What should governments do about high public debt-to-GDP ratios? This question is getting much-deserved attention. Let’s abstract from macroeconomic (business cycle) considerations and look at the issue purely from an optimal tax smoothing perspective—that is, weighing the cost and benefits of raising taxes to pay down debt. By doing so we decidedly do not engage in the current debate about the contribution that fiscal policy may make to demand management.

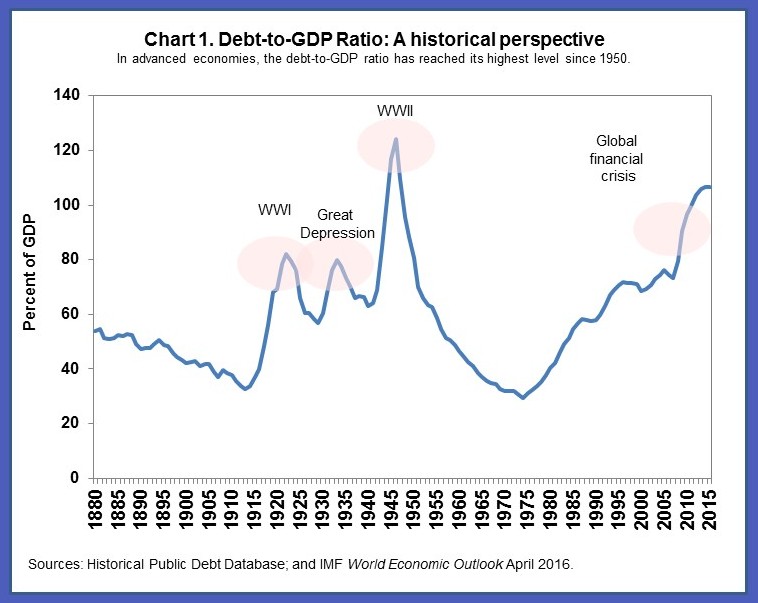

In advanced economies, the debt-to-GDP ratio has reached the highest level on record since 1950 (Chart 1). The increase in debt has been particularly pronounced since the beginning of the Great Recession, when many governments stepped in to rescue their financial system and stimulate economic activity—at the expense of a substantial increase in general government’s liabilities. In an era of low inflation and low growth, deleveraging is difficult. At the same time, with bond yields at historical lows, fiscal policy has been called upon to play a more active role to head off a new mediocre of subpar growth and extremely low inflation.

In an interesting paper published last year, our IMF colleagues Jonathan Ostry, Atish Gosh and Raphael Espinoza argued that countries can live with high debt under certain assumptions (for example, continuous access to financing).They look at the interaction between tax smoothing and productive public investment in determining optimal policy. In their model, high public debt ratios are bad for standards of living (or growth) because they imply higher tax rates. Nevertheless, after a sharp increase in the debt ratio, taxes should be increased only to the extent necessary to stabilize it. Pushing taxation further up to reduce debt would not be optimal because the excess burden of taxation increases more than proportionally to the tax rate. The contribution of Ostry et al. was to show that from the fact that public debt is bad for growth (or the standards of living) it does not necessarily follow that governments should actively pursue debt reduction policies. The authors stress that governments should nevertheless be opportunistic in reducing public debt, for instance when there are privatization receipts, licensing royalties, or economic booms that yield exceptionally high revenues

In a recent working paper, we follow their contribution but simplify the framework by disregarding public investment and by directly postulating the normative goal of minimizing the excess burden of taxation. But, on the other hand, we extend it by taking into consideration the empirical fact that financial crises, natural disasters, and wars are repeated events, with sizable implications for public finances. Moreover, we were motivated by the perception that risks to public finances are asymmetric: large, positive disturbances to the public debt ratio are much more likely than negative shocks of similar magnitude (IMF, 2016). To put it simply, sudden surges in debt ratios from, say, wars or bank bailouts are more common than sudden drops of debt ratios from, say, privatizations or licenses.

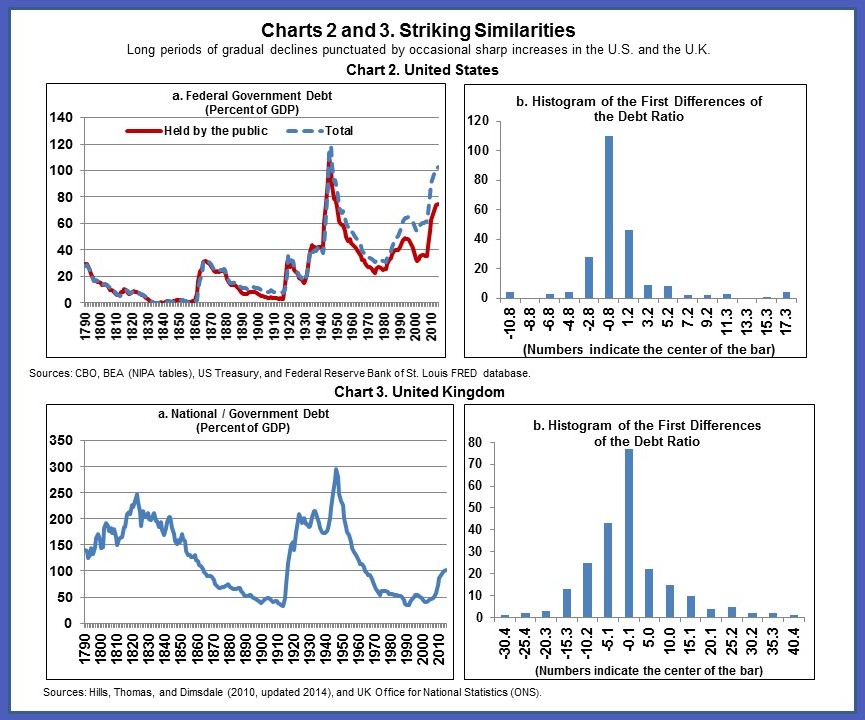

To document this asymmetry, we looked at the long-term trends of debt ratios in the United States and the United Kingdom using historical time series. In the last 200 years, these two countries provided the ultimate safe asset to the world economy and data are available for both (see Chart 2, for the U.S., and Chart 3, for the U.K.). Chart 2a and 3a show the historical behavior of the debt ratio over the period 1790 to 2014. The pattern is striking: long periods of persistent, gradual declines punctuated by occasional sharp increases. Charts 2b and 3b show the histogram of changes in the debt ratio, which suggests that the distribution is skewed to the right. In the paper, we confirm this visual impression through a battery of statistical tests. Those allow for the rejection of symmetry.

How often and at what scale do surges in debt ratios occur? In the United Kingdom, we observe on average a (positive) outlier year every 28 years with an average increase in the debt ratio of 30.8 percentage points of GDP. The corresponding numbers for the United States are an outlier every 32 years on average with an average increase in the debt ratio of 15.4 percentage points of GDP. To prevent debt from ratcheting up because of such future shocks, the debt ratio needs to decline in normal years, as insurance. Our computations show that, indeed, the average decline in the debt-to-GDP ratio was 1.3 percentage points of GDP in the UK and 0.3 in the United States. The corresponding model normative benchmarks are, respectively, 1.1 and 0.5 percentage points. Surprisingly, the actual behavior of public debt in the two countries that have provided the ultimate safe asset to the world economy, over the last 200 years, is close to the normative implications of the model.

The key to optimal tax smoothing is small but enduring public debt reductions in normal years.