|

Transcript of a Tele-Conference Press Briefing on "U.S. Fiscal Policies and Priorities for Long-Run Sustainability," an Occasional Paper by the IMF January 7, 2004 United States and the IMF IMF Staff Report on U.S. 2003 Article IV Consultation, August 2003 IMF Report on U.S. Fiscal Transparency, August 2003 Other Titles in the Occasional Paper Series | |

| |

Long-Run Sustainability Martin Mühleisen and Christopher Towe, Editors ©2004 International Monetary Fund January 7, 2004 Order information for full text in hard copy (abstract below)

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

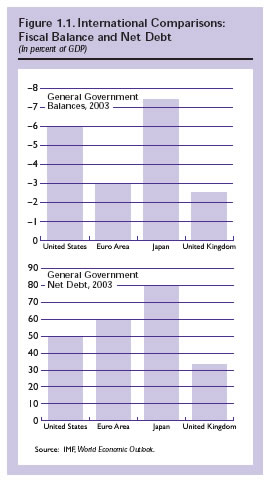

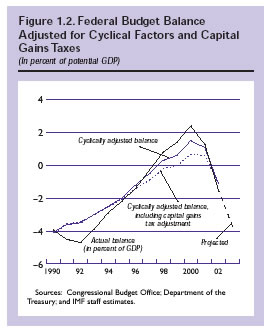

I. Overview: Returning Deficits and the Need for Fiscal ReformU.S. government finances have experienced a remarkable turnaround in recent years. Within only a few years, hard-won gains of the previous decade have been lost and, instead of budget surpluses, deficits are again projected as far as the eye can see. The deterioration has not been restricted to the federal budget but has also taken place at the state and local government levels. As a result, the U.S. general government deficit is now among the highest in the industrialized world, and public debt levels are approaching those in other major industrial countries (Figure 1.1). Although fiscal policies have undoubtedly provided valuable support to the recovery so far, the return to large deficits raises two interrelated concerns. First, with budget projections showing large federal fiscal deficits over the next decade, the recent emphasis on cutting taxes, boosting defense and security outlays, and spurring an economic recovery may come at the eventual cost of upward pressure on interest rates, a crowding out of private investment, and an erosion of longer-term U.S. productivity growth. Second, the evaporation of fiscal surpluses has left the budget even less well prepared to cope with the retirement of the baby boom generation, which will begin later this decade and place massive pressure on the Social Security and Medicare systems. Without the cushion provided by earlier surpluses, there is less time to address these programs' underlying insolvency before government deficits and debt begin to increase unsustainably, making more urgent the need for meaningful reform. The remainder of this section summarizes the IMF staff's assessment of the U.S. fiscal situation,describing both the factors that have contributed to the burgeoning of the deficit and the key policy challenges posed by the impending demographic transition. It ties together subsequent sections on domestic and international implications of current budget policies; long-term prospects for Social Security and Medicare; an intergenerational analysis of long-term fiscal imbalances; the role of energy taxation; effectiveness of spending rules; and state and local government finances. The Fiscal Deficit: Back to Square OneThe 1990s were marked by significant fiscal consolidation as the economy emerged from the 1991 recession and experienced one of the longest expansions in recent history. As a result, following many years of failed attempts at exerting fiscal discipline, the federal budget—including the Social Security surplus—moved from a deficit of 4½ percent of GDP to surpluses that reached 2½ percent of GDP in FY2000 (Figure 1.2).1 Both macroeconomic developments and policy actions played an important role in achieving this correction. Strong economic growth buoyed tax revenues, and the stock market boom fueled an unprecedented increase in capital gains taxes. Estimates by the Congressional Budget Office (CBO, 2003) suggest that cyclical factors accounted for about 4 percent of GDP of the fiscal improvement between FY1992 and FY2000, just over half the shift in the deficit ratio (see Figure 1.2).2 The balance was achieved through tax increases—including those incorporated in the 1993 Omnibus Budget Reconciliation Act—and the discipline over both mandatory and discretionary spending exerted by the 1990 Budget Enforcement Act.3 Since FY2000, however, the fiscal position has eroded rapidly and, with the deficit expected to exceed 4 percent of GDP in FY2004, essentially all the gains achieved during the earlier decade have disappeared. Again, as Table 1.1 shows, the reasons for this shift include both cyclical and policy factors:4

The major tax cuts (as well as some spending measures) enacted in 2001 and 2003 have been estimated to have cost roughly $1.7 trillion over FY2002–FY2011. However, substantial debate and uncertainty have surrounded these cost estimates, largely reflecting the complicated and nontransparent manner in which the measures have been enacted. For example, some measures are only effective for a short period, while others—such as the elimination of the estate tax—are being phased in so that the fiscal cost will rise in the coming years. Moreover, all tax measures are subject to sunset clauses, which will mean that rates and deductions will—in the absence of policy action—return to pre-2001 levels in 2011 at the latest. However, it is the administration's stated intention to make the tax cuts permanent, which would leave the federal budget deficit roughly 2 percent of GDP above its baseline level by FY2013. Costs and Consequences of Tax Cuts and DeficitsThe sharp erosion in the fiscal position and the recent emphasis on tax cuts have revived a long-standing debate about the extent to which fiscal deficits crowd out private investment, and whether tax cuts, by improving economic incentives, can significantly boost the economy's supply side. The current administration has played an active role in this debate.6 It has emphasized that tax cuts would carry important longer-run supply-side benefits that could help mitigate their budgetary cost. The administration has also stressed that the federal deficit and debt-to-GDP ratios that are projected over the coming 5–10 years are "manageable" and remain well below the peak levels recorded in the 1980s and early 1990s. There is little doubt that significant macroeconomic gains could be reaped from reforms of the U.S. tax code, with the Council of Economic Advisers (CEA, 2003) citing estimates of potential gains in the range of 2–6 percent of GDP. The tax system places a disproportionate burden on personal and corporate incomes, compared with a consumption-based tax system, discourages labor market participation and saving, and is, hence, economically less efficient. The administration's 2003 proposals were viewed as a significant move toward a consumption-based tax system, because the initial package of measures announced in February would have lowered marginal income tax rates, eliminated the double taxation of dividends, and significantly expanded the extent to which income earned on saving would have been tax free. Moreover, tax reform that simplified the system could also yield significant gains, given that the multitude of tax deductions and exemptions have imposed considerable administrative and other costs. As noted in CEA (2003), taxpayers are required to spend roughly 3 billion hours a year dealing with federal tax matters, and overall compliance costs are estimated at around 10 percent of total federal tax revenues.It remains an open question whether the tax cuts adopted since early 2001 will have significant supply-side benefits: Although the cuts in income tax rates will—at the margin—improve incentives to work, the labor participation rate is already high, and empirical studies do not suggest that it is highly tax elastic (Angrist, 1991; Blundell, Duncan, and Meghir, 1998).7

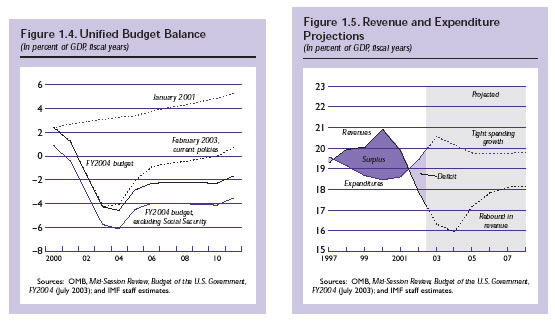

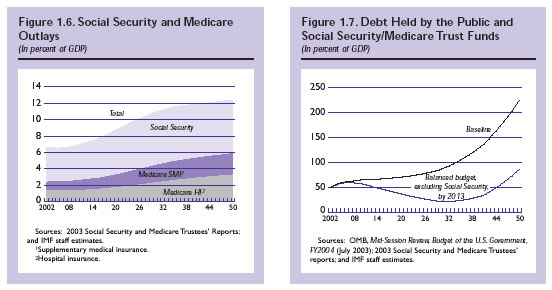

The modest efficiency gains that might arise from the recent tax cuts will also have to be weighed against the effects of a prolonged period of fiscal weakness. As shown in Figure 1.4, the FY2004 budget is expected to result in deficits well into the next decade—a substantial deterioration compared with the January 2002 current services baseline, which saw a return to budgetary surpluses around 2007.Although the deficit ratio is expected to narrow somewhat as the economy recovers in coming years, there are important reasons to worry that these projections may still prove optimistic (Figure 1.5). The strict limits on discretionary spending that have been assumed may be difficult to sustain, especially because of pressures to increase outlays on defense and homeland security, as yet undefined supporting policies for ensuring that limits on other discretionary programs are adhered to, and reduced pressure to maintain spending discipline as a result of the expiration of the Budget Enforcement Act (BEA).8 Also, there are significant uncertainties about tax revenue projections. Notably, the official budget projections do not take into account the costs of reforming the Alternative Minimum Tax (AMT), and are predicated on the assumption that the recent (and still not fully understood) sharp drop in personal tax revenue will be largely reversed.9 With U.S. fiscal deficits expected to persist into the foreseeable future, will any supply-side benefits be outweighed by the effect of weaker public saving on interest rates and investment? The Council of Economic Advisers (2003) argued strongly that these potential offsetting effects would be minimal. However, the estimates surveyed in Section II generally suggest that the short-term stimulus stemming from the FY2004 budget proposals is likely to wane in several years, with higher deficits beginning to crowd out private investment and dampen output thereafter. In one simulation, for example, the tax cuts would eventually lower U.S. productivity—in terms of labor output per hour—by ½ percent in the long run. Global IssuesAlthough U.S. fiscal policy has undoubtedly provided valuable support to the global economy in recent years, large U.S. fiscal deficits also pose significant risks for the rest of the world. Simulations reported in Section II suggest that a 15 percentage point increase in the U.S. public debt ratio projected over the next decade would eventually raise real interest rates in industrial countries by an average of ½–1 percentage point. Higher borrowing costs abroad would mean that the adverse effects of U.S. fiscal deficits would spill over into global investment and output. Moreover, against the background of a record-high U.S. current account deficit and a ballooning U.S. net foreign liability position, the emergence of twin fiscal and current account deficits has given rise to renewed concern. The United States is on course to increase its net external liabilities to around 40 percent of GDP within the next few years—an unprecedented level of external debt for a large industrial country (IMF, 2003b). This trend is likely to continue to put pressure on the U.S. dollar, particularly because the current account deficit increasingly reflects low saving rather than high investment. Although the dollar's adjustment could occur gradually over an extended period, the possible global risks of a disorderly exchange rate adjustment, especially to financial markets, cannot be ignored. Episodes of rapid dollar adjustments failed to inflict significant damage in the past, but with U.S. net external debt at record levels, an abrupt weakening of investor sentiments vis-à-vis the dollar could possibly lead to adverse consequences both domestically and abroad.10 Long-Run Insolvency of Social Security and MedicareFrom a long-term perspective, higher U.S. fiscal deficits are especially worrisome because of the precarious financial position of the Social Security and Medicare systems. Although U.S. demographics compare relatively favorably with most other industrialized nations (see discussion in Section III), both systems are projected to run sizable deficits about a decade from now when the baby boom generation enters its peak retirement years, and accumulated surpluses are exhausted 10–20 years thereafter. The Social Security system is under pressure as a result of both the declining fertility rate—which (unlike in many other countries) is somewhat offset by higher immigration—and increases in longevity. As a result, the dependency ratio—the ratio of retirees to the working-age population—is projected to rise from 20 percent at present to around 40 percent by the middle of the century. This implies that payroll tax revenues will decline while social security spending is expected to roughly double as a proportion of GDP (Figure 1.6). The financial position of the Medicare and Medicaid systems is considerably worse, given the rapid growth of health care costs and the modest share of benefits that is covered by individual contributions. Medicare expenditures are projected to grow almost threefold relative to GDP over the next five decades, and considerable increases are also likely in the case of Medicaid.11 The projected sharp increase in expenditures, relative to contributions, and the rapid increase in health care costs mean that the Social Security and Medicare systems are highly under funded. Unless steps are taken to adjust contribution rates and benefits, the programs will fall into deficit in the next two decades and have to be supported by growing transfers out of the federal general fund. IMF staff simulations of the rapid increase of federal debt that would result—which are similar to those presented by the CBO and the administration's FY2004 budget—are shown in Figure 1.7. Official estimates place the net present value of the programs' unfunded actuarial liability at around 160 percent of current GDP, if measured over a 75-year horizon.12 But even these estimates understate the financial problems facing these programs because, in the absence of policy action, the programs will be running large cash flow deficits past this projection horizon. Moreover, closing the fiscal gap can be accomplished through a variety of policy measures (e.g., tax hikes, spending cuts, and so on) and at varying speed, both of which have different implications that are not captured by typical actuarial measures. These considerations have led to a renewed emphasis on estimates of the fiscal gap, which take into account longer horizons and the intergenerational transfers that are involved. Section IV presents estimates of the U.S. fiscal imbalance using an intergenerational accounting framework that encompasses the entire federal fiscal system over an infinite horizon. The results suggest that the fiscal imbalance is as high as $47 trillion, nearly 500 percent of current GDP, and that closing this fiscal gap would require an immediate and permanent 60 percent hike in the federal income tax yield, or a 50 percent cut in Social Security and Medicare benefits. The analysis also illustrates that this gap is associated with a severe intergenerational imbalance, with the burden on future generations increasing further if corrective measures are delayed. The Policy ChallengeTo restore a sustainable position, U.S. fiscal policy must refocus on two key objectives. The first is to adopt a clear and credible policy framework to achieve a balanced budget (excluding the Social Security surplus) over the cycle. The second is to pursue the reforms needed to place the Social Security and Medicare systems on a sound financial footing. Restoring Budget BalanceBalancing the budget, excluding Social Security, has been an underlying goal of U.S. fiscal policy since at least 1985, when this objective was enshrined in the Gramm-Rudman-Hollings legislation. It is also an objective that the current administration has endorsed in the past—for example, the FY2002 budget was committed to saving the entire Social Security surplus, allowing almost all outstanding federal debt to be repaid over 10 years. The focus on balanced budgets is grounded in the realization that today's Social Security surpluses represent an accumulation of contributions by program participants that need to be saved to fund future retirement benefits. With the approaching retirement of the baby boom generation, reestablishing a balanced U.S. federal deficit is becoming increasingly urgent. Achieving this objective over a 5–10-year period would leave the government debt ratio more than 10 percent of GDP lower in 2013 than at present and provide much-needed room for designing and implementing the reform of entitlement programs in advance of the demographic shock (see Figure 1.7 for an illustration). Returning to a balanced budget would also help ensure that the eventual adjustment of the U.S. current account deficit is orderly and rests on stronger national saving rather than weaker U.S. investment and growth.13 How large a fiscal adjustment would be needed to meet this objective? The CBO's August 2003 baseline suggests that the effort would need to be significant. For example, assuming that the recent tax cuts are made permanent, amendments to the Medicare system are implemented, and steps are taken to address the reform of the Alternative Minimum Tax system, the unified budget deficit would fall to around 1½ percent of GDP in 2013. This measure still includes the surplus of the Social Security Trust Fund, however, which is classified as an "off-budget" item in the U.S. fiscal accounts. Once this surplus is excluded, the budget deficit, and the measures needed for balance, would be over 3 percent of GDP.14 However, these estimates assume that extremely strict limits on discretionary spending—which keeps spending constant in real terms—are maintained for 10 years, and even larger shortfalls can be envisaged. Given the magnitude of this adjustment, it would seem likely that both revenue measures and sustained spending restraints would need to be considered. On the revenue side, allowing the tax cuts to expire would yield around 2 percent of GDP, including the associated interest saving, but any revenue effort would also need to look for opportunities to expand the tax base. Recent CBO publications have illustrated that substantial revenues could be derived from reducing corporate and personal income tax preferences—including corporate tax shelters and mortgage interest deductibility. Section V suggests that energy taxes, which are comparatively light in the United States, could help meet the administration's environmental objectives while also providing substantial support for fiscal consolidation. These measures would have to go hand-in-hand with a tightening of expenditure discipline, which weakened significantly with the emergence of surpluses in the late 1990s. In recent years, geopolitical considerations and the war on terrorism have compounded spending pressures, but these and other spending priorities will need to be weighed carefully if the adjustment burden is not to fall more heavily on the revenue side. To support efforts to rein in public spending, greater weight could be given to reintroducing and strengthening the budget rules contained in the Budget Enforcement Act (BEA), which expired in October 2002. The international and U.S. experience is that fiscal adjustment tends to be more effective if it is based on formal rules embedded in a fiscal policy framework with clearly defined medium- and long-term objectives, similar to the fiscal responsibility legislation adopted by a number of industrial countries. Such a framework—and the political consensus that would surround it—could help provide policy-makers with an appropriate basis for facing the difficult trade-offs in the period ahead. A similar conclusion has been reached by a recent IMF report on U.S. fiscal transparency, which generally praised the high degree of transparency in the United States but noted a lack of clarity in the longer-term direction of its fiscal policy (Box 1.2). Fiscal responsibility legislation could also help guard against using accounting devices that obscure the true cost of measures and lead to loss of credibility, as appears to have been the case in recent years. Section VI shows that the caps on discretionary outlays and pay-as-you-go (PAYGO) requirements contained in the BEA strongly contributed to the successful fiscal consolidation in the United States during the 1990s. Although the BEA's constraints were increasingly circumvented just prior to its expiration, Section VI suggests a range of options for further strengthening these types of budget rules.

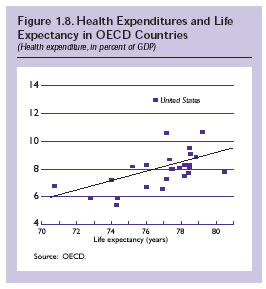

Reforming Entitlement Programs Although the impact of population aging will not be felt fully until well into the next decade, and public debt ratios are not expected to rise before 2020, the long lead times required in reforming pension and health insurance programs suggest that policy actions need to be taken well in advance. For example, the 1983 reform of the Social Security system raised the normal retirement age from 65 to 67, but to allow workers to adjust their saving and retirement plans, the increase was scheduled to be phased in over a 25-year period, beginning only in 2002. At this stage, relatively modest changes would still appear to be sufficient to close projected pension shortfalls. For example, an immediate 2 percentage point hike in the Social Security payroll tax could be sufficient to close the system's 75-year actuarial liability. However, payroll taxes in the United States are already high and further increases would tend to be regressive and could adversely affect incentives to hire labor. Other options include measures to stem the growth of benefits, including by indexing the calculation of pension benefits to the consumer price index (CPI) rather than wages, further increasing the normal retirement age, or reducing the benefits for early retirement. In general, however, the longer such decisions are delayed, the larger and more painful the required adjustments will be. Privatizing Social Security could, in principle, provide a framework for addressing the system's unfunded liability, but would still require either cuts in benefits or hikes in premiums, as well as an explicit recognition of the liabilities that the system has already accrued. Moreover, the higher returns that might be earned from personal retirement accounts would have to be weighed against the increased exposure of retirement savings to market fluctuations, which would likely require the government to still provide a minimum safety net for retirees. Questions have also been raised about the administrative costs that would have to be borne in managing small accounts, and the challenge of designing a system that discourages workers from withdrawing excessive amounts at retirement and imposing a burden on the rest of the system. Medicare reform is even more critical. The Medicare trust fund begins to run into deficit in 2016, and the unfunded actuarial liability (in net present value terms) has been estimated at 130 percent of current GDP. This raises the question of whether it would have been prudent to defer an extension of benefits, including to cover prescription drugs, until credible measures to address the system's longer-term financial problems are established. Indeed, the broader weakness of the U.S. health care system—which has left health care spending the highest among OECD countries (relative to GDP), without a commensurately high ranking in public health indicators (see Figure 1.8)—suggests that more sweeping reforms of the system may be needed. State and Federal Fiscal RelationsA review of the U.S. fiscal situation would be incomplete without considering the relatively sharp deterioration of state and local government finances in recent years. In aggregate, this sector accounts for close to half of general government spending, raising concern that expenditure cutbacks on the state and local levels could offset some of the stimulus provided by the federal government. This issue is addressed in Section VII, which reviews the principal causes of the state and local fiscal crisis and attempts to quantify its macroeconomic implications. Rising deficits have been caused both by shrinking corporate and personal income tax revenues and by sharp increases in cyclical and health-related spending—in part reflecting tax cuts and more generous benefit levels granted during the boom years of the 1990s. With budget reserves being increasingly eroded, further adjustment measures will be needed. However, the aggregate size of local and state government cutbacks is estimated to be only a small fraction of the overall stimulus provided by the federal government, and their macroeconomic impact is likely to remain small. Concluding RemarksMeaningful reforms of entitlement programs such as Social Security and Medicare tend to require long lead times, given their impact on intergenerational income distribution and politically controversial nature. To reach broad-based agreement on such reforms, fiscal resources are often required to smooth the transition and ensure that reform measures can be implemented over a politically acceptable time horizon. Only a few years ago, the conditions for movement on these fronts seemed to be in place in the United States, with the demographic shock still half a generation away and government debt set to be all but eliminated within a decade. Since then, however, a combination of cyclical, geopolitical, and policy factors have erased a decade's worth of fiscal consolidation, just a short time before the retirement of the baby boom generation begins. The discussion in this and subsequent sections suggests that the U.S. fiscal problem is still manageable, and there remains a window of opportunity for reform. However, the experience of recent decades has shown that fiscal consolidation is difficult to achieve and perhaps even more difficult to hold on to. Therefore, the room for maneuver is narrowing quickly. ReferencesAngrist, J., 1991, "Grouped-Data Estimation and Testing in Simple Labor-Supply Models," Journal of Econometrics, Vol. 47, No. 2/3, pp. 243–66. Blundell, R., A. Duncan, and C. Meghir, 1998, "Estimating Labor Supply Responses Using Tax Reforms," Econometrica, Vol. 66, No. 4, pp. 827–62. Congressional Budget Office (CBO), 2003, The Budget and Economic Outlook: Fiscal Years 2004–2013 (Washington: U.S. Government Printing Office). Council of Economic Advisers (CEA), 2003, Economic Report of the President, February 2003 (Washington: U.S. Government Printing Office). Gale, W.G., and P.R. Orszag, 2003, "The Administration's Proposal to Cut Dividend and Capital Gains Taxes," Tax Notes (Washington: Urban Institute, Brookings Institution), January. Available via Internet: www.taxpolicycenter.org/commentary/taxnotes.cfm. Gross, D.B., and N.S. Souleles, 2001, "Do Liquidity Constraints and Interest Rates Matter for Consumer Behavior? Evidence from Credit Card Data," NBER Working Paper No. 8314 (Cambridge, Massachusetts: National Bureau of Economic Research). Gruber, J., and E. Saez, 2000, "The Elasticity of Taxable Income: Evidence and Implications," NBER Working Paper No. 7512 (Cambridge, Massachusetts: National Bureau of Economic Research). International Monetary Fund, 2003a, United States: Report on the Observance of Standards and Codes—Fiscal Transparency Module, IMF Staff Country Report No. 03/243 (Washington: International Monetary Fund). ———, 2003b, World Economic Outlook, September 2003: Public Debt in Emerging Markets (Washington: International Monetary Fund). Leidy, M., 1998, "A Postmortem on the Achievement of Federal Fiscal Balance," in United States: Selected Issues, IMF Staff Country Report No. 98/105 (Washington: International Monetary Fund). Office of Management and Budget (OMB), 2003a, Budget of the U.S. Government, Fiscal Year 2004 (Washington: U.S. Government Printing Office). ——— , 2003b, Mid-Session Review, Budget of the U.S. Government, FY2004 (Washington: U.S. Government Printing Office), July. 1The U.S. fiscal year runs from October through September. 2The calculation of cyclical factors has been complicated by the sharp increase in capital gains tax revenues during the stock market boom of the 1990s. The CBO does not treat these revenues as a cyclical factor, but they clearly need to be excluded for identifying policy-related factors. Hence, Figure 1.2 includes a cyclically adjusted balance that has been corrected for the deviation of capital gains tax revenues from their historical average. 3Some studies have suggested a lesser contribution from cyclical factors, partly reflecting difficulties in distinguishing cyclical effects from structural shifts in the economy. For example, Leidy (1998) found that only about 20–25 percent of the fiscal improvement between FY1992 and FY1997 was caused by the cycle. He estimated that roughly half the turnaround was accounted for by tax measures and another one-fourth by reductions in discretionary spending relative to GDP. 4Both the Office of Management and Budget and the CBO regularly present a decomposition of changes in the budget balance into cyclical and other factors. 5Discretionary spending is controlled by annual appropriations acts. Mandatory spending is provided by permanent law and does not require annual appropriations to ensure the continuation of spending. 6See, for example, the discussion in OMB (2003a). 7At the same time, the short-term demand effect of the tax cuts is likely to have been limited by the fact that higher-income households tend to derive most of the income gains from tax reform (Gruber and Saez, 2000) but generally have a lower marginal propensity to consume than lower-income households (e.g., Gross and Souleles, 2001). 8For example, the administration's $87 billion supplemental to cover the costs of ongoing military operations and reconstruction in Afghanistan and Iraq was about twice the size expected at the time the staff projections underlying Figure 1.5 were made. 9The AMT is a parallel income tax system with fewer exemptions, deductions, and rates than the regular income tax (e.g., personal exemptions and the standard deduction are not allowed under the AMT). It was enacted to limit the extent to which high-income taxpayers can reduce their tax liability by using preferences in the regular tax code. Due to increases in nominal income, the number of tax returns subject to the AMT is projected to increase from 4 million in 2004 to 33 million in 2010. 10In a March 2003 speech, delivered at a Bank of France symposium, Federal Reserve Chairman Alan Greenspan remarked on the U.S. current account deficit: "There are limits to the accumulation of net claims against an economy that persistent current account deficits imply. The cost of servicing such claims adds to the current account deficit and, under certain circumstances, can be destabilizing." 11Cost increases for Medicaid are less strongly driven by demographic developments, since benefits are provided to all low-income households independent of age. 12OMB, 2003a, Chapter 3. This estimate assumes that current assets of the Social Security Trust Fund will be used to cover future pension benefits. 13Federal Reserve Chairman Greenspan also made this point in his February 2002 speech to the National Summit on Retirement Savings. 14The Social Security surplus reflects an accumulation of assets that is—in principle—matched by future obligations to retirees. For this reason, U.S. policymakers and other analysts have often focused on measures of the fiscal balance that exclude the Social Security surplus. |