Credit (ohoto: Metamorworks/iStock by Getty Images)

Credit (ohoto: Metamorworks/iStock by Getty Images)

Credit (ohoto: Metamorworks/iStock by Getty Images)

Credit (ohoto: Metamorworks/iStock by Getty Images)

“It’s awful. Why did nobody see it coming?” asked Queen Elizabeth II in November 2008 during a visit to the London School of Economics, wondering why nobody had predicted the Global Financial Crisis. The bewilderment wasn’t unique to the British monarchy; across the world, many asked the same question.

Ten years on, it remains difficult to forecast financial instability. However, progress is afoot to improve the understanding of important links between the financial sector and the economy. We now understand better how financial vulnerabilities can amplify negative shocks and hurt output and employment.

Twice a year, the IMF comes out with its latest analysis of global financial stability risks in the Global Financial Stability Report, where it continues to initiate improvements in a framework for financial stability monitoring.

The current approach, described in a new IMF paper, involves a systematic assessment of financial vulnerabilities for financial firms and markets, and business, household and government borrowers, and a summary financial stability risk measure in terms of forecast GDP growth depending on financial conditions. The two-part approach enhances transparency and provides a path to better communication among financial regulators and central banks, and ultimately policymaking.

We now understand better how financial vulnerabilities can amplify negative shocks and hurt output and employment.

How it works

In the framework, cyclical financial stability risks go up as lenders and borrowers increase risk-taking in response to loose financial conditions. Greater collective risk-taking leads to a buildup of financial vulnerabilities, such as high borrowing or maturity mismatch of financial firms. Vulnerabilities will amplify shocks and lead to tighter financial conditions and reduce economic growth. This process is mutually reinforcing as vulnerable financial firms are forced to reduce their debt when asset prices fall, leading to further declines in asset prices and economic growth.

The first part of the current approach involves a “bottom-up” monitoring matrix of indicators, defined by types of vulnerabilities across types of lenders and borrowers in the financial system. Financial vulnerabilities include inflated asset valuations; greater leverage and funding mismatches of banks and other financial firms; and greater indebtedness among nonfinancial borrowers, including households, businesses, and governments.

The chart below shows this matrix in a graphic form, including snapshots of the degree of vulnerabilities for lenders and borrowers at different points in time. It illustrates the high vulnerabilities of banks and nonbank financial firms globally and the high indebtedness of households in many countries at the time of the crisis, and the substantially stronger positions now. Over time, this matrix may evolve as the monitoring framework should adapt to capture vulnerabilities that may emerge in new forms.

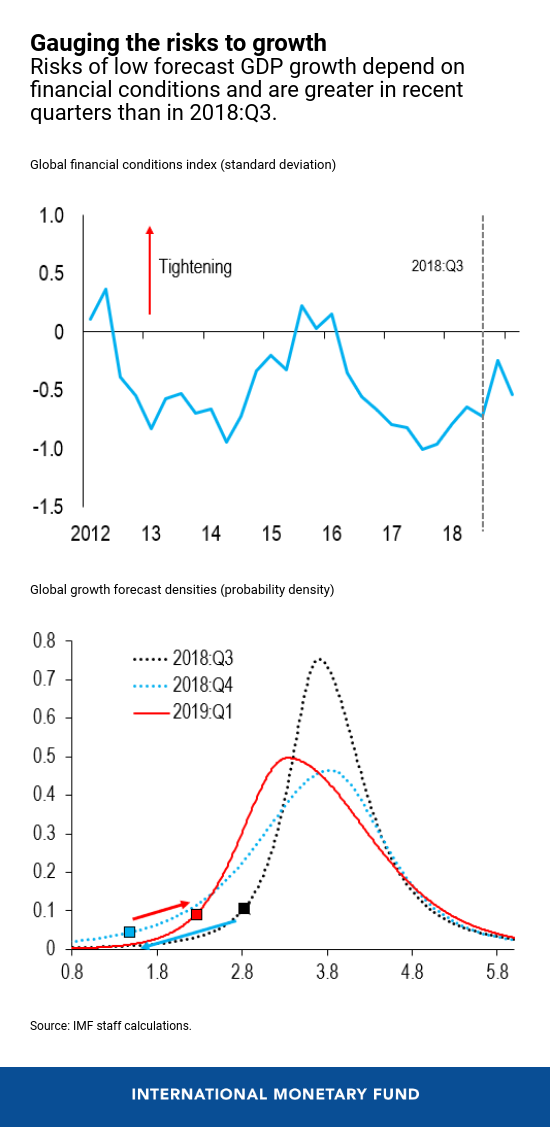

The second part of the approach is a “top-down” summary measure of financial stability risk—“Growth at Risk” or GaR—measured by downside risks to projected GDP growth depending on financial conditions. The key innovation of GaR is that the entire distribution of forecast GDP growth is linked to financial conditions, which capture the underlying price of risk in the economy.

In other words: When forecasting GDP growth, think in terms of probabilities. It is important to consider not only expected growth but risks to expected growth.

The chart below shows how the probability distribution of forecast global GDP growth shifts in reaction to financial conditions at three different points in time. Global financial conditions for the two quarters before the April 2019 GFSR were tighter than in 2018:Q3 and, as a result, the downside risks to forecast year-ahead GDP growth increased somewhat.

In addition, while looser financial conditions can raise growth and reduce volatility in the near term, they can increase volatility in the medium term because vulnerabilities build up in response to looser financial conditions. This is the so-called volatility paradox. Work is ongoing to incorporate vulnerabilities to estimate GaR.

Measuring financial stability risks for policymaking

The two parts of this approach are complementary. GaR provides a summary indicator of financial stability risks, which can be compared directly to historical levels of risk to judge the severity of potential downsides. The more granular monitoring of various specific vulnerabilities provides necessary nuance and depth to GaR estimates and highlights potential targets for macroprudential policies.

The monitoring framework could lead to more and better indicators of financial conditions and vulnerabilities that could be used to estimate GaR for the global economy, regions, or countries. In other words, it could be useful for both multilateral and bilateral surveillance by the IMF.

The new framework also supports monitoring of macroprudential policy implementation across countries to mitigate financial stability risks. The IMF has launched a new annual survey on the use of macroprudential policies, and policies can be mapped to the financial vulnerabilities in the matrices.

In terms of the Queen’s question, this monitoring framework would have allowed us to tell her that, if the vulnerabilities that were identified were left unaddressed, a severe financial crisis was likely, even if we could not tell her when that might happen. Looking ahead, it formalizes regular systematic assessments of financial stability risks and provides a summary measure of these risks in terms of output growth. It thus allows financial stability risks to be incorporated into decision-making frameworks for monetary policy and regulatory policy, rather than only intermittently when financial risks are already very high.