December 13, 2018

[caption id="attachment_25244" align="alignnone" width="1024"] Villagers of Moruleng mining community in South Africa; Sub-Saharan Africa countries can see an increase in growth by relying less on commodities and more on non-resource intensive investments. (Photo: SIPHIWE SIBEKI/Reuters/Newscom) [/caption]

Villagers of Moruleng mining community in South Africa; Sub-Saharan Africa countries can see an increase in growth by relying less on commodities and more on non-resource intensive investments. (Photo: SIPHIWE SIBEKI/Reuters/Newscom) [/caption]

The story of Africa’s growth rate over recent years is a tale with several story lines. Key to the tale is the degree of dependence on commodities. Our Chart of the Week shows how the greater a country’s reliance on commodities, the more dramatic the impact of the 2014 commodity shock. Also, clearly illustrated: the more dramatic the shock, the more challenging the recovery.

Average growth for sub-Saharan Africa is expected to reach about 3.1 percent in 2018, up from 2.7 percent in 2017. But the overall picture for sub-Saharan Africa hides a range of different experiences.

Key to the tale is the degree of dependence on commodities.

Prior to 2014, the region enjoyed a sustained period of strong growth (averaging 5.6 percent during 2000–13) thanks to deep structural reforms and highly supportive external conditions. Since the 2014 commodity shock, life has been difficult for many countries. Regional growth dipped to 1.4 percent in 2016—the lowest level in more than two decades.

Different countries experienced the shock and subsequent recovery very differently. Most oil exporters—countries like Angola and Nigeria—fell into recession after 2014—resulting in a dramatic “V-shaped” dip in the chart. Conditions in other resource-intensive countries, such as Ghana, South Africa and Zambia were also difficult due to a fall in energy and metal prices, and policy uncertainty.

Since then, the slight upward tilt of the line graph illustrates that resource-intensive countries have seen some pickup but still below levels attained prior to 2014. The growth momentum has improved most notably for oil exporters, mainly in Nigeria, while remaining subdued in South Africa. Meanwhile, a few countries continue to deal with security problems which are imposing a severe human and economic toll. One-third of the population of sub-Saharan Africa lives in countries where GDP per capita fell in 2017 and is expected to fall further in 2018 and 2019.

Meanwhile, non-resource-intensive countries continued to enjoy high growth—at about 6 percent on average, notwithstanding a slight dip after 2014. This was partly due to public infrastructure investment, good agricultural season, improved business environment and positive impact from lower oil prices.

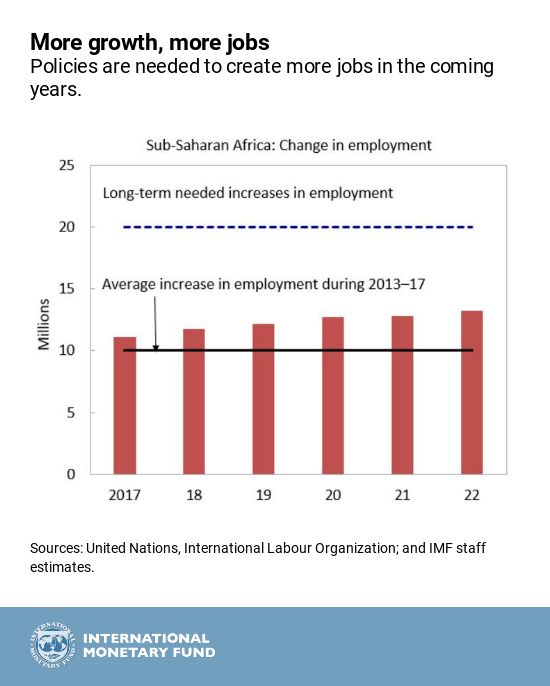

Looking ahead, again, the picture is a varied one. Over the medium term, and with current policies in place, growth is expected to improve to about 4 percent, or 1½ percent per capita—a respectable rate but not enough for the region to fully harness Africa’s demographic dividend, as illustrated in the bar chart below. The region needs to raise growth to create the additional 20 million jobs per year needed to absorb new entrants to labor markets.

In general, most economies in sub-Saharan Africa are projected to grow far below the rates expected in countries from other regions at similar levels of per capita income. This is the case for several large economies, including Nigeria and South Africa, which are expected to see their real per capita income fall or stagnate over the medium term.

In contrast, several countries including Ethiopia, Senegal, and Tanzania, are poised to see their per capita income rise faster than would be expected given their level of income due in part to strong public investment.

Shielding the recovery and creating enough jobs for the region to fully harness its demographic dividend will require strong, sustainable, and inclusive growth. Achieving this will, in turn, demand policies to strengthen resilience and facilitate the reallocation of labor and capital into more productive sectors.