, one has to look beyond productivity in the manufacturing sector, which tends to be the focus of most studies in the literature. In fact, what differentiates labor productivity in South America from that in the rest of Latin America in the last decade is the performance of the services sector (Sosa and Tsounta, forthcoming). In the past, declining labor productivity in services dragged down all of Latin America. But in the past decade, service sector productivity has been on the rise in South America, growing three times faster than in the rest of the region. Important factors behind the better performance in South America are the decline in informality—most notably in services, which partly reflects the ease of finding jobs in the formal sector during the boom—and improvements in policies and institutions.

The challenge of sustaining growth

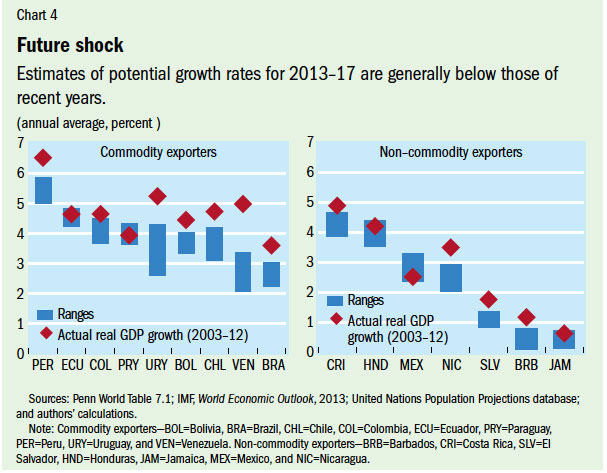

Our analysis suggests, however, that the more recent slowdown in the growth performance of commodity exporters could be more than a blip: sustaining high growth rates in these countries will be difficult. Estimates of potential growth rates for 2013–17 are generally lower than those for recent years (see Chart 4). While these economies grew, on average, at 4 1/2 percent a year during 2003–12, Sosa, Tsounta, and Kim (2013) estimate that the average potential GDP growth rate in 2013–17 will be closer to 3 3/4 percent. The growth outlook appears to be particularly disappointing for the region’s largest economy, Brazil, where GDP growth is expected to hover around 3 percent over the next few years. That projected slowdown reinforces rising concerns about a regional economic deceleration—especially because of potential spillovers to smaller neighboring economies (Adler and Sosa, 2012).

Several factors are at work in the anticipated slowdown. First, growth of physical capital is expected to moderate, as the low global interest rates that facilitated large capital flows to the region start to rise and commodity prices stabilize. In addition, the contribution of labor will likely be limited in the coming years by such natural constraints as an aging population. Record-low unemployment rates, typically well below the rates considered sustainable over the long run (known as the natural rate), also make it unlikely that employment will grow strongly in the future.

In other words, as the impact of favorable external conditions on growth dissipates and some supply constraints kick in, the strong growth South American commodity exporters experienced over the past 10 years is unlikely to be sustained unless TFP performance improves significantly. Indeed, despite its recent improvement, when compared with emerging Asia, TFP performance remains weak in these economies. In fact, most of the superior growth in emerging Asia is explained by the TFP differential.

Among non–commodity exporters, the disappointing growth performance appears to be in line with their production capacity. For these countries, potential GDP growth is estimated at an annual average of about 2 1/4 percent for 2013–17.

Significant efforts will be needed to unlock this region’s growth potential, especially policies that foster investment and productivity growth. The good news for the non–commodity exporters is that they are unlikely to be badly hurt by the fading effects of external liquidity and strong commodity prices, given their limited financial integration (with the notable exception of Mexico) and the fact that they are mostly net importers of primary goods. It is also good news that these economies are, for now at least, less constrained by population aging and have a lot of room to improve productivity levels, including by shifting resources to the more productive formal sector. However, the lukewarm growth outlook projected in the United States and the euro area—economies to which non–commodity exporters are strongly linked—will continue to affect their growth potential.

TFP to the rescue?

The Latin American and Caribbean countries could improve their growth potential by increasing domestic savings—and, in turn, investment levels, which remain low by international standards. Domestic saving rates in Latin America are less than 20 percent of GDP, compared with more than 40 percent in emerging Asia. Mobilizing higher domestic savings could, for instance, help increase investment in infrastructure—such as roads, ports, and airports. Inadequate infrastructure has constrained growth in the region. Improvements in infrastructure will not only help increase the contribution of capital to growth but will also enhance TFP. Improvements in the quality of the workforce (so-called human capital) can also increase potential growth in the region. In fact, there is ample room for improvement in the quality of education, as the region generally underperforms on standardized international tests.

But improving TFP performance will be pivotal to sustaining growth in the region. Although improvements in infrastructure and human capital would help increase productivity, by themselves they would be insufficient. Despite the recent improvements in South American commodity exporters, raising TFP has proved a challenge. Higher productivity growth is crucial, however, for the whole region and would also increase incentives to invest further in human and physical capital.

Achieving faster productivity growth entails more than fostering innovation and technological development. Low productivity has many causes. It is often the unintended result of market distortions (such as labor market rigidities that impede hiring or tax regimes that induce poor decisions) and bad policies (for example, inadequate regulation and supervision of the financial sector or unsustainable fiscal policies). These distortions weaken incentives for innovation, discourage competition, and prevent efficient allocation of resources from the less productive to the more efficient firms. Thus, designing a policy agenda to unleash productivity is a difficult task and entails country-specific measures.

The authorities should consider such policies as

• strengthening the business climate, for example, by simplifying the tax system;

• improving the enforcement of contracts and access to credit information;

• strengthening entry and exit regulation to facilitate the reallocation of resources to new and high-productivity sectors; and

• improving infrastructure.

In Central America and the Caribbean, efforts are also needed to tackle high debt levels and weak competitiveness, which are other factors behind the lukewarm growth performance there.

The road ahead will be bumpy for the economies of Latin America and the Caribbean. As the stimulus from an extraordinary external environment dissipates and some supply bottlenecks (associated with natural constraints on labor) kick in, the growth momentum in the region is unlikely to be sustainable unless TFP performance improves significantly. Thus, fostering productivity remains a key priority for the whole region: for commodity exporters to prevent a return to growth lower than they achieved in the past decade and for non–commodity exporters to overcome their historically low growth potential. These difficulties may actually open up opportunities for better policies and structural reforms that could lead to refreshingly new periods of higher economic growth and better living standards. ■

Sebastián Sosa is a Senior Economist in the IMF’s Western Hemisphere Department, and Evridiki Tsounta is a Senior Economist in the IMF’s Strategy, Policy, and Review Department.

References:

Adler, Gustavo, and Sebastián Sosa, 2012, “Intra-Regional Spillovers in South America: Is Brazil Systemic after All?” IMF Working Paper 12/145 (Washington: International Monetary Fund).

Barro, Robert, and Jong-Wha Lee, 2010, “A New Data Set of Educational Attainment,” NBER Working Paper 15902 (Cambridge, Massachusetts: National Bureau of Economic Research).

Busso, Matías, María Victoria Fazio, and Santiago Levy, 2012, “(In)Formal and (Un)Productive: The Productivity Costs of Excessive Informality in Mexico,” IDB Working Paper 341 (Washington: Inter-American Development Bank).

Sosa, Sebastián, and Evridiki Tsounta, forthcoming, “Labor Productivity and Potential Growth in Latin America: A Post-Crisis Assessment,” IMF Working Paper (Washington: International Monetary Fund).

———, and Hye S. Kim, 2013, “Is the Growth Momentum in Latin America Sustainable?” IMF Working Paper 13/109 (Washington: International Monetary Fund).

Swiston, Andrew, and Luis-Diego Barrot, 2011, “The Role of Structural Reforms in Raising Economic Growth in Central America,” IMF Working Paper 11/248 (Washington: International Monetary Fund).

IMF sees higher Latin American growth

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org