Versions in عربي (Arabic), and Español (Spanish)

In December 2016, the U.S. Fed raised interest rates for the first time in a year, and said they planned more increases in 2017. Emerging market currencies took a bit of a dive, but overall investors didn’t overreact and run for the doors with their money. For the bigger picture, you can read IMF Chief Economist Maurice Obstfeld’s blog that outlines how the U.S. election and Fed decision will impact the global economy.

One aspect that makes emerging markets more vulnerable is their corporations are loaded down with debt in both local and foreign currency—to the tune of roughly $18 trillion—fueled in large part by low interest rates in the United States. This debt now makes them vulnerable to the expected interest rate increases in 2017. Will firms be able to roll over their debt?

The debt balloon

The debt of nonfinancial firms in emerging markets has quadrupled over the past decade, with bonds accounting for a growing share (Chart 1). The considerable increase in corporate debt raises concerns, given the link between the rapid build-up in leverage in emerging markets and past financial crises.

Our new paper suggests that:

- Debt accumulation was more pronounced for firms which are more dependent on external financing. Likewise, relative to other types of firms, small and medium-sized enterprises disproportionately increased their leverage.

- The impact of U.S. monetary policy on debt growth was greater for sectors that are more heavily dependent on external funding in financially open emerging markets with relatively more rigid exchange rate regimes.

- Global financial conditions affected emerging market firms’ growth in debt in part by relaxing corporate borrowing constraints.

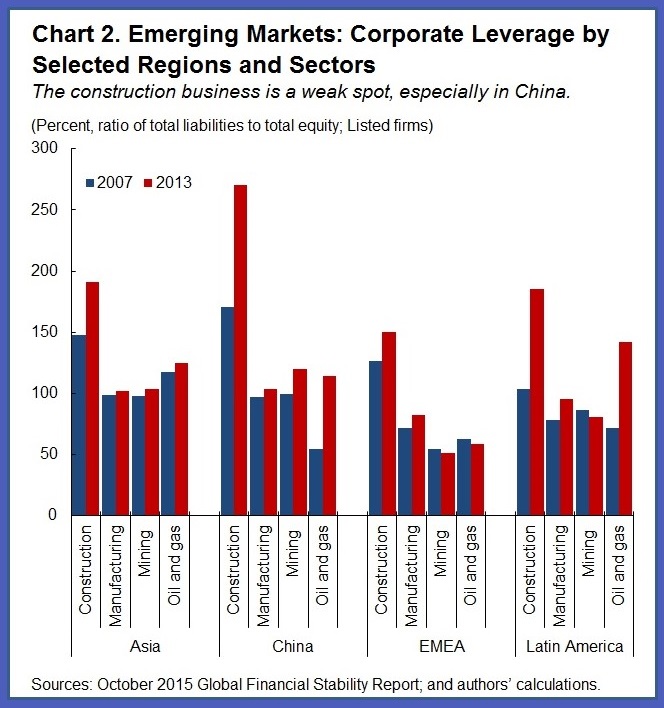

Where is debt highest

Corporate debt in emerging markets has climbed faster in more cyclical sectors, with the greatest growth seen in construction (Chart 2). The striking increase in leverage within the construction sector is most notable in China and Latin America. In addition, firms that took on more debt have, on average, also increased their foreign exchange exposures.

Readers can stay tuned for more details on emerging markets and the global economy when the IMF releases the update to the World Economic Outlook on January 16.