People are becoming concerned that the rising power of big successful companies may be behind some of the recent sluggish economic growth and rising income inequality.

Are these concerns justified? Our research in Chapter 2 of the April World Economic Outlook looks at this question using data for nearly 1 million companies from 27 advanced and emerging market economies since the early 2000s.

We find that rising corporate market power has had a fairly limited negative economic impact so far. But, if left unchecked, it could take a bigger toll on growth and people’s incomes in the future. Policymakers need different policies to keep market competition strong.

The overarching policy goal should be to ensure a level playing field among all companies.

Rise in market power

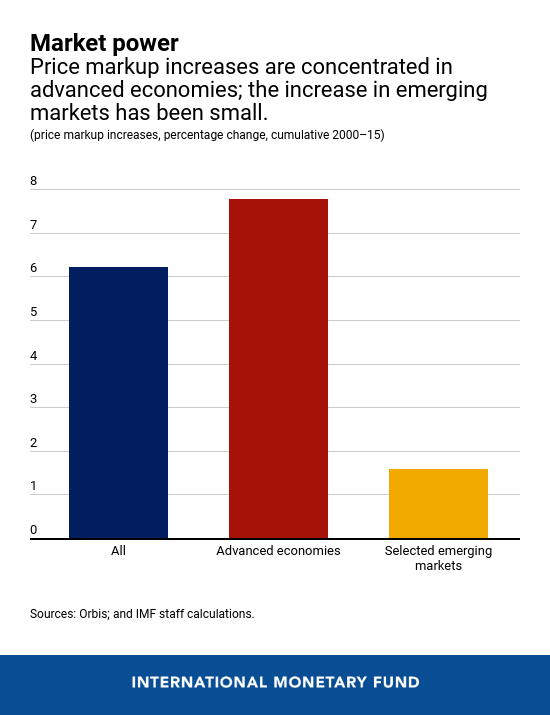

While market power is often associated with rising concentration and the surge of corporate giants in industries like pharmaceuticals or high-tech, a better indicator is the so-called price markup—how much a company charges for its products compared with how much it costs to produce, expressed as a ratio. By this metric, we find that firms’ average markup has increased, although moderately—by close to 8 percent in advanced economies since 2000, but by less than 2 percent in those emerging economies covered by the analysis.

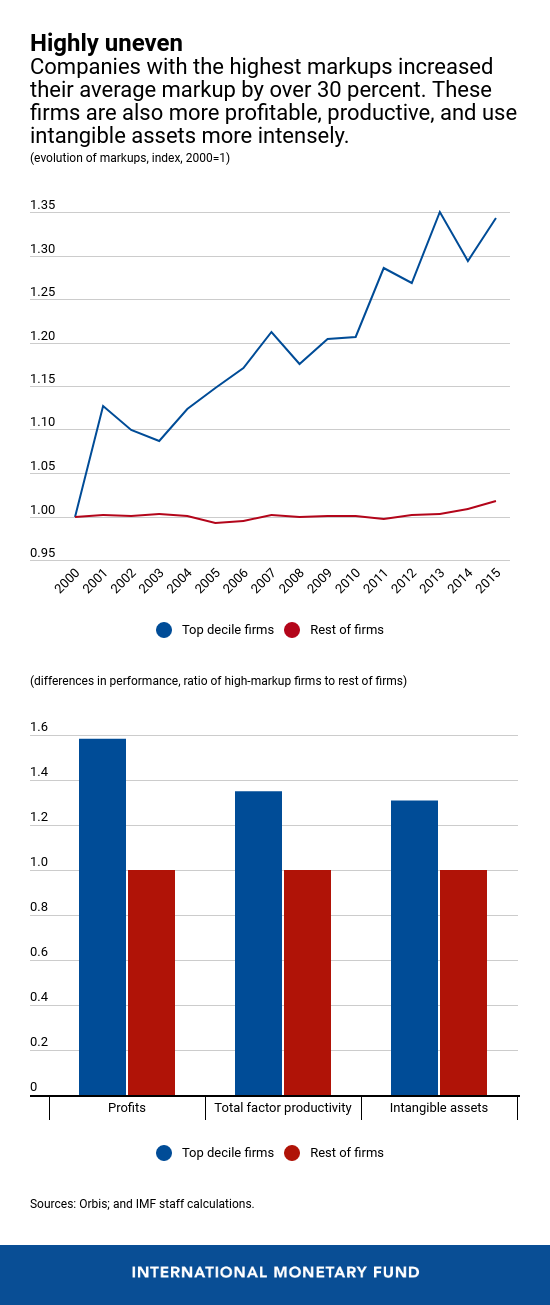

This increase has taken place in most industries, with the largest among nonmanufacturing companies and in those that use digital technologies most intensely. But within industries, higher markups have been concentrated among a small fraction of companies.

Companies with the highest markups (in the top 10 percent) raised theirs by over 30 percent since 2000, while markups have been largely flat among the remaining 90 percent.

These high-markup companies vary in size but perform better than others. On average, they are about 50 percent more profitable, over 30 percent more productive, and use 30 percent more intangible assets (like patents or software) than others. Most of the high-markup companies are rather small—they can dominate niche markets, for example—but the larger ones in the group account for most of the group’s total sales.

The role played by a small fraction of better-performing companies in driving up markups across a wide range of advanced countries and industries points to common underlying forces.

One such force is the so-called “winner-takes-most” dynamic. In many markets, the rising market power of the more productive and innovative companies has been helped by their superior ability to exploit proprietary intangible assets, network effects, and economies of scale (reduced costs per unit as output increases). In the United States, for example, these high-markup companies have also expanded in size in relation to their low-markup counterparts, contributing to a larger increase in aggregate markups compared with Europe.

Worrisome trends

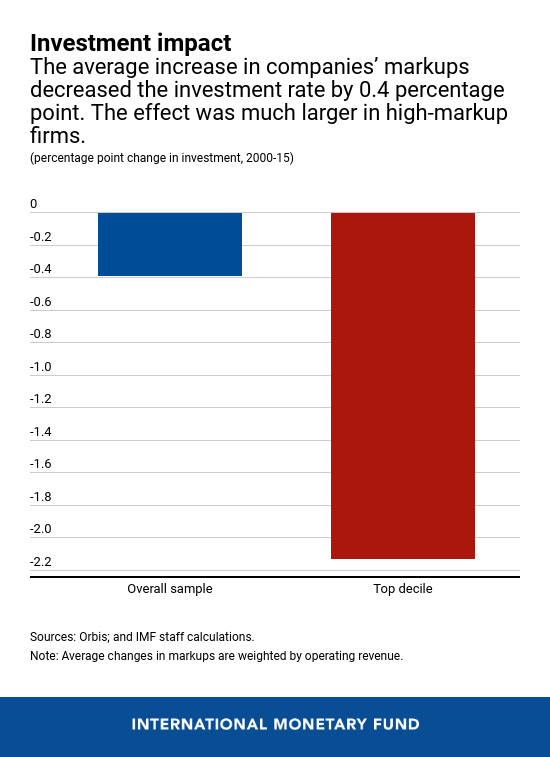

Our study finds that, since the early 2000s, rising markups have contributed to some reduction in companies’ investment—a key ingredient to sustained growth. As a company’s market power increases, it can widen its profits by charging a higher price and reducing its output. This, in turn, leads the company to reduce its demand for capital and, therefore, its investment. This effect was large for those companies whose markups increased the most, but more moderate for the group of advanced economies.

We estimate that if markups had remained at their 2000 levels, the stock of capital goods today would be on average about 3 percent higher and GDP about 1 percent higher. By reducing investment, rising market power weakened aggregate demand and, thereby, also amplified slightly the impact of the 2008 financial crisis.

Increased market power since 2000 has also accounted for at least 10 percent of the overall decline (0.2 out of 2 percentage points) in the share of national income paid to workers in advanced economies. This has contributed to greater earnings inequality between workers since rising capital income tends to mostly benefit high-income individuals.

Policies to strengthen competition

Policymakers need to act for two reasons.

First, while the macroeconomic effects described above have been rather modest so far, they could become increasingly negative if the rise in market power were left unchecked. This is because, in addition to further declines in investment and the labor income share, another negative impact could kick in: beyond a certain threshold, greater market power would stifle innovation, as firms’ incentives to separate themselves from competitors through innovation would become too weak.

Second, the role of technological forces in driving up market power does not mean policymakers should stay inactive. Any weakening of pro-competition policies could amplify winner-takes-most dynamics, and companies that have achieved market dominance primarily through innovative products and business practices may attempt to entrench their positions by erecting barriers to entry, such as high customer switching costs.

The overarching policy goal should be to ensure a level playing field among all companies, including possible new ones, particularly in nonmanufacturing industries where markups have increased the most. This means lowering domestic barriers to entry (for example, by reducing administrative burdens on start-ups) and reducing barriers to trade and foreign direct investment in services. Other measures include strengthening some features of competition law and policies—such as the role of market examinations—reforming corporate taxes so as to tax the excess returns on capital derived from market power, and ensuring that intellectual property rights encourage groundbreaking innovations more than incremental ones.

Watch a conversation with the authors: