A souvenir shop in Lisbon, Portugal: Income convergence in the euro area has slowed (Photo: Rafael Marchante/REUTERS/Newscom)[/caption]

A souvenir shop in Lisbon, Portugal: Income convergence in the euro area has slowed (Photo: Rafael Marchante/REUTERS/Newscom)[/caption]

By Jeffrey Franks and Hanni Schölermann

September 13, 2017

Versions in Español (Spanish), 語 (Japanese)

The experience of recent decades has challenged the prediction that the single currency would help differences in income levels across euro area countries narrow over time. This income convergence among the founding countries of the euro has not happened, prompting a need for further economic reforms. While newer members of the euro have converged, even this trend has stalled since the crisis.

When the 12 founding members of the euro embarked on the project of economic and monetary union, they had a clear expectation that sharing a single currency and liberalizing capital flows would boost economic growth, and help countries with lower initial income levels catch up to their richer neighbors.

Although monetary policymaking can operate effectively when income levels differ, convergence helps to ensure that the gains from economic integration are shared, and thus bolster the cohesion of the monetary union.

Great expectations of convergence

Countries expected incomes would converge as investment rose in lower-income countries. Investors would take advantage of the disappearance of exchange-rate risk and freed cross-border capital markets to increase capital spending in countries where investment had previously been weak.

The architects of the euro area counted on the single market to support convergence through other channels as well: workers could move to countries with higher incomes, thereby increasing their own pay as well as that of those staying in their home country by tightening the local labor supply. Moreover, the common currency would increase cross-border trade and firms would exploit greater economies of scale, raising productivity and living standards across countries.

Yet, the expected convergence has not materialized among the original 12 members.

Catching-up disappointed

Our recent paper that accompanied the IMF’s annual consultation report on the euro area assesses the degree of income convergence among the euro area’s 12 founding members before and after euro introduction.

The analysis shows that the euro’s founding fathers had reason to expect convergence under economic and monetary union based on previous experience: in the decades leading up to the 1990s, when monetary union was founded, there had been steady income convergence. As economic integration deepened, euro area countries with lower initial GDP per capita, such as Spain or Ireland, grew faster than their higher-income peers, and cross-country differences in income levels narrowed.

However, contrary to expectations, the catching-up process stopped in the monetary union. Income differences among the original 12 countries failed to decrease further in the first decade of the euro, bringing convergence to a halt. Since the crisis, the uneven recovery has caused per capita income levels to diverge across these countries, reversing the progress made over earlier decades.

Here are three charts to understand how income convergence unfolded, and why it has so far failed to meet expectations.

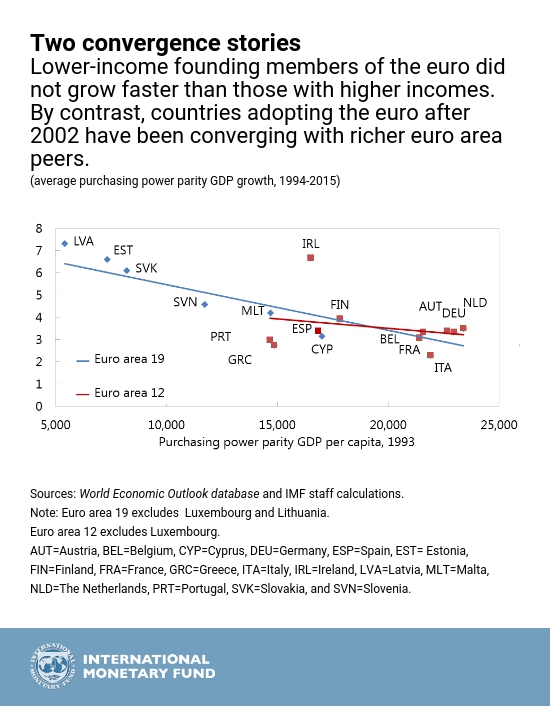

The variation in per capita income levels across the original euro area member countries narrowed before the currency was introduced in 1999, remained largely unchanged in the 2000s, and widened sharply after the crisis. For new euro members, income differences continued to decrease until the crisis, but have changed little since.

We also look at whether countries with initially lower incomes per capita grew faster than higher-income countries over the period 1993–2015. In this graph, a downward sloping line signifies convergence. But the red line for the original euro area members is almost flat, meaning very little convergence. Indeed, if fast-growing Ireland is excluded, there would be no convergence at all. By contrast, countries that adopted the euro after 2002 did experience rapid catch-up vis-à-vis the rest of the euro area between 1993 and 2015, with income gaps narrowing considerably, shown by the steeply downward-sloping blue line.

Poor productivity growth, no convergence

Disappointing economic growth in three of the four original euro area countries with the lowest GDP per capita in 1993—Greece, Portugal and Spain—is the main explanation for the lack of convergence among the founding members. These countries experienced substantial capital inflows in the first decade of the euro, but these investments fueled unsustainable credit booms in consumption and real estate rather than boosting productivity.

In fact, since the 1990s, total factor productivity growth, which measures how efficiently capital and labor are used in production, has been consistently slower in these countries than in their euro area peers. It has also seen a more pronounced slowdown over time. A sharper fall in investment and employment since 2008 adds to the post-crisis divergence in growth.

Steps to restart convergence

Is the euro to blame for the lack of convergence? IMF research suggests that the productivity slump behind this phenomenon is related more to a lack of sufficient structural reforms at the national level rather than the single currency.

To restart convergence, policymakers should focus on raising productivity growth in the lagging countries. While deepening the single market at the European level in areas like capital markets, energy, and digital commerce can help, the main responsibility for reviving productivity growth rests with reforms at the national level. These should aim to make product and labor markets more efficient and to encourage investment in more productive technologies.

The founders of the euro were aware that members would have to enhance competitiveness and productivity to compensate for the lack of exchange-rate flexibility under monetary union. Twenty-five years on, with slipping productivity growth in Europe and tougher competition from a more globalized world economy, reforms are even more imperative to sustain growth and restart the convergence process.