The global economic and financial outlook has improved in the last six months. Inflation has fallen, financial conditions have eased, and risks to the outlook are balanced. However, many countries continue to struggle with high public debt and fiscal deficits amid new challenges from high real interest rates and dimming medium-term growth prospects.

Our latest Fiscal Monitor calls for governments to avoid slippages and focus more on rebuilding buffers and safeguarding fiscal sustainability over the medium term.

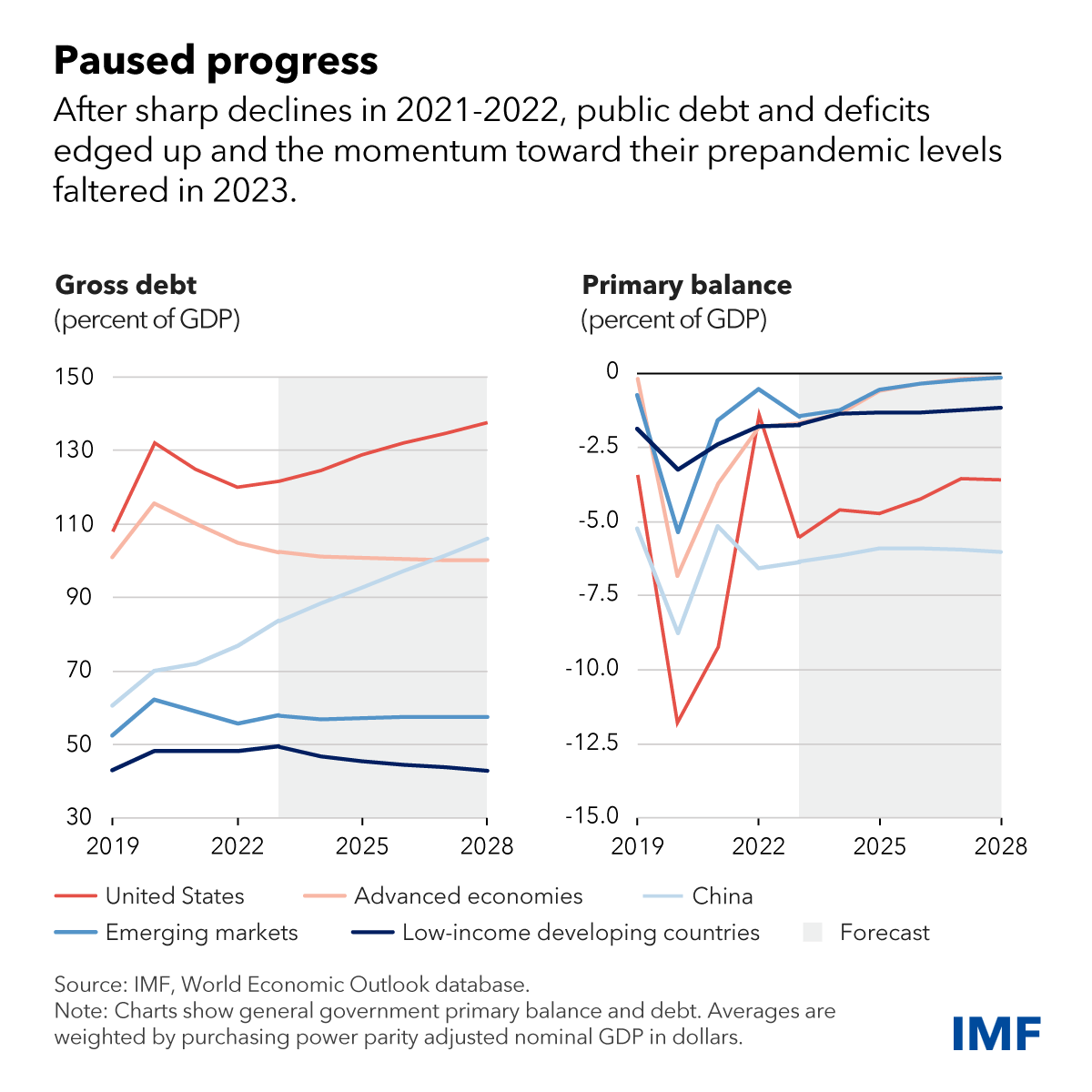

Fiscal policy shifted to be more expansionary last year after a rapid improvement in debt and deficits in the prior two years. Only half of the world’s economies tightened fiscal policy last year, down from about 70 percent in 2022.

Four years after the start of the pandemic, public spending, excluding interest payments, remained about 3 percentage points of gross domestic product above prepandemic projections in advanced economies, excluding the United States, and 2 percentage points above them in emerging market economies, excluding China. This spending level reflects the slow unwinding of crisis-era fiscal policies and the introduction of new support measures, alongside new industrial policy measures including subsidies and tax incentives. Higher nominal interest rates pushed up interest payments in most economies.

Global public debt edged up to 93 percent of GDP in 2023 and remained 9 percentage points above the prepandemic level. The increase was led by the two largest economies, United States and China, where debt rose by over 2 and 6 percentage points of GDP respectively.

These two economies also shape global fiscal developments and outlook. Slowing growth in China could weigh on global growth and trade, posing fiscal challenges for countries with strong trade and investment linkages. High and volatile government bond yields in the United States would lead to tighter financing conditions in the rest of the world.

Moderate fiscal tightening is expected to resume this year, but significant uncertainty remains.

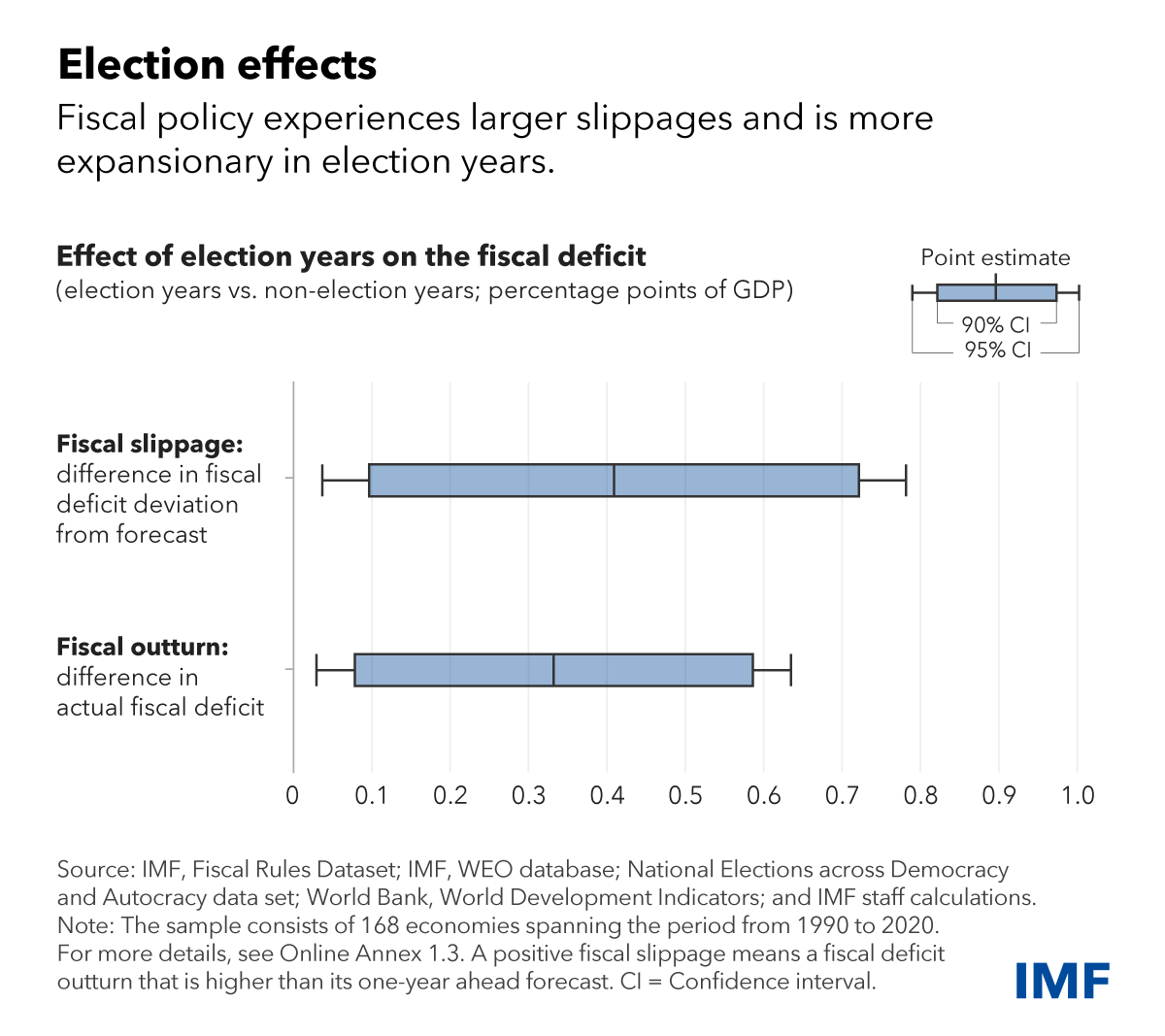

In 2024, a record number of countries, home to more than half of the world’s population, are holding national elections. History shows governments tend to spend more and tax less during election years. Deficits in election years tend to exceed forecasts by 0.4 percentage points of GDP, compared to non-election years. In this great election year, governments should exercise fiscal restraint to preserve sound public finances.

While we project modest fiscal tightening over the medium term, it will be insufficient to stabilize public debt in many countries. Our chapter shows that, under current policies, primary deficits—which exclude interest expenses—will remain above debt-stabilizing levels in 2029 in about a third of advanced and emerging market economies and in almost a quarter of low-income developing countries. The size of necessary further adjustments varies. The required average reduction in primary deficits is particularly large for emerging markets with rising public debt-to-GDP ratios in our projections. We estimate it at 2.1 percentage points of GDP. The country groups in this paragraph include the two largest economies—the United States and China—in the appropriate aggregate.

Without further efforts, the return of fiscal policy to its prepandemic normal may take years. Spending pressures to address structural challenges—including demographic and green transitions—are becoming more pressing, while slowing medium-term growth prospects and high real interest rates are likely to further constrain fiscal space in most economies.

Countries need decisive efforts to safeguard sustainable public finances and rebuild fiscal buffers. The pace of consolidation should be calibrated depending on fiscal risks and macroeconomic conditions that each country faces. Countries will need to act resolutely in cases where sovereign risks are elevated and fiscal credibility is lacking.

Governments should immediately phase out legacies of crisis-era fiscal policy, including energy subsidies, and pursue reforms to curb rising spending while protecting the most vulnerable. Advanced economies with aging populations should contain spending pressures for health and pensions through entitlement reforms and other measures.

Revenue should keep up with spending over time. In advanced economies, targeting excessive profits as part of the corporate income tax system could further bolster revenues. Emerging market and developing economies could raise their tax revenue potential by broadening tax bases, improving the design of their tax systems, and strengthening revenue administration. Such measures could, in ideal circumstances, yield as much as an additional 9 percent of GDP, our research shows.

The foundations for sound and sustainable public finances require a medium-term approach to budgetary planning and execution. All countries can benefit from enhanced transparency of public finances and greater use of modern technology, known as GovTech. For countries in severe debt distress, orderly and timely debt restructuring is important. Continued international cooperation, including through the Group of Twenty Common Framework and the Global Sovereign Debt Roundtable, is crucial to facilitate an efficient debt restructuring process.

—This blog is based on Chapter 1 of the April 2024 Fiscal Monitor.