During the years that followed the euro’s introduction, financial integration proceeded rapidly and markets and governments hailed it as a sign of success. The widespread belief was that it would benefit both south and north—capital was finally able to flow to where it would best be used and foster real convergence.

But in fact, a lasting convergence in productivity did not materialize across the European Union. Instead, a competitiveness divide emerged. As the financial crisis gripped the euro area in 2010, these and other problems came to the fore.

Three years later, the financial symptoms of the crisis are thankfully receding with a new sense of optimism in markets. But the underlying problems—lack of convergence of productivity and the structural flaws in the architecture of the monetary union—have only been partially addressed.

So where do we stand, and what more is needed?

(Not) the right kind of integration

Europe has committed itself to increasingly harmonize legal structures and governance to facilitate the free flow of goods, services, and capital, as well as the free movement of its citizens. Even those European countries that are not part of the European Union, such as Iceland, Norway and Switzerland, share formal ties through pacts and treaties, such as the European Free Trade Agreement.

But if Europe has clearly become more integrated de jure, has it made a difference, de facto, in economic terms? The answer is clearly yes. One simple way of illustrating this is to look at correlations of business cycles between countries.

Figure 1-2, which depict these correlations, show the close links developed between European economies during the past decade. All economies in the European Union—not just euro area member states—are more tightly clustered now than they were.

But integration has many more dimensions. For the 17 euro area members, the introduction of a common currency also meant a common monetary policy and, for a while, the convergence of risk premia. This encouraged capital to shift from the richer north to the poorer south (known as the periphery), and differences in sovereign yields across the euro area narrowed quickly.

But as we now know, the optimism about the use of these funds turned out to be overdone. Domestic productivity in most of the recipient countries did not improve—credit was used to finance current consumption and investment in real estate rather than productive capital.

In fact, there has been little absolute real convergence in the euro area. Those euro area countries that had low per capita incomes in 1999 did not have the highest per capita growth rates.

The newly accessant countries from emerging Europe did better—their per capita incomes seem to be converging faster to northern Europe levels (Figure 3). These economies were in a better position to take advantage of global growth, attract FDI, and strengthened their integration in worldwide supply chains, in particular by building strong links with Germany.

The crisis in the euro zone stems, in large part, from the unwinding of financial integration that occurred in the absence of the necessary accompanying improvements in productivity. As the gaps in growth prospects became apparent, financial markets again began to discriminate among countries that hitherto had enjoyed similar borrowing costs. This resulted in a reversal of capital flows and a fragmentation of the financial system in the euro zone.

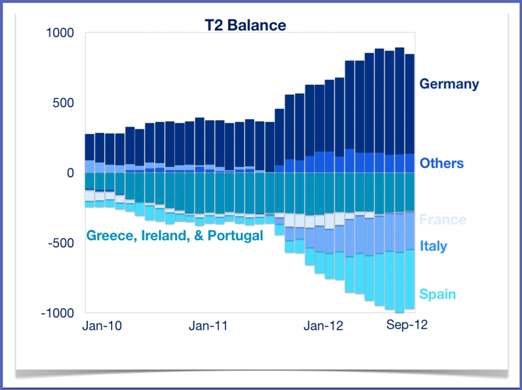

That fragmentation has had implications for the monetary policy transmission mechanism. The Target2 system, the mechanism by which national central banks in the euro area borrow from or lend to each other, is a good indicator of financial fragmentation along national borders (Figure 4).

In late 2011, Target2 balances increased particularly due to fragmentation affecting the markets in Italy and Spain. Surplus countries, particularly Germany, provide the counterbalance. On the positive side, the existence of the Target 2 system was an important shock absorber that worked when needed, and now balances have stabilized.

In the past three years, the hard-hit countries on the southern periphery have implemented tough reforms to improve their competitiveness, and these are now starting to bear fruit. But much work remains to be done.

Research from the IMF shows that if euro area member states managed to close half the gap with OECD best practice in labor market and pension policies, they could boost GDP by almost 1½ percent on average after five years—and by another 2¼ percent if more competition is introduced into markets for products and services.

As the reform policies take hold and growth prospects improve, private capital has to return again to the periphery. But the countries have to put it to good use—to finance investment that turns those prospects into reality.

Fixing the flaws

While national governments need to continue their reform efforts, it is by now widely accepted that managing the crisis also requires “more Europe” to undo the financial fragmentation and avoid sudden stops in capital flows within the currency union.

What is economically necessary is, however, politically difficult: public support for the European project has fallen in most EU member countries. So how much more integration is really necessary for the euro area and the European Union more generally?

Many of the measures taken recently aim at strengthening the functioning of the monetary union. Figure 5 shows euro area policy actions taken over the last year or so. Actions which help growth are in yellow; those which help integration are in blue; and the intersection is in green. The process has not always been elegant and I would characterize it as “just in time integration”—but euro area leaders have defied the skeptics and managed to make significant progress.

Looking ahead, two elements would seem necessary to make the union more viable: a banking union, to make the financial sector more robust to future economic shocks; and more fiscal integration, to address the current gaps that amplify country-level shocks into zone-wide events.

Recent decisions on the shape of a banking union constitute important steps to strengthen the architecture of monetary union. From an IMF perspective, a banking union also requires a common fiscal backstop to deal with resolution of troubled banks and a common approach to deposit insurance.

There is not yet consensus on the shape of closer fiscal integration. Some proposals have been made for a common euro area treasury, with its own centralized budget. Other proposals call for the power to direct national budgets, and for common borrowing. Clearly, there are direct monetary implications, as well as substantial consequences for national sovereignty, that policymakers need to carefully think through. The empirical evidence from a variety of federations across the world shows governments can make many models work.

More integration, more growth

Further steps to integrate Europe are taking place against the backdrop of a still very weak economic outlook. For this reason, the focus needs to be squarely on growth, particularly to address unemployment, which has reached intolerable levels in much of the EU.

That means making progress on national level reforms that will encourage labor mobility, product market reforms, and investments in infrastructure and education to foster competitiveness. Other reforms, such as central support for market access or troubled banks, need to happen at the eurozone level.

2012 was a year of balancing on the edges of cliffs and precipices for Europe. 2013 needs to be a year of climbing mountains—doing the long and hard work of restoring competiveness across economies to restore growth, and making steady progress on completing the architecture of the monetary union.