Choosing Exchange Regimes in the Middle East and North Africa Creating Employment in the Middle East and North Africa Financial Development in the Middle East and North Africa GCC Countries: From Oil Dependence to Diversification The Middle East and North Africa in a Changing Oil Market |

|

|

|

Challenges of Growth and Globalization in the Middle East and North Africa

George T. Abed and Hamid R. Davoodi © 2003 International Monetary Fund [Preface] [Economic Performance in the MENA Region] [Factors Affecting the Region's Performance] [The Urgency of Reforms] [Bibliography] PrefaceThe Middle East and North Africa (MENA) is an economically diverse region that includes countries with a common heritage, at various stages of economic development, and with vastly different endowment of natural resources. Despite undertaking economic reforms in many countries, and having considerable success in avoiding crises and achieving macroeconomic stability, the region's economic performance in the past 30 years has been below its potential. The purpose of this pamphlet is to take stock of the region's relatively weak performance, as measured by rate of growth, links to the global economy, and employment generation; explore the reasons for this outcome; and propose an agenda for urgent reforms. The authors would like to thank Susan Creane for her comments and suggestions, other colleagues in the Middle Eastern Department of the IMF for valuable comments on earlier drafts, Heather Huckstep for administrative support, and Brett Rayner for research assistance. The authors bear the sole responsibility for any remaining errors and omissions. |

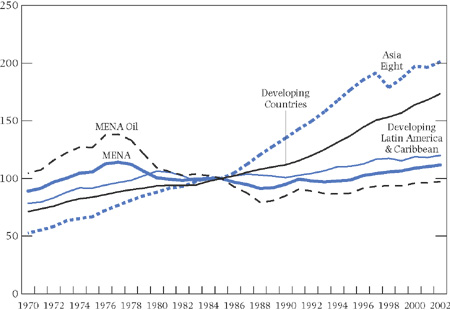

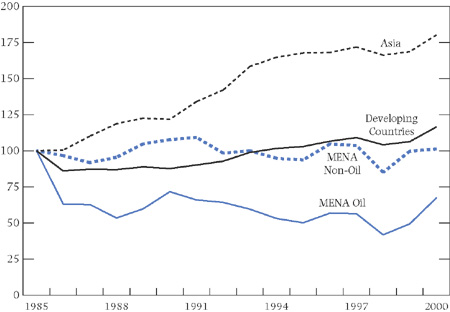

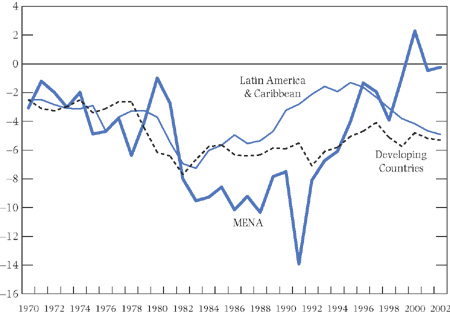

The Middle East and North Africa (MENA) is an economically diverse region that includes countries with a common heritage, vastly different levels of per capita income, and a common set of challenges (see Box 1). Historically, dependence on oil wealth in many countries and a legacy of central planning in other countries have played major roles in shaping the region's development strategies. The MENA region benefited immensely from the wealth created by the sharp increase in oil prices in the 1970s. The explosion of investment and growth in the oil-exporting countries resonated in other countries of the region through a sharp rise in worker remittances, trade, and capital flows. Gross capital formation, although volatile, was maintained at exceptionally high rates, supporting a strong increase in growth rates of GDP and a vast improvement in living standards. Substantial financial assets were accumulated abroad as national savings exceeded investment, especially in the oil-producing countries. However, the region's economic performance during the next 20 years weakened as growth rates declined and failed to generate the employment opportunities sought by a rapidly expanding labor force. This deterioration in economic conditions brought about pressures for economic reforms, which were undertaken by a number of countries during the mid-to-late 1980s and early 1990s. Fiscal reforms included introducing value-added tax (VAT), phasing out subsidies, and improving management of public expenditure. Monetary policy frameworks were strengthened by introducing indirect monetary policy instruments. Trade regimes were liberalized and foreign direct investment (FDI) was encouraged while exchange rates became more flexible. In subsequent years, the countries that pursued reforms, such as Egypt, Jordan, Mauritania, Morocco, and Tunisia, enjoyed the region's most rapid growth rates. Although the momentum for reform has slackened more recently, other macroeconomic outcomes have remained positive in much of the region. For example, inflation has been low and on the decline for most of the 1990s; fiscal deficits, while persisting, have narrowed since the mid-1980s to levels below those of other developing countries. Financial crises, which plagued other regions during the past two decades, were averted. In addition, for a large number of countries in the region, external and domestic debts are not high by international standards, and debt service is low. In sum, while macroeconomic stability was maintained, the MENA region as a whole failed to generate high and sustained growth rates. In contrast to other developing countries, the region underperformed since the 1970s and, as a result, did not reap the full benefits of globalization and world economic integration. In what ways, then, is the region's growth performance during the past three decades different from that of other developing countries? The experience of the last 50 years across wide regions of the globe has shown that developing countries, on average, have found it much easier to initiate growth than to sustain it. In this regard, the MENA countries' experience is not unique. What is unique is the extent to which growth rates since the 1970s have been volatile and low relative to other developing countries. Volatility of real per capita GDP growth in the region has been twice that of developing countries' average. In the oil-producing countries, the real per capita GDP growth rate (hereafter referred to as growth) was twice as volatile as in the non-oil economies. Of greater concern is the region's near-zero percent growth rate during the past 30 years, when all other developing countries as a group grew at 2.5 percent per annum. Even as economic performance in the region improved in the 1990s, the region achieved an annual average growth rate of only 1.3 percent, compared with an annual average of 4 percent for all developing countries. A major consequence of this poor record is persistent high unemployment, which has been reinforced by years of high growth rates of population and labor force. Employment in the MENA region did grow, at times faster than in other developing countries, but rapid population growth inflated the ranks of the young and fed the labor market with a rising tide of job seekers that exceeded the economies' capacity to absorb them. Linked to the region's record on growth and employment is its weak integration into the global economy. The experience accumulated to date indicates that economies that, over extended periods, embrace openness and globalization tend to grow faster than those that adopt inward-looking growth strategies. And, in this regard, the performance of the MENA region has fallen short, depriving many countries of reaping the full benefits of globalization. The challenges facing the region are daunting. The MENA countries' economic performance remains below its potential, giving rise to chronic unemployment and poor living conditions in large parts of the region. Countries in the region must achieve higher rates of sustainable growth and integrate more fully into the global economy if they are to succeed in creating meaningful employment for a rapidly rising labor force and, more generally, reduce poverty and improve living conditions. In this pamphlet, we take a closer look at economic performance in the region, particularly with respect to growth, unemployment, and global integration, followed by an exploration of possible reasons for the weak performance. In conclusion, we outline the reforms needed to improve the region's economic performance. Economic Performance in the MENA RegionGrowthReal per capita GDP growth in the MENA region during the last 30 years has virtually stagnated compared to the rest of the developing world (Figure 1). In part, this reflects the extended weakness in the oil markets as producers outside of the MENA region gained market share at the expense of oil exporters in the region. In addition, the region's high population growth dragged down the rate of growth of per capita GDP. Within the region, the contrast in the growth experience of the oil and non-oil economies is striking. On the one hand, in the last 30 years, per capita income in the oil-producing countries declined at a rate of 1.3 percent per annum, compared with an increase of 2 percent per annum in the non-oil economies. Even during the booming 1970s, oil-producing countries grew, in real per capita terms, at about half the rate of non-oil-producing countries in the region. Again, much higher rates of population growth in the oil-producing countries, among other factors, pulled down per capita growth rates. On the other hand, non-oil economies, enjoyed positive growth rates over the last 30 years, matching those of developing countries in the 1970s and 1980s. It was only in the 1990s that growth in the non-oil economies (at 1.5 percent per annum) fell short of the average for developing countries more generally (at 4 percent per annum). In addition to differences in growth volatility and demographic dynamics, the oil-producing countries seem to have experienced what has become known as the "resource curse." An abundance of natural resource wealth can lower growth by, among other things, generating an appreciation of the real exchange rate resulting from large oil-related foreign exchange inflows, thus making non-oil exports less competitive and shrinking the relative size of the non-oil export sector. Aggregate economic growth in oil-producing countries continues to be dominated by developments in the oil sector. In many of the larger oil economies, oil and other hydrocarbon products, on average, account for 75 percent of total exports. The non-oil sectors, on the other hand, have yet to generate sustained growth high enough to absorb the growing numbers of entrants into the labor force. Volatility and low growth in several of the oil economies are aggravated further by highly procyclical fiscal policy as government spending tends to rise and fall with oil revenue. This is, in part, because of the absence of effective automatic stabilizers, which could cushion the severity of economic fluctuations. Some of the region's oil-producing countries, such as the Islamic Republic of Iran, Kuwait, and Oman, have addressed this procyclicality by establishing oil and stabilization funds (OSF) that save part of the oil receipts abroad, in effect, sterilizing foreign exchange inflows. Other oil-producing countries in the region have chosen not to establish formal OSFs with precommitted fiscal rules, but have tended to conduct fiscal management with a "virtual" OSF that, in effect, invests the excess oil receipts abroad. UnemploymentEconomic growth and job creation are closely linked. They form a nexus that is an important part of any strategy to alleviate MENA's high and persistent unemployment, given the predominance of the young population in the region and its high unemployment rate (currently in excess of 15 percent in a number of countries in the region). Keller and Nabli's 2002 World Bank study of 16 MENA countries, representing about 60 percent of the population in the entire region, shows that up to 47 million new jobs would need to be created between 2002 and 2012 merely to keep pace with new entrants into the labor market. An additional 6.5 million jobs would be needed to reduce the unemployment rate to just below 10 percent. The outlook for employment generation in the MENA region as a whole becomes even more challenging in the face of the widespread unemployment in the post-conflict states of Iraq, the Islamic State of Afghanistan, and the West Bank and Gaza. These three economies have a combined estimated population of 53 million, with unemployment rates that are well in excess of those in the rest of the region. Of course, employment growth depends not only on output growth but also the elasticity of employment with respect to output, that is, the employment intensity of such growth. Assuming a relatively high elasticity of 0.7, the required employment growth for the 16 MENA countries rests on generating sustained annual growth of real output of about 6 percent over the next 10 years, some 2 percentage points above the recent trend for the region. Only two countries, Qatar and Sudan, have achieved 6 percent or higher average rates of real GDP growth over the last five years. Global IntegrationCommon measures of globalization illustrate the MENA region's relatively weak integration with the world economy. The region receives only one-third of the FDI expected for a developing country of comparable size, and most is concentrated in a handful of countries. Portfolio investment is virtually nonexistent because of the poor state of development of equity markets. Global financial integration lags behind that of other developing countries. The number of MENA countries adhering to IMF Article VIII provisions, which generally signifies full current account liberalization, is proportionally lower, at one-third of the total, than in other regions. The MENA region's trade performance is also below that of other regions: although oil exports continue to be a substantial source of foreign exchange earnings for oil producers, the relative importance of such exports has declined since 1985 (Figure 2). Non-oil export growth varied during this period but, on the whole, grew at a slower rate than for all developing countries. As a result, the MENA region's share in the world export market fell by more than half in the 20-year period between 1980 and 2000. Developing countries' share of the world market rose slightly during the same period. Moreover, the region's information and technology links are among the weakest in the world. Although the number of Internet users is growing in the region, it has remained low by international standards.

Factors Affecting the Region's PerformanceClearly, there are risks in making generalizations about the growth performance of the region as a whole because each of the 24 economies has had its own experience, which in some ways remains unique. Differences also arise between oil producers and non-oil producers in the region and between countries that undertook reforms, and hence grew at higher rates, and those that were less vigorous in pursuing reforms and fell behind. Nevertheless, the economic structures and institutions of the MENA countries do tend to exhibit common features and, given the need for a policy focus on the challenges and opportunities that face the region, there is a strong case for treating the region as a unit of analysis. However, the variations, the differences, and the distinctions between countries, which are relevant to the arguments being made, must always be highlighted. With this caveat, and viewing the MENA region as a whole, one may attribute the region's weak economic performance to the following possible reasons, most or all of which are interrelated and characterize each country to varying degrees:

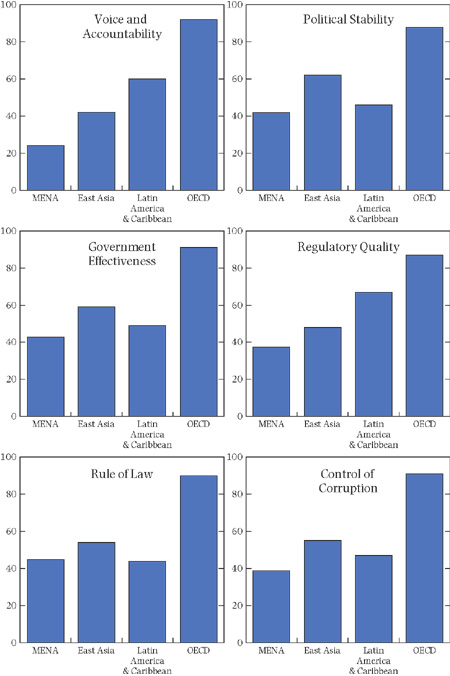

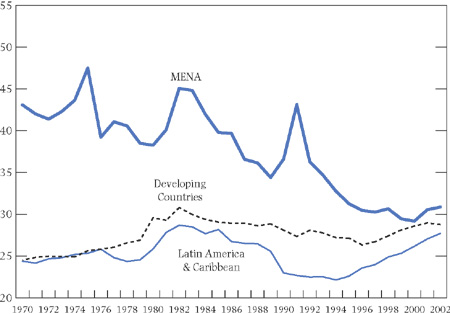

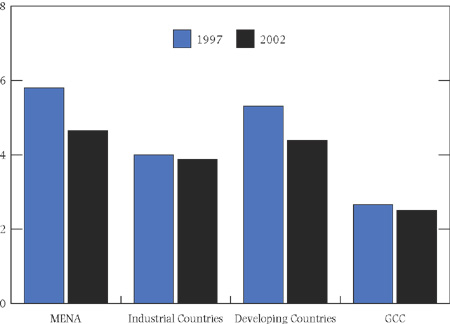

High Population Growth and Low ProductivityHigh population growth. With a 2.5 percent annual increase over the past 20 years, the MENA region has had one of the highest rates of population growth in the world, close to that of sub-Saharan Africa. Although population growth in the MENA countries is projected to decline to 1.5 percent over the period 2000–15, this rate is still high, and would no doubt remain a factor in the slow growth prospects for real per capita GDP. In the 1970s and 1980s, annual population growth rates in the oil economies exceeded those of non-oil economies by 2 percentage points. Although the rates in these subgroups converged by late 1990s to about 2.5 percent, they remained quite high by international standards. Population growth in developing countries averaged 1.7 percent per year at that time. There were substantial cross-country differences in population growth rates. For example, Saudi Arabia's population grew at an annual average rate of 4.2 percent in the 1970s and, though it has decelerated, it remained relatively high at 3.2 percent in the 1990s. Tunisia's annual population growth averaged 3.4 percent in the late 1970s but slowed to 1.3 percent in the late 1990s, below the developing country average. In the majority of countries in the region, over two-thirds of the population is under 30 years of age. Over the last 20 years, the labor force has grown in excess of population growth and is projected to grow at 3 percent per annum till 2010. The ensuing high and rising share of working age population could, under the appropriate circumstances, be seen as a demographic gift capable of contributing positively to growth rate in the region. However, this gift is not automatic because it has to be translated into employment growth and a skill mix that is demanded in the global economy. Moreover, other policies and institutions conducive to complementary growth need to be in place to support the growing working age population. Low productivity. Another reason for the low-growth performance is the region's low or often negative growth of total factor productivity (TFP), that is, the efficiency with which factors of production such as physical capital and labor are employed to generate growth. Most of the output growth in the region has occurred as a result of increases in capital and labor rather than in TFP, particularly in non-oil economies. A sustained rise in living standards is difficult if higher rates of accumulation of physical capital and labor are not accompanied by positive TFP growth, which is often seen as a prerequisite for employing the largely young labor force in the region while avoiding a real wage erosion. The importance of TFP growth cannot be underestimated in any analysis of growth. Research shows that TFP growth accounts for about 60 percent of cross-country variations in output growth. This research also shows that the importance of TFP growth increases further if allowance is made for the contribution of human capital—job experience and level of schooling—to output growth. Recent studies that focus on MENA countries also show the importance of TFP growth to overall growth. These studies show that MENA countries that have achieved positive TFP growth rates since 1960, for example, Egypt, Tunisia, Pakistan, and Morocco, have also achieved relatively high growth rates. MENA countries with negative TFP growth rates, many of which are oil-producing countries, often tend to have relatively poor growth performance. Limited evidence on TFP growth for selected oil-producing MENA countries in the 1990s, according to research conducted by the staff of the IMF, is consistent with these long-run studies. Similarly, recent research on sources of TFP growth in the MENA region as well as other regions shows that to reverse the region's low and negative TFP growth, policymakers need to focus on improving governance and quality of institutions, investing in human capital, and establishing market-friendly and peaceful political environments. Fortunately, these are the same factors that promote investment and GDP growth, which in turn help boost employment growth. Lagging Political and Institutional ReformsDespite its geopolitical importance, the MENA region's influence in the global economic system remains weak. Political fragmentation, recurring conflicts, and authoritarian rule have hampered the development of democratic institutions and remain major obstacles to economic reform. As noted in the widely discussed Arab Human Development Report (United Nations, 2002), the region performs poorly in the areas of civil and political freedoms, gender equality, and, more generally, opportunities for the full development of human capabilities and knowledge. To overcome these handicaps, modern institutions, such as freely elected legislatures and competent and independent judiciaries, and institutions that safeguard civil and human rights need to be strengthened. The demarcation line between the public and private sectors in many MENA countries is often unclear, encouraging conflicts of interest, rent seeking (i.e., lobbying policymakers for purely private gain), and widespread corruption. Civil society organizations such as professional associations, the nonofficial media, and "autonomous" nongovernmental entities tend to be weak and are often co-opted by governments. While there are exceptions, transparency in government is poor and accountability remains a problem, as seen from perception-based measures of governance. Recent empirical studies, based on data from a large number of countries, show that quality of institutions and governance are significant not only for stimulating growth over time but also for explaining differences in the levels of per capita incomes and TFP among countries. On most measures of good governance and institutions, especially voice and accountability, regulatory quality, and control of corruption, the MENA region did not fare as well as other developing and emerging economies (Figure 3). Some progress, however, has been made recently though it has yet to influence perception-based measures of governance. In most countries, elections for representative legislatures are becoming more open and meaningful, and the political leadership is becoming more aware of the need for political reform. In part, this positive development reflects the impact of the citizens' vastly expanded access to diverse sources of information as well as internal and external pressures. The authorities' response to demands for accountability, however, has been uneven and hesitant, often leading to an easing of domestic political restrictions and some improvement in economic management, but very little in the way of genuine political reform. A deepening of political reforms is widely viewed as a prerequisite for firmly rooting badly needed economic reforms. Recognizing the importance of transparency and good governance for high-quality growth, and in part in response to the financial crises of the late 1990s, the international financial institutions launched a set of initiatives to address weaknesses in economic institutions around the world. A main weakness was recognized to be the extent to which countries observe certain internationally accepted standards of transparency in economic management, such as in the fiscal, statistical, and financial sectors and in creating a fair and open environment for the private sector. A number of countries in the MENA region have voluntarily participated in these initiatives, which include the assessment of fiscal transparency in the operation of the public sector and its interface with the private sector (the Islamic Republic of Iran, Pakistan, Tunisia, and Mauritania); data transparency and integrity (Jordan, Morocco, and Tunisia); monetary and financial policy transparency (Algeria, Tunisia, the United Arab Emirates, Morocco, and Oman); and legislation on anti–money laundering and combating of terrorist financing (nearly all countries in the region). Detailed reviews of market-based standards—for example, insurance markets, corporate governance, accounting standards, insolvency and creditor rights—are on the agenda. These assessments by the IMF and the World Bank, in collaboration with the member countries, evaluate performance in each area against the generally accepted international standards and codes. The resulting reports on participating countries in the MENA region, which are available from the websites of the IMF, the World Bank, and central banks or ministries of finance of these countries, have generally shown progress in some areas. These include, among others, recording and accounting of government's receipts and expenditures; quality of macroeconomic statistics; and financial soundness of banks and of equity and insurance markets. They have also, however, identified a number of weaknesses, including the need for creating institutions for regulatory and external oversight in the public and private sectors; public dissemination of economic statistics; and more transparent budget preparation, execution, and reporting systems. While acknowledging flaws in institutional arrangements, these reports also provide detailed diagnoses that help the authorities prioritize their institutional reform agenda and future technical assistance in these areas. Large and Costly Public SectorsA large and inefficient public sector can impose significant costs on the economy in a number of ways, such as crowding out private sector demands for credit; high cost of revenue collection; delays in awarding licenses, permits, and contracts; arbitrary enforcement of existing regulations and laws; complex and opaque court systems with high case loads; poor quality of institutions; and poor delivery of other public goods and services for which the public sector has the main responsibility, such as the rule of law and protection of property rights. These deficiencies adversely affect the business and investment climate and increase the cost of doing business for both domestic and foreign investors. For example, a 2003 World Bank study showed that costs of complying with official requirements to set up new businesses in the MENA region are five times as high as in East Asia and 2.5 times as high as in Eastern Europe and Central Asia. Size and composition of the public sector. Although much is known about the size of the central governments within the MENA region, not much is known with any certainty about the size of the overall public sector—which includes, among others, central government, local governments, and state-owned enterprises—in a majority of countries. It is, though, believed to be large. There are several reasons for this ambiguity: data limitations, unclear demarcation line between the private and the public sectors, lack of transparency regarding the size of extra-budgetary operations and contingent or hidden liabilities, and implicit subsidies, many of which are associated with the public enterprise sector. Political economy considerations have also often impeded the quest for greater clarity. Much of the growth of governments in the region during the 1970s has been fueled by high rates of economic and population growth. As a result, the size of governments in the MENA countries, as measured by the ratio of central government spending to GDP, averaged about 42 percent of GDP in the 1970s, some 12 percentage points higher than for developing countries as a group (excluding the MENA countries). Although this ratio has been declining since then, by the end of the 1990s it remained relatively high by international standards (Figure 4).

In many countries of the MENA region, the public sector has also increasingly served as employer of last resort, inflating public payrolls and wage bills. In a group of 12 MENA countries that disseminate fiscal data through the IMF's Annual Government Finance Statistics—Bahrain, Djibouti, Egypt, the Islamic Republic of Iran, Kuwait, Lebanon, Mauritania, Morocco, Pakistan, the Syrian Arab Republic, Tunisia, and Yemen—the wage bill has been growing steadily, accounting for 30 percent of government spending in the early 1980s and 35 percent in the late 1980s before leveling off by the late 1990s. By this time it was 4 percentage points of GDP higher than for all other developing countries. Although spending on subsidies and transfers in the region is higher than in other developing countries, evidence for the 12 MENA countries shows that some subsidy reforms may have paid off as they have gradually declined, both as a fraction of GDP and of total government spending. Nonetheless, generalized subsidies, which have been widely recognized as costly and inequitable, are maintained in several countries, for example, Egypt, the Islamic Republic of Iran, Libya, and the Syrian Arab Republic. In addition, countries in the region continue to devote a large fraction of their budgets to military spending. For example, in the 1990s, military spending in the region accounted for 20 percent of government spending, compared with developing countries' average of 12 percent. Although a certain level of military spending is needed for internal and external security, current levels are high by international comparison, and, in any event, high military spending did not seem to spare MENA countries from civil strife and war. Even in the absence of any impending external threat, military service is used in some countries as yet another way of alleviating unemployment pressures, a strategy that depresses productivity, delays labor market reforms, and impedes the process of human capital accumulation. Fiscal reforms. Faced with persistent deficits since the early 1970s, some countries in the region initiated fiscal reforms that, starting in the mid-1980s, began to improve fiscal balances (Figure 5). In the tax area, nine countries introduced the VAT between 1986 and 2002. Morocco and Tunisia were the first countries to introduce the VAT in 1986 and 1988, respectively. VAT revenue productivity, that is, average VAT revenue gain per 1 percentage point change in the VAT rate, in these countries compares favorably with that in many OECD countries with a longer history of VAT. Efficient and modern VATs have been recently introduced in Lebanon and Sudan and are under consideration in the Islamic Republic of Iran and some of the countries of the GCC.

A poorly administered tax system is another channel through which the public sector can impose significant costs on the economy. Therefore, some fiscal reforms have aimed at reducing the cost of domestic resource mobilization by improving the administration of the tax system. Adoption of the VAT and its associated tax administration improvements have tended to enhance the efficiency of the entire tax system. Other fiscal reforms have targeted a broadening of the tax base through reduction or elimination of tax exemptions (e.g., Jordan, Pakistan), the modernization of procedures including computerization (e.g., Lebanon), and the reform of customs administration (e.g., Lebanon, Morocco, some of the GCC countries, and, more recently, Egypt). On the expenditure side, significant reforms have taken place in the area of public expenditure management systems (e.g., some of the GCC countries, Jordan, Mauritania, and Pakistan). Privatization. Although public ownership in itself is not necessarily a cause for inefficiency in the operation of public entities, the full development of productive enterprises in an increasingly competitive environment has often called for private ownership within a framework of sound corporate governance structures. As a result, privatization of state-owned enterprises has been viewed as one approach to the rationalization of public sector activities. Although comparison of privatization receipts across countries is somewhat problematic, the available data show that the privatization process in the MENA region has been rather slow. For example, according to the World Bank's Global Development Finance report (2001), the MENA region's privatization receipts in the 1990s amounted to some $8.2 billion, the same as that for the sub-Saharan Africa region in the 1990s. This amount, however, remained small compared with $178 billion for Latin America and the Caribbean, $65 billion for Eastern Europe and Central Asia, $44 billion for East Asia and Pacific, and $12 billion for South Asia for the same period. Throughout the world, major infrastructure, such as telecommunications and power, has generally been the sector that generated the largest proceeds from privatization and this has also been the case in the MENA region. In addition to the outright sale of government assets, privatization

attempts have taken other forms. Some countries are experimenting with

financial contracts and leasing arrangements between the public and the

private sectors. Egypt has made some successful inroads into the divestment

of state holdings by adopting domestic stock exchange floatation and

employee buyouts. Jordan's privatization strategy has benefited from

proper sequencing and a clear institutional environment, supported by

legislative and regulatory oversight. From 1994 to 2001, Egypt and Jordan

raised some $4.9 billion (6 percent of GDP) and $800 million (8.5 percent

of 2002 GDP), respectively, in privatization receipts. Morocco raised

an estimated $1.2 billion by awarding a second global systems license

for mobile communication in 1999 and $2.1 billion with the sale of Morocco

Telecom in 2000. In Saudi Arabia, a list of activities targeted for privatization

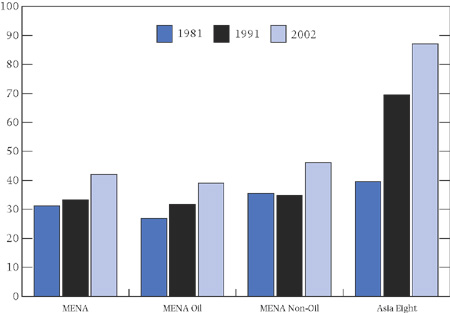

was issued While progress has been made, the process of rationalizing the role of the state and adapting it to the requirements of a modern, competitive economy remains incomplete. Most economies in the region remain dominated by large public sectors that are heavily vested in financial markets through state-owned banks and other public enterprises. These provide a wide range of goods and services that would normally be produced by the private sector in a market-based, competitive environment. More often than not, public enterprises are not part of the regular budget process and hence escape the required public scrutiny. Many are actively engaged in quasi-fiscal activities that are not subject to the rigors of transparency and financial accountability. Public infrastructure. The quality of the infrastructure in the MENA region varies enormously across countries and sectors. It is good or well developed in the GCC countries, Lebanon, Jordan, Tunisia, and Morocco, but somewhat less developed in others. The transportation infrastructure, for example, is highly developed in most countries of the region but telecommunication services, especially through modern, high-capacity fixed line networks, remain inadequate. According to the World Bank's 2002 World Development Indicators, as of 2000, the average waiting time for connection to public telephone mainlines for the region was 1.6 years, with the waiting time for individual countries ranging from zero or one month (the United Arab Emirates and Morocco, respectively) to 4.4 years or more (Sudan and the Syrian Arab Republic, respectively). However, it should be noted that cross-country comparisons of waiting time is complicated by the advent of mobile phones and applicants registering more than once to obtain a public fixed phone line. Inefficient production and distribution of electricity, an important ingredient in the business infrastructure, is another cause for concern and another high cost area in the MENA region. According to the same source, in 1999, transmission losses in electricity networks in the region amounted to 16 percent of output compared with averages of 11 percent for sub-Saharan Africa and 7 percent for East Asia. Poor provision of basic public goods and services, such as public infrastructure, accounts in large part for the low private sector investment response in the MENA countries. Experience has shown that certain types of reforms are conducive to private sector development and, if appropriately implemented in the region, could help improve performance. For instance, further privatization efforts in the telecommunication and infrastructure sectors, appropriate regulatory oversight, proper sequencing of regulatory reform, and an adequate social safety net mechanism—all could serve to further stimulate private sector investments. Education: Room for Improving Efficiency and EquityHuman capital—whether measured by life expectancy, years of schooling, job market experience, literacy rates, enrollment rates, or student test scores—is an important factor in economic growth, employment generation, and globalization. Availability of key complementary inputs—physical capital, labor, and human capital—has long been recognized as an important factor for the location of economic activity, and this is especially true in an increasingly globalized economy characterized by high capital mobility. Although investment capital seeks both a skilled and educated as well as a cheap and unskilled labor force, it is generally accepted that growth, and more assuredly a higher standard of living, is more likely to be sustained with an educated workforce that can adapt its skills and implement new ideas. Recent research suggests that countries starting with lower productivity but with a more educated workforce close the gap between their per capita income and that of richer countries at a faster rate than countries with a less educated workforce. Foreign direct investment is also found to contribute more to growth in countries endowed with a more educated labor force. Over the past 30 years, the MENA region has made significant progress in increasing its stock of human capital. In a sample of 12 MENA countries—which include Afghanistan, Algeria, Bahrain, Egypt, the Islamic Republic of Iran, Iraq, Kuwait, Pakistan, the Syrian Arab Republic, Sudan, Tunisia, and Jordan—the segment of the population over 25 years of age with no schooling declined from 80 percent in 1970 to 46 percent in 2000. During the same time period, average years of schooling increased from 1.3 years in 1970 to 4.5 years in 2000. In several countries in the region—some of the GCC members, Lebanon, Jordan, and Tunisia—human development indicators are high by international comparison. However, for the region as a whole, the quality of human capital has not advanced correspondingly. Although the MENA countries spend more on education than other countries at comparable income levels, their educational systems do not perform better. Possible reasons for this include emphasis on quantity at the expense of quality of teachers, lagging educational technology, inflated administrative bureaucracies, and a spending bias toward higher, rather than primary, education. Dropout and repetition rates remain high in several countries. In some countries, the system produces graduates with skills that are not in demand in a modern, globalizing economy. One area of education that has seen significant gains, but where much more needs to be done, is the closing of the gap between male and female access to education. In some countries, such as Lebanon, Syria, Jordan, and Tunisia, male-to-female education ratios are converging. In many other countries in the region, however, enrollment rates, years of schooling, and literacy rates remain distinctly lower for females than for males. Though female illiteracy rates have declined significantly over the past decades, the adult female illiteracy rate in 2000, at 41 percent, is almost twice that of the male illiteracy rate. The male-female education disparity has an economic cost. Recent research (Klasen, 2002) shows that gender inequities have adverse growth effects—about 0.85 percentage points of the real per capita growth differential between the MENA region and East Asia is accounted for by gender inequality. To boost the efficiency of their education systems, countries in the region need to streamline the management of such systems (most education systems in MENA countries are managed by at least three ministries), reform hiring and remuneration practices to better link them to results, encourage and increase private participation in the education systems, and adapt education programs and syllabi to the demands of a modern economy to better exploit the opportunities offered by increased globalization of information and technology. Financial Market Development: Further Reform Holds PromiseDevelopment of financial sectors in the MENA region made significant strides from the 1970s through the mid-1980s. As in many of the other factors underlying growth, the performance on financial development is differentiated across countries in the region. Some countries now have well-developed financial, mainly banking, sectors. These include the GCC countries, Lebanon, and Jordan. Others countries in the region, such as Egypt, Morocco, and Tunisia have made important advances over the past 30 years, although further steps remain to be taken. Recent banking sector and monetary policy reforms include strengthening of banking regulation and supervision, such as in Bahrain, Jordan, Lebanon, Morocco, Sudan, and Tunisia; introduction of greater flexibility in exchange rates; and a move toward the use of indirect monetary policy instruments. Overall, financial markets in the MENA region, which remain dominated by traditional banking activity, are fragmented. As a result, they have not played the intermediation role needed to underpin a more vigorous pace of investment and growth. Though the region has been a net exporter of capital for the past 30 years, the financial sector has failed to develop the capacity to channel a significant portion of these savings into long-term productive investment within the region. In many cases, banking systems remain dominated by public ownership or control with considerable exposure to government debt, weak regulatory and enforcement capacity, management skills that need upgrading, and weak links to international capital markets. With minor exceptions, equity and debt markets, insurance, leasing, and long-term financing remain weak and underdeveloped. A look at common quantitative measures of financial depth provides a similar analysis. While the ratio of broad money to GDP increased in the MENA region from 50 percent of GDP in 1980 to 70 percent in 2002, and credit to the domestic private sector from 30 percent to 40 percent of GDP, these rates remain at half their corresponding levels in East Asia (Figure 6). In addition, the increase in private investment during that time has not kept pace with credit expansion. The resulting liquidity growth has fueled capital outflows, inflated valuations in the equity and property markets, and subsidized construction activity. Heavy reliance on real estate collateral in some countries has led to poor provisioning policies.

Allocation of credit to more productive investment should guide lending strategy. Experience shows that it is investment in plant and equipment with their embedded technology that is growth enhancing rather than investment in real estate, overvalued equities, or subsidized construction. A certain level of infrastructure is needed of course to accommodate the growing population in the region and the expanding private sector activity, but investment in the construction sector in the MENA region is disproportionate to other, more productive, investments. In fact, high growth rates in real estate and in construction may have been a factor in the negative TFP growth recorded in some MENA countries. Trade Liberalization: Some Progress, but an Unfinished AgendaResearch indicates that trade openness—the degree to which foreigners and nationals may transact goods and services without government-imposed costs, that is, tariffs and nontariff barriers—is a significant contributor to higher productivity and per capita income growth. Increased trade boosts productivity by importing knowledge and stimulating innovation. In the MENA region, there is a dichotomy in trade regimes. Many countries, including the GCC members, Yemen, and Mauritania, and, to a lesser extent and more recently, Algeria and Jordan, are generally open to free trade. However, the remaining countries, despite recent trade liberalization efforts, such as in the Islamic Republic of Iran, Morocco, Pakistan, Tunisia, and Sudan, continue to maintain relatively high tariffs and nontariff barriers. As a result, for the MENA region as a whole, the overall degree of trade restrictiveness, as measured by an index developed by the IMF staff, is above that of other regions in the world, although it has improved over the last six years (Figure 7). In terms of nontariff barriers, MENA countries are not that different from developing countries as a group.

Inappropriate Exchange Rate PolicyAn appropriate exchange rate policy is an important ingredient in supporting globalization and growth. About half of the countries in the region have fixed exchange rates, and another quarter have exchange rate regimes that are near fixed, such as pegs or moving pegs with narrow bands. For most currencies outside of the Maghreb region of Algeria, Libya, Mauritania, Morocco, and Tunisia, the peg or reference currency is the U.S. dollar. Although the peg has served some countries well, such as in GCC countries, the choice of an exchange rate regime has not always been appropriate in the region more generally. Countries have had a tendency to delay adjustment of pegs in the presence of clear real exchange rate appreciation or have shown reluctance to exit an inflexible arrangement when this is called for. Delayed adjustment can manifest itself in real exchange rate overvaluation and misaligned exchange rates. A high real exchange rate overvaluation occurs when the nominal exchange rate is fixed in the face of high domestic inflation. Real exchange rate overvaluations—for example, as measured by its misalignment based on purchasing power parity comparisons—have persisted in some of the MENA countries, thus distorting relative prices and possibly leading to misallocation of resources. Real exchange rate overvaluation often also reflects a poor mix of macroeconomic policies and associated imbalances. A large body of empirical work shows that countries with overvalued real exchange rates tend to have lower rates of growth, and this indeed may have been a factor in lowering economic growth in the MENA region, particularly in MENA countries that are not part of the GCC. The weight of evidence indicates that greater flexibility in exchange rate management enhances the ability of a country to deal with exogenous shocks, reduces the risk of banking crises, and contributes to maintaining financial stability. Inappropriate exchange rate policies and the inability to resolve the closely related phenomenon of the "resource curse" in natural-resource-rich countries are important factors in the slow growth of non-oil exports from the region. It is possible that inflexible exchange rate policies, among others, may also have been a factor in delaying the development of monetary policy frameworks (e.g., inflation targeting), that are judged to be more suitable to emerging economies in the region seeking to integrate more fully into the world economy. Such economies include those of Egypt, Jordan, Lebanon, Morocco, and Tunisia. Some progress has been made recently in introducing greater flexibility in the exchange rate policies in the region, such as in Egypt, the Islamic Republic of Iran, Morocco, Libya, Pakistan, and Tunisia. Such flexibility is important for the continuing efforts of these countries to undertake structural reforms that promote economic efficiency and stimulate trade and investment. The Urgency of ReformsHow can the MENA region reignite and sustain high output and employment growth, better integrate with the global economy, and manage the booms and busts in oil prices? The past 20 years have seen clear progress in implementing macroeconomic reforms and in moving toward structural reforms. However, these have neither gone far enough to address the deep-rooted structural problems nor seriously tackled the governance and institutional reform issues. There is a need for accelerated and broad action on this front, including a fundamental reassessment of the role of the state in the economy and the creation of a rules-based regulatory environment. Greater efforts are needed to accelerate trade liberalization; reform financial and labor markets; and improve transparency, governance, and the quality of state institutions. Economic liberalization should ensure fair and open competition where market forces could create opportunities for a more efficient allocation of resources and support private sector investment and growth. These reforms must aim at transforming the business and investment climate that is crucial to economic growth, employment generation, and the region's integration into the global economy. Oil-exporting countries in the region need to conduct fiscal policy by taking a longer view of their resource endowments and their impact on the country's welfare. Fiscal policy, the single most important policy instrument in the oil-producing countries, needs to cushion the effects on the economy of booms and busts in the oil markets and, over the longer term, take account of issues of intergenerational equity in mapping out strategies for government spending, investment, and financing of public sector operations. Although some countries have taken steps to delink government spending from current oil receipts, a much more considered and comprehensive approach is needed to help diversify the economy and remove obstacles to developing the non-oil sector. Reducing dependence on oil would also require establishing modern tax policy structures and tax administrations, with broad-based taxes and low rates. Several non-oil economies in the region rely on aid, capital flows, and worker remittances from the oil-producing MENA countries. As the latter move toward more balanced economic structures, the non-oil economies would also need to make necessary adjustments. While all countries in the region need to maintain macroeconomic stability and pursue structural reforms, it is the reform of public and private sector institutions that, in the final analysis, will make the difference. According to the April 2003 issue of the IMF's World Economic Outlook, there could be substantial economic gains for MENA countries that introduce such reforms. Strengthening the quality of institutions in the MENA region to that of the advanced economies could result in a 20-fold increase in real per capita GDP and a 3 percentage point increase in growth of real per capita GDP. A more determined and sustained drive by MENA countries toward a more open and democratic society, embracing fundamental structural and institutional reform, would therefore appear to be the best assurance that the region, with its rich civilization and abundant endowment of natural resources, can achieve its potential for higher growth rates and a decent and dignified life for the 500 million human beings who live in it. BibliographyAbed, George T., 2003, "Unfulfilled Promise," Finance & Development, Vol. 40, No. 1, pp. 10–14. Available via the Internet: http://www.imf.org/external/pubind.htm. ———, and Sanjeev Gupta, eds., 2002, Governance, Corruption, and Economic Performance (Washington: International Monetary Fund). Alfaro, Laura, Sebnem Kalemli-Ozcan, and Vadym Volosovych, 2003, "Why Doesn't Capital Flow from Rich Countries to Poor Countries? An Empirical Investigation" (unpublished; Houston: University of Houston). Barnett, Steven, and Rolando Ossowski, 2002, "Operational Aspects of Fiscal Policy in Oil-Producing Countries," IMF Working Paper 02/177. ———, 2003, "What Goes Up . . .," Finance & Development, Vol. 40, No. 1, pp. 36–39. Available via the Internet: http://www.imf.org/external/pubind.htm. Bennett, Adam, 2003, "Failed Legacies," Finance & Development, Vol. 40, No. 1, pp. 22–25. Available via the Internet: http://www.imf.org/external/pubind.htm. Berg, Andrew, and Anne Krueger, 2003, "Trade, Growth, and Poverty: Bisat, Amer, Mohamed El-Erian, and Thomas Helbling, 1997, "Growth, Investment, and Savings in Arab Economies," IMF Working Paper 97/85. Dasgupta, Dipak, Jennifer Keller, and T.G. Srinivasan, 2002, "Reform and Elusive Growth in the Middle East: What Has Happened in the 1990s?" Middle East and North Africa Paper Series 25 (Washington: World Bank). Davis, Jeffrey, Rolando Ossowski, James Daniel, and Steven Barnett, 2001, Stabilization and Savings Funds for Non-Renewable Resources, IMF Occasional Paper No. 205. Dowrick, Steve, 2003, "Ideas and Education: Level or Growth Effects?" National Bureau of Economic Research Working Paper No. 9709. Caselli, Francesco, 2003, "The Missing Input: Accounting for Cross-Country Income Differences," in The Handbook of Economic Growth (New York: Elsevier Science), forthcoming. Creane, Susan, Rishi Goyal, A. Mushfiq Mobarak, and Randa Sab, 2003, "Banking on Development," Finance & Development, Vol. 40, No. 1, pp. 26–29. Available via the Internet: http://www.imf.org/external/pubind.htm. Easterly, William, and Ross Levine, 2001, "It's Not Factor Accumulation: Stylized Facts and Growth Models," World Bank Economic Review, Vol. 15, No. 15, pp. 177–219. Ebrill, Liam, Michael Keen, Jean-Paul Bodin, and Victoria Summers, 2001, The Modern VAT (Washington: International Monetary Fund). Eken, Sena, David A. Robalino, and George Schieber, 2003, "Living Better," Finance & Development, Vol. 40, No. 1, pp. 15–17. Available via the Internet: http://www.imf.org/external/pubind.htm Fischer, Stanley, 2003, "Globalization and Its Challenges," Richard Ely Lecture presented in January 2003 at the American Economic Association Meeting in Washington, DC. Available via the Internet: http://www.iie.com/Fischer. Gardner, Edward, 2003, "Wanted: More Jobs," Finance & Development, Vol. 40, No. 1, pp. 18–21. Available via the Internet: http://www.imf.org/external/pubind.htm. Hall, E., and Charles I. Jones, 1999, "Why Do Some Countries Produce So Much More Output Per Worker Than Others?" Quarterly Journal of Economics, Vol. 114, pp. 83–116. International Monetary Fund, Reports on the Observance of Standards and Codes, various countries and years (Washington: International Monetary Fund). Available via the Internet: http://www.imf.org/external/np/rosc/rosc.asp. ———, 2003, World Economic Outlook, April 2003: Growth and Institutions (Washington: International Monetary Fund). Jbili, Abdelali, and Vitali Kramarenko, 2003, "Should MENA Countries Float or Peg?" Finance & Development, Vol. 40, No. 1, pp. 30–35. Available via the Internet: http://www.imf.org/external/pubind.htm. Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi, 2003, "Governance Matters III: Governance Indicators for 1996–2002," unpublished World Bank Discussion Paper. Available via the Internet: http://www.worldbank.org/wbi/governance. Keller, Jennifer, and Mustapha K. Nabli, 2002, "The Macroeconomics of Labor Market Outcomes in the MENA Region over the 1990s." Available via the Internet: http://www.worldbank.org/wbi/mdf/mdf4. Klasen, Stephan, 2002, "Low Schooling for Girls, Slower Growth for All? Cross-Country Evidence on the Effect of Gender Inequality in Education on Economic Development," World Bank Economic Review, Vol. 16, No. 3, pp. 345–73. Kuczynski, Pedro-Pablo, and John Williamson, eds., 2003, After the Washington Consensus: Restarting Growth and Reform in Latin America (Washington: Institute for International Economics). Makdisi, Samir, Zeki Fattah, and Imed Limam, 2003, "Determinants of Growth in the MENA Region," Arab Planning Institute Working Paper No. 0301 (Kuwait). Available via the Internet: http://www.arab-api.org. Prasad, Eswar, Kenneth Rogoff, Shang-Jin Wei, and M. Ayhan Kose, Effects of Financial Globalization on Developing Countries: Some Empirical Evidence, IMF Occasional Paper No. 220, forthcoming. Available via the Internet: http://www.imf.org. Rodrik, Dani, ed., 2003, In Search of Prosperity: Analytical Narratives on Economic Growth (Princeton, New Jersey: Princeton University Press). ———, 2003, "Growth Strategies," in The Handbook of Economic Growth (New York: Elsevier Science), forthcoming. Available via the Internet: http://www.ksg.harvard.edu/rodrik. ———, Arvind Subramanian, and Francesco Trebbi, 2002, "Institutions Rule: The Primacy of Institutions over Integration and Geography in Economic Development," IMF Working Paper 02/189. Sala-i-Martin, Xavier, and Elsa V. Artadi, 2002, "Economic Growth and Investment in the Arab World," Columbia University Discussion Paper No. 0203-08 (New York). Sundararajan, V., Udaibir S. Das, and Plamen Yossifov, 2003, "Cross-Country and Cross-Sector Analysis of Transparency of Monetary and Financial Policies," IMF Working Paper 03/94. United Nations Development Program, 2002, Arab Human Development Report (New York). World Bank, 2001, Global Development Finance: Building Coalitions for Effective Development Finance (Washington: World Bank). ———, 2002, World Development Indicators (Washington: World Bank). ———, 2003, Trade, Investment, and Development in the Middle East and North Africa: Engaging with the World (Washington: World Bank). |

| Public Affairs | Media Relations | |||

|---|---|---|---|---|

| E-mail: | publicaffairs@imf.org | E-mail: | media@imf.org | |

| Fax: | 202-623-6278 | Phone: | 202-623-7100 | |