Impediment to Growth

Finance & Development, June 2016, Vol. 53, No. 2

Africa’s inadequate infrastructure limits the continent’s economic progress, but funding roads, ports, and power projects is difficult

Inadequate infrastructure—including unreliable energy, an ineffective urban-rural road network, and inefficient ports—is one of the largest impediments to economic growth in Africa. It limits the returns from human capital investment—such as education and health. Hospitals and schools cannot function properly without electricity.

A 2009 World Bank study estimated that sub-Saharan Africa’s infrastructure needs are about $93 billion a year (Foster and Briceño-Garmendia). Recently, the IMF estimated that budget spending on infrastructure by sub-Saharan African countries reached about $51.4 billion (IMF, 2014), meaning a financing gap of about $41.6 billion.

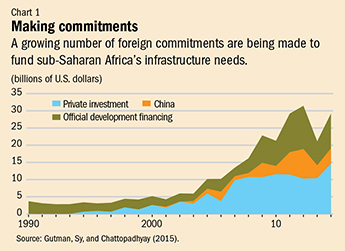

External commitments, both private and public, appear to fill a substantial share of this gap (see Chart 1). They rose to about $30 billion a year in 2012 from $5 billion in 2003 (Gutman, Sy, and Chattopadhyay, 2015). Official development financing has increased—especially from the World Bank and the African Development Bank. Private participation in infrastructure has surged and now accounts for more than half of external financing. China has become a major bilateral source of financing.

But the remaining gap of about $11.6 billion is probably too low an estimate that global assistance in any event will not fill under current circumstances. First, the 2009 World Bank calculation underestimates current needs, such as urban infrastructure. Second, the $30 billion in external commitments is not comparable to budget spending. These commitments materialize over time and do not arrive evenly. One large deal, such as a major energy investment in South Africa in 2012, can distort that year’s data. Third, overall numbers don’t tell the whole story. Of the $59.4 billion in budget spending on infrastructure by African governments, South Africa accounted for about $29 billion in 2012, with the number two country, Kenya, allocating about $3 billion. Countries also vary widely in their commitment to infrastructure spending. Angola, Cabo Verde, and Lesotho invest more than 8 percent of GDP, while oil-rich Nigeria and fragile South Sudan allocate less than 1 percent.

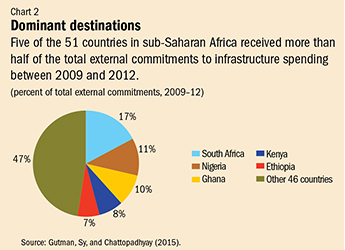

In addition, most external financing is concentrated in a few large countries and a few sectors. Five countries attracted more than half of the total external commitments to infrastructure development in 2009–12 (see Chart 2).

Except for Nigeria and South Africa, sub-Saharan African countries have been unable to attract significant private investment outside the telecommunications sector. In 2013, sub-Saharan Africa received about $17 billion in private funds, of which all but $2 billion went to South Africa and Nigeria in sectors other than telecommunications. Overall, private investment (which includes public-private partnerships) went mostly to information and communications technology and electricity from 2005 to 2012.

A policy agenda for building and maintaining infrastructure in sub-Saharan Africa under these circumstances should have at least three priorities.

First, domestic budget spending—the largest source of African infrastructure financing—should be increased. African countries generate more than $520 billion annually from domestic taxes and can mobilize more domestic revenue through improved tax administration and measures to broaden the tax base. The average tax-to-GDP ratio increased from 18 percent in 2000–02 to 21 percent in 2011–13—equivalent to half the development aid Africa received in 2013 (Africa Progress Panel, 2014). The increase in domestic financing is no doubt the result of debt relief, some increased tax revenue collection, gains from the commodity price boom, and improved macroeconomic and institutional policies.

But it will be hard for many countries to find more domestic revenue. Tax mobilization remains low despite significant effort and recent reforms in non-resource-rich countries (Bhushan, Samy, and Medu, 2013). The ratio of general government tax revenue to GDP in 2013 ranged from 2.8 percent in the Democratic Republic of the Congo to 25 percent in South Africa (one of the highest among developing economies).

Helping African countries raise more funds domestically for many purposes, including infrastructure, should be a priority for African policymakers and the international community. In 2015, global donors committed to helping African countries improve tax collection. In 2011, the latest year for which figures are available, less than 1 percent of official development assistance went to domestic revenue mobilization.

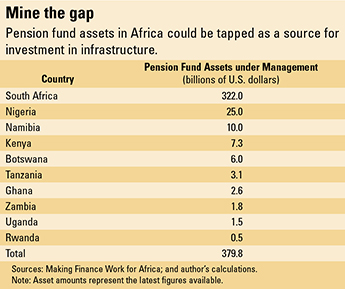

Second, sources of domestic revenue should be broadened. From 2006 to 2014, 13 countries issued a total of $15 billion in international sovereign bonds, often intending to use the proceeds to finance infrastructure. But a more prudent and sustainable way to finance infrastructure would be to increase the participation of domestic institutional investors, such as pension funds.

African pension funds have about $380 billion in assets under management, 85 percent of which are in South Africa (see table). In countries such as Cabo Verde, Kenya, South Africa, Swaziland, Tanzania, and Uganda, funds are investing in infrastructure (Inderst and Stewart, 2014). Pension fund trustees and managers should consider whether risk-adjusted investments can be made within the context of their fiduciary duty to beneficiaries. Countries must also improve the governance, regulation, and development of domestic financial and capital market instruments for infrastructure investment—and seek to attract foreign institutional investors too.

Third, funds must be spent efficiently. Most of the debate on infrastructure needs in sub-Saharan Africa focuses on financing issues. But there is evidence that efficiency, not financing, is often the barrier to investment. For example, the IMF (2015) estimates that about 40 percent of the potential value of public investment in low-income countries is lost to inefficiencies in the investment process due to time delays, cost overruns, and inadequate maintenance. Those inefficiencies are often the result of undertrained officials; inadequate processes for assessing needs and preparing for and evaluating bids; and corruption. Reducing inefficiencies could substantially increase the economic dividends from public investment.

The 2009 World Bank study estimated that if inefficiencies were addressed through such measures as rehabilitating existing infrastructure, targeting subsidies better, and improving budget execution—in other words more efficient use of existing infrastructure—the $93 billion financing need could be reduced by $17 billion. That means that the focus of attention on infrastructure should be broadened beyond financing issues to include efforts to improve efficiency. This is a complex task that requires African governments and the international community to focus on individual sectors and how they operate in particular countries and requires robust monitoring capability. ■

Amadou Sy is a senior fellow and director of the Africa Growth Initiative at the Brookings Institution.

Reference

Africa Progress Panel, 2014, “Grain Fish Money: Financing Africa’s Green and Blue Revolutions,” Africa Progress Report 2014” (Geneva).

Bhushan, Aniket, Yiagadeesen Samy, and Kemi Medu, 2013, “Financing the Post–2015 Development Agenda: Domestic Revenue Mobilization in Africa,” North-South Institute Research Report (Ottawa).

Foster, Vivien, and Cecilia Briceño-Garmendia, 2009, “Africa’s Infrastructure: A Time for Transformation,” Africa Development Forum Series (Washington: World Bank).

Gutman Jeffrey, Amadou Sy, and Soumya Chattopadhyay, 2015, Financing African Infrastructure: Can the World Deliver? (Washington: Brookings Institution).

Inderst, Georg, and Fiona Stewart, 2014, Institutional Investment in Infrastructure in Emerging Markets and Developing Economies (Washington: World Bank).

International Monetary Fund (IMF), 2014, Regional Economic Outlook: Sub-Saharan Africa—Staying the Course (Washington, October).

———, 2015, “Making Public Investment More Efficient,” IMF Staff Report (Washington).

Opinions expressed in articles and other materials are those of the authors; they do not necessarily reflect IMF policy.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org