Bretton Woods to Brexit

Finance & Development, September 2017, Vol. 54, No. 3

The global economic cooperation that has held sway since the end of World War II is challenged by new political forces

The British vote to leave the European Union and the election of Donald Trump as president of the United States have brought a new style of politics—not just in the United Kingdom or the United States, but for the world. The developments of 2016 constitute a major challenge to the liberal international order constructed after the defeat of Nazism in 1945 and strengthened and renewed after the collapse of the Soviet system between 1989 and 1991.

The United States and the United Kingdom were the main architects of the post-1945 order, with the creation of the United Nations systems, but they now appear to be pioneers in the reverse direction—steering an erratic, inconsistent, and domestically controversial course away from multilateralism. Other countries, meanwhile, for various reasons are incapable of assuming that global leadership, and the rest of the world likely would not support a new hegemon in any event.

The postwar system created at the Bretton Woods, New Hampshire, conference in 1944 should be credited with economic growth, a reduction in poverty, and the absence of destructive trade wars. It built a comity that encourages to this day cooperation on issues as diverse as taxation, financial regulation, climate change policy, and terrorism financing.

The central postwar concern was international financial stability. The United States and the newly created International Monetary Fund were at the center of a system that sought to maintain that stability by linking exchange rates to the dollar, with the IMF the arbiter of any changes. But today exchange rates are largely set by market forces; the IMF has morphed into a combination of crisis manager, global economic monitor, and policy consultant; and US dominance may be replaced by new powers, such as China and the European Union, even as domestic political forces seem to be tugging the United States away from international engagement.

What changes are needed to adjust today’s world to the changed geography of economic development, to a transforming geopolitical environment, and to large and potentially unstable financial flows?

In 1944 and 1945 a multilateral liberal world order was built, largely at the initiative of, and in accordance with, the perceived interests of one power: the United States. Forty-four countries were formally present at Bretton Woods, but US and British policymakers steered the negotiations. The essential vision involved multilateralism that benefited everyone. The Soviet Union, which participated in Bretton Woods, did not ratify the agreement, in part because it was suspicious of the American motivation, and in part because it did not want to supply the data that was a requirement of membership in the IMF.

Endless imbalances

How countries adjust when they spend more on foreign purchases than they earn from abroad was particularly contentious—and the debate about international order was shaped by lessons drawn from the unsuccessful attempt to create a stable order after World War I, when pressure on deficit countries to adjust produced harmful worldwide deflation and then depression. The IMF was devised to prevent currency wars and competitive devaluations, which had been the 1930s’ response to deflation.

Most countries in 1944 and 1945 could reckon that they would import more than they would export for a long time and that the United States would have semipermanent trade surpluses. That’s because the United States was not only a major supplier of food for a world ravaged by war, it was also the only really substantial producer of a wide range of engineering and machine tool products since industrial capacity in Germany and Japan was destroyed. That meant that most countries would have to scramble to come up with enough dollars to buy needed imports.

The grand compromise reached by delegates to Bretton Woods appeared evenhanded: a country could be deemed to have a “scarce currency”—the US dollar—and the United States would accept full responsibility if there was a “fundamental disequilibrium.” Other countries would then be allowed to impose trade and exchange restrictions to reduce exports from the country with the currency that was misaligned.

But in practice, the voting arrangements of the new IMF gave the United States the power to block a hostile decision as to whether dollars were in fundamental disequilibrium or “scarce” when other countries couldn’t get enough of them. Moreover, by the 1960s, the feared US surpluses had disappeared, and even before that so had worries about new permanent and pernicious world deflation. That’s because the United States recycled its surpluses through military expenditures and foreign direct investment, which allowed much of the rest of the world to catch up.

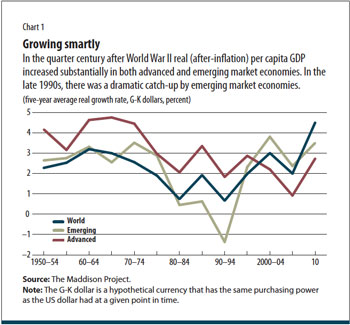

Overall, the first 25 years after Bretton Woods were generally benign: US-inspired multilateralism helped everyone. There was growth, stability, and catch-up. In the Bretton Woods period, all countries grew. In the late 1990s, in the new era of globalization, there was a dramatic catch-up by emerging market economies (see Chart 1).

In France, the postwar decades are usually called the 30 years of glory. But 30 is an exaggeration. Things looked shaky by the late 1960s for the global financial system. The mechanism of generally fixed but adjustable exchange rates collapsed between 1971 and 1973. The world experienced an inflationary surge with unstable capital flows, and democracy and political stability were threatened.

New issues for multilateralism

Multilateralism was inventive, though, in dealing with the new issues. The leading industrial countries in 1975 (France, Germany, Italy, Japan, United Kingdom, United States) convened at Rambouillet, France. It was the ancestor of modern Group of Seven (G7) summits, which added Canada in 1976 (and indirectly of the broader Group of 20)—and successfully dealt with inflationary developments and the political challenge that came when oil prices skyrocketed after the Organization of the Petroleum Exporting Countries cut production in 1973 following the Arab-Israeli war. Influential voices in the United States initially pushed for a military solution to the oil cartel’s challenge. But advanced economies ultimately adopted an alternative vision, largely driven by US Secretary of State Henry Kissinger, using private flows of money to bring the oil producers into the system. That achieved political stability, but at the price of financial volatility generated by very large capital flows as oil producers deposited in large multinational banks their massive profits, which the banks then lent to countries to enable them to pay the higher oil price.

The IMF developed new financing facilities for developing economies hit by the higher oil prices and the recession they caused. But when bank-driven capital flows stopped—first for particular countries and then in a general Latin American debt crisis in 1982—the IMF embarked on a new life. No longer was it the overseer of fixed exchange rates; it morphed into a crisis manager, coordinating rescue operations that depended on IMF loans, country reform programs, and new money from the lending banks.

Multilateralism was also at the core of managing a cautious, rule-bound, and fundamentally orderly transformation of formerly state-planned (Soviet-style) economies in the 1990s. The 1990s, and the evident failure of central planning, also marked a turning, in that multilateral institutions realized that in the middle of a complex political and social upheaval, it was important to speak to a wide range of interests: opposition parties, trade unions, civil society groups. Other issues apart from purely economic ones started to be central to multilateral efforts, such as the quality and effectiveness of government and the level of corruption and transparency.

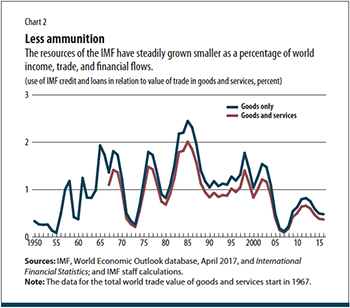

The results of the changes are ambiguous: the surges of private capital flows contributed to substantial growth, a redistribution of the geographical focus of economic activity, and the lifting of billions of people out of extreme poverty. But capital-driven globalization was also volatile and unstable, and the resources of multilateral institutions appeared smaller in relation to world income, trade levels, and financial flows than in the earlier era (see Chart 2).

Asian crisis

The major intellectual challenges to reconfigured and decentralized multilateralism occurred with the Asian crisis in 1997–98 and then, in a different form, in the response to the global financial crisis that began in 2008 and hit the old rich industrial countries, in particular Europe, especially hard. The outcome of the Asian crisis was interpreted widely in crisis countries, but also by some influential economists and theorists in the United States, as the imposition of US views and US interests. In one interpretation, the severity of the crisis that followed from a sudden stop of capital market flows, and the imposition of adjustment programs, allowed Western institutions to acquire significant holdings in a dynamic region at bargain basement prices. At the beginning of the crisis, Japan had pushed for an Asian Monetary Fund, but that idea was killed by US opposition.

Some large Asian countries decided that they never again wanted to be dependent on the IMF and moved to self-insure by building up foreign exchange reserves—which required large current account surpluses. The logic of this argument created a good cover story for a mercantilist export promotion drive that depended on countries holding down the value of their currencies by fixing (or pegging) their currencies, usually to the dollar. As current account imbalances soared, the structural flaw that had dominated the Bretton Woods negotiations reemerged: large current account surpluses, this time mainly for oil exporters and China, and, in a turned table, large deficits in the United States and some other industrial countries.

China also pushed for the creation of regional facilities to support countries with balance of payments and other problems—both as a version of the original Asian Monetary Fund proposal from the 1990s and as a substitute for the global institutions. The Chiang Mai Initiative started in 2000 with a series of bilateral swap arrangements between 10 southeast Asian countries plus China, Japan, and South Korea that allowed a country in need of a foreign currency to borrow it from another member of the initiative (though there have been no swaps yet). The 2008 global crisis intensified the regional push: in 2010 the Chiang Mai arrangements were enhanced, and new institutions began, notably the New Development Bank (popularly called the BRICS bank) in 2013 and the Asia Infrastructure Investment Bank in 2016.

Some lessons emerge from the increasingly decentralized governance of the international system. Each major challenge—the 1970s inflation and oil price shocks and the recent global crisis—produced some new approaches to multilateral cooperation and coordination: the G5 in 1975 and the G20 advanced and emerging market economies in 2008. In each case, however, a productive initial meeting was followed by a process of routinization that sapped the urgency and the capacity to generate major breakthroughs and policy improvements.

Each big challenge also produced regional initiatives aimed at financial and economic governance. The European Monetary System, an attempt to build a regional Europeanized version of the Bretton Woods system, was a response to the currency chaos of the 1970s. The Asian crisis led to a move for greater Asian integration. In Europe, the European Stability Mechanism, created in 2012 to fund EU interventions in member countries in crisis, is also likely to develop into a European Monetary Fund.

The buildup of the proliferation of regional answers raises the question of how regional and global institutions can work together effectively. One long-standing objection to a world based on regional arrangements was that it would be helpless in the face of impacts or spillovers from one area to another: the Asian crisis for instance spread to Russia and Brazil. Another problem involves countries on the periphery of regional blocs that feel increasingly vulnerable. How then can nations coordinate the interaction between the provision of financial facilities—where regional resources are increasingly important—and the design of policy, which has global ramifications?

Design questions

There were three distinct ways multilateral governance institutions operated in the era of postwar stability. The first was in a judicial or quasijudicial role in arbitrating disputes between countries. There are many cases that look as if they require arbitration: trade disputes and—often associated with trade disputes—whether currencies are unfairly valued to produce a subsidy for exporters.

The new emphasis on sovereignty—in the United Kingdom and elsewhere in Europe where “sovereignists” confront “globalists”—pushes back against this type of arbitration. In the past, the United States has used the World Trade Organization’s dispute settlement mechanism to justify keeping trade open.

Currency misalignment was a much more difficult issue for international settlement, and in the most important cases—with Japan in the 1980s and China in the 2000s—the IMF backed away from formal declarations that a currency was deliberately undervalued.

The second style of multilateralism involved institutions acting as sources of private advice to governments on policy and on the interplay between policy in one country and in the rest of the world: explaining and analyzing feedback and spillovers and offering policy alternatives. That sort of consultation—rather than a formal arbitration procedure—was the main vehicle for discussion of currency undervaluation issues in the 2000s. The essence of this kind of advice is that it is private. The outcome may be changes in behavior or policy but the outside world will not understand the reason or the logic that compels the better behavior.

The third was as a public persuader with a public mission. Former British Prime Minister Gordon Brown liked to use the phrase “speaking truth to power” with regard to the advice of multilateral institutions, such as the IMF or World Bank. There is increasing recognition of the limits of secret diplomacy and behind-the-scenes advice. Societies cannot be moved without genuine consensus that they are moving in the right direction. The backlash against globalization is fed by a climate of suspicion: experts, economists, international institutions are not trusted. During the 2000s, the G20 and the IMF moved to public assessments of how policy spillovers affected the world—and in particular examined the multilateral dimensions of trade imbalances and their various causes, including monetary policy stances and structural and demographic developments.

This public style of action looks more appropriate in an age of transparency—when information technology seems less secure, when secrets leak, when WikiLeaks flourish. Today it is unwise to assume that anything is secret.

The accessibility of information presents a fundamental dilemma. Policy advice is invariably quite complicated. Spillovers and feedback require a great deal of analysis and explanation and cannot easily be reduced to simple formulas.

Accessible information

Should international institutions be more like judges, or priests and psychoanalysts, or persuaders? The traditional roles by themselves are no longer credible. But multilateral institutions will also find it impossible to take on all three roles simultaneously. Judges do not usually need to embark on long explanations as to why their rulings are correct. If they act as persuaders, maintaining a hyperactive Twitter account, they merely look self-interested and lose credibility. But if they are secretive—like the World Bank’s International Centre for Settlement of Investment Disputes—they may be more efficient (as measured by the gains from their rulings) but will lose legitimacy.

It is easy to see why the institutions that built the stability of the post-1945 order might be despondent in the face of apparently insuperable challenges. It is hard to apply fundamental and widely shared principles such as human dignity and sustainability to the minutiae of policy. But the institutions might harness the new technologies to successfully mediate disputes that threaten to divide but also to impoverish the world.

In the postcrisis world, ever larger and more updated amounts of data are available. In the past, we had to wait months or years for accurate assessments of the volume of economic activity or trade. Data on a much broader set of measurable outcomes, including measures of health and economic activity, are now available in real time. Managing and publishing those data in accessible and intelligible ways can be critical to forming the debate about the future and about the way individuals, societies, and nations interact. Instead of a judge, multilateral institutions can become purveyors of the costs and benefits of alternative policies. They need to work on ways of letting data speak.

Some of the issues to be addressed are new, or appear in new forms, and are global public goods: defense against diseases that spread easily in an age of mass travel, against terrorism, against environmental destruction. In each case, the availability of large amounts of detailed information, available quickly, is essential to coordinate an effective response: for instance, where there is pollution and how it affects health and sustainability and where and why it originates. Even large countries cannot find the right response on their own.

Some of today’s problems were already identified at Bretton Woods: How can countries avoid unsustainable current account deficits, which make them vulnerable to shocks and reversals of confidence on the part of capital markets? How can large surpluses that impose a deflation risk on the rest of the world be reduced? Regional agreements cannot find an answer to these problems. Simple global answers are also impractical and unlikely to sustain consensus. Instead, large amounts of data hold the key to effective action, identification of precisely how the financing of external imbalances is achieved, and the circumstances that make a major external imbalance harmful and destabilizing. Much more than in 1944 and 1945, governance will depend on information.

HAROLD JAMES is a professor of history and international affairs at Princeton University and IMF historian.