Dislocations from the pandemic, geoeconomic fragmentation, and Russia’s war in Ukraine have shifted world trade dynamics. While this has created challenges, the redirection of trade has also generated new opportunities, particularly for the Caucasus and Central Asia.

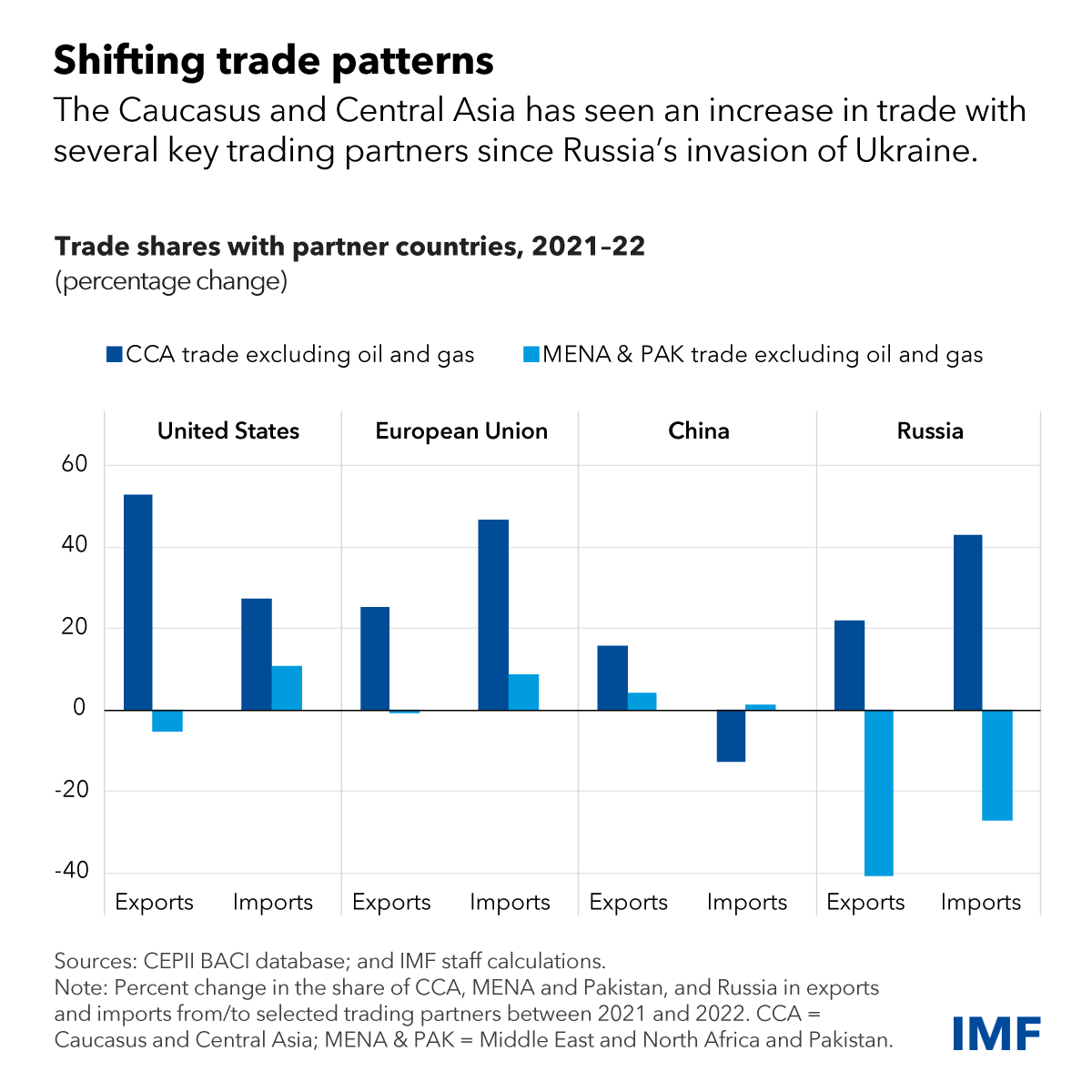

Since the war began, the region’s economies have shown continued resilience and trade activity in many countries has surged, fueled in part by alternative trade routes. In 2022, Armenia, Georgia, and the Kyrgyz Republic saw their share of trade excluding oil and gas with major partners such as China, the European Union, Russia, and the United States rise as much as 60 percent. Hence, despite some moderation, gross domestic product growth in the Caucasus and Central Asia is projected to remain robust at 3.9 percent in 2024 before picking up to 4.8 percent in 2025.

Trade volumes between China and Europe via Central Asia have more than quadrupled. Though this route, known as the Middle Corridor, represents a small fraction of overall trade between China and Europe, it holds significant promise for economic development in the Caucasus and Central Asia and its integration into global supply chains.

Shifting trade patterns have also opened opportunities elsewhere. For example, countries in the Middle East and North Africa, such as Algeria, Kuwait, Oman, and Qatar, roughly doubled their energy exports to the European Union in 2022–23 to meet surging demand for non-Russian oil and gas.

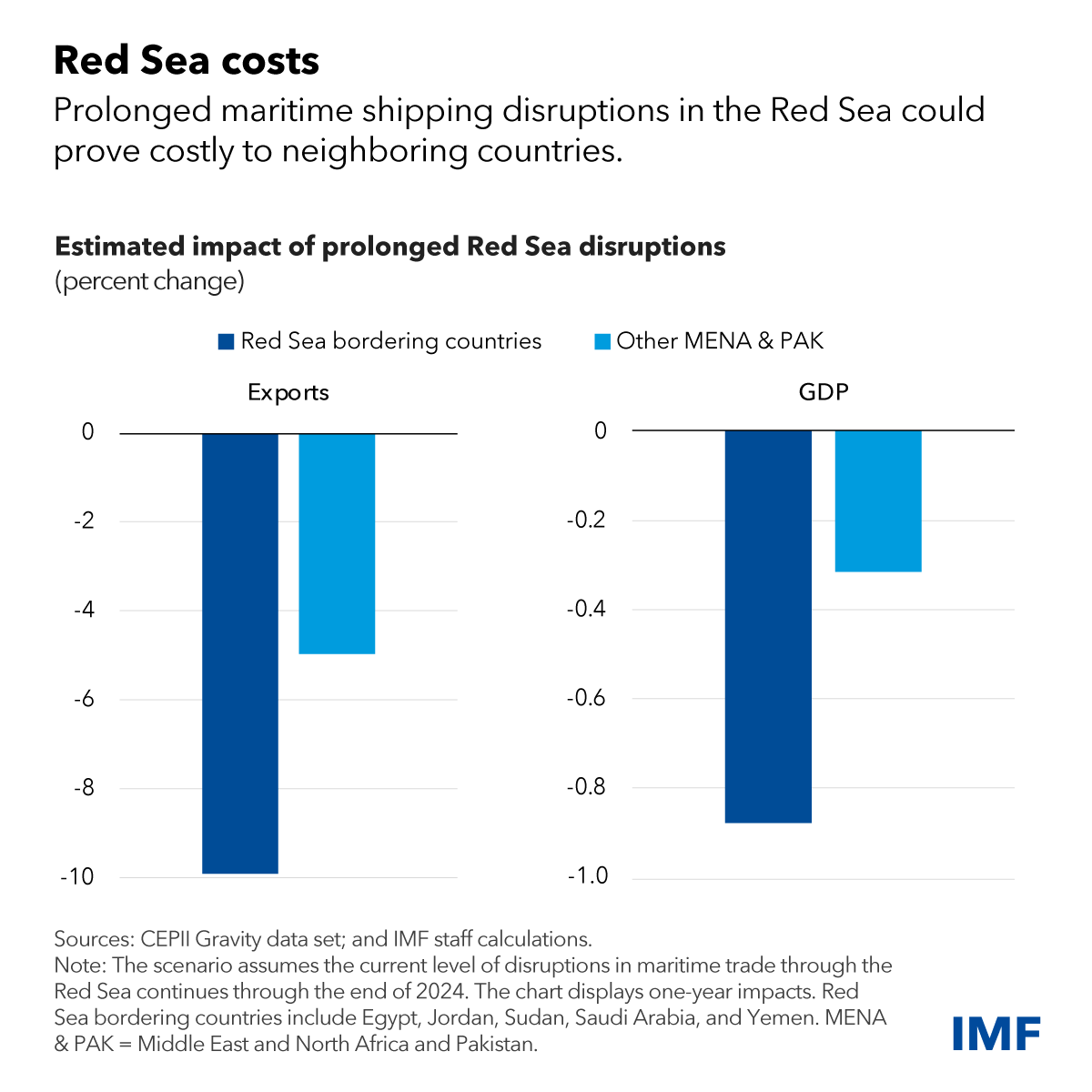

More recently, Red Sea shipping attacks stemming from the conflict in Gaza and Israel have not only disrupted maritime trade and impacted neighboring economies but also increased the level of uncertainty. Suez Canal transits are down more than 60 percent since the conflict in Gaza and Israel began as ships are rerouted around the Cape of Good Hope. Cargo volumes also have contracted sharply in Red Sea ports such as Jordan’s Al Aqaba and Saudi Arabia’s Jeddah. However, some trade has been redirected within the region, including to Dammam, Saudi Arabia, on the Persian Gulf.

Persistent Red Sea disruptions could have sizable economic consequences for the most exposed economies. An illustrative scenario in our most recent Regional Economic Outlook shows that countries on the Red Sea (Egypt, Jordan, Saudi Arabia, Sudan, Yemen) could lose about 10 percent of their exports and close to 1 percent of GDP on average if disruptions continue through the end of this year.

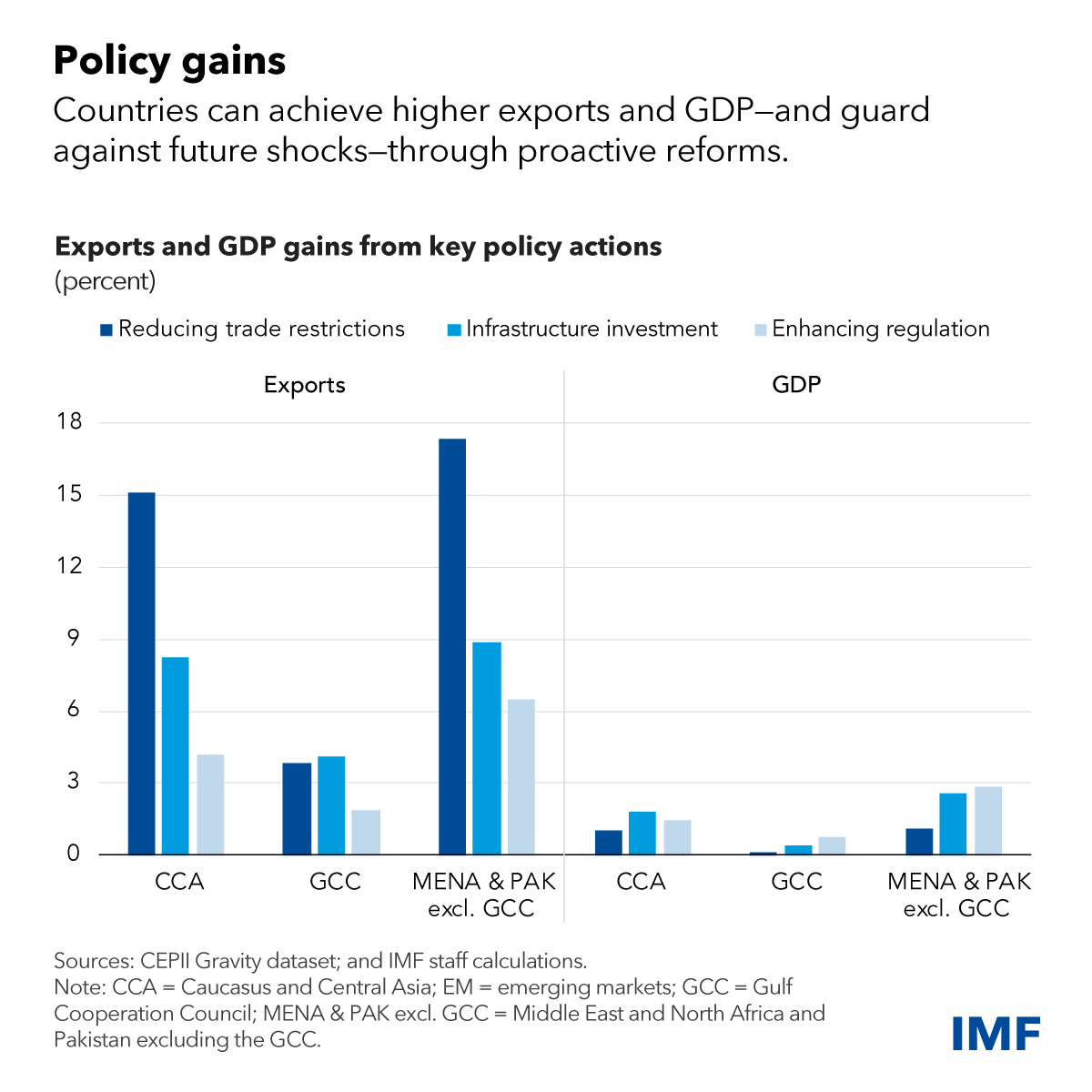

In the current uncertain landscape of international trade, strategic foresight and proactive policy reforms will be the key factors enabling countries to achieve trade and income gains. Addressing the challenges posed by these shocks and seizing the opportunities ahead will require that countries tackle longstanding trade barriers arising from elevated nontariff restrictions, infrastructure inadequacies, and regulatory inefficiencies.

Targeted policy reforms can help do this, though preparation is crucial. Reducing nontariff trade barriers, boosting infrastructure investment, and enhancing regulatory quality could help increase trade by up to 17 percent on average over the medium term, our research shows, while economic output could be 3 percent higher. This would also enhance resilience against future trade shocks.

Past reforms show effective action is possible. Uzbekistan has enhanced its attractiveness to foreign investors and deepened its integration into the global economy eliminating currency controls and improving the business environment. Saudi Arabia grew its non-oil economy and attracted international businesses through its Vision 2030 reform plan, which included easing regulatory constraints on trade and investment. Azerbaijan’s investment in the Baku-Tbilisi-Kars railway, a key segment of the Middle Corridor, highlights the potential of infrastructure investment, increasing cargo capacity between Asia and Europe. These initiatives underscore the transformative power of targeted policy reforms in adapting to and thriving within the global trade landscape.

Countries in the Middle East and North Africa can mitigate ongoing shipping disruptions by improving their supply chain management, securing new suppliers in the most affected sectors, seeking alternate shipping routes, and assessing air freight capacity needs. In the medium term, countries can increase their resilience to trade disruptions by strengthening and expanding regional linkages and connectivity. In turn, investing in transportation infrastructure, including by developing innovative sea–land routes, would be important.

Building a more diversified trade profile—spanning partners, products, and routes—would significantly bolster the region’s ability to withstand disruptions. Shifting trade patterns present a unique opportunity for countries to redefine their place in the global economic framework.

—This blog reflects contributions by Bronwen Brown and other staff across the Middle East and Central Asia Department. It is based on Chapter 3 of the April 2024 Regional Economic Outlook for the Middle East and Central Asia, “Trade Patterns amid Shocks and a Changing Geoeconomic Landscape.” The authors of the chapter are Apostolos Apostolou, Hasan Dudu, Filippo Gori, Alejandro Hajdenberg, Thomas Kroen, Fei Lui, and Salem Mohamed Nechi.