View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

The case for modernizing the multilateral framework This is a defining moment for the global financial system and, by implication, for relationships between countries. The institutional and policymaking landscape is changing in a rapid and unpredictable manner. The changes are not being driven by a master plan but by a series of separate reactions to the global financial crisis. As a result, market accidents and policy mistakes have become largely inevitable. In the process, the inadequacy of today's multilateral coordination is there for everyone to see. Looking ahead, there is a need for introspection in the countries worst affected by the crisis and for a vision on how to move forward. The financial system will not reset to what it looked like just a year ago, and the longer-term impact of the crisis on the real economy—including on productivity and employment trends—will change the fundamentals of the world economy. All this accentuates the need for urgent and bold modernization of the multilateral framework.

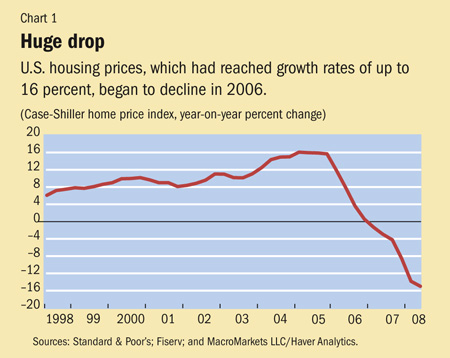

A crisis in the making The housing sector. The first major segment to experience a downturn was housing, starting in 2006 (see Chart 1). The immediate damage was felt in the most highly leveraged sector of the economy, a sector that also had the weakest capital support, least transparency, and poorest due diligence: subprime mortgages in the United States.

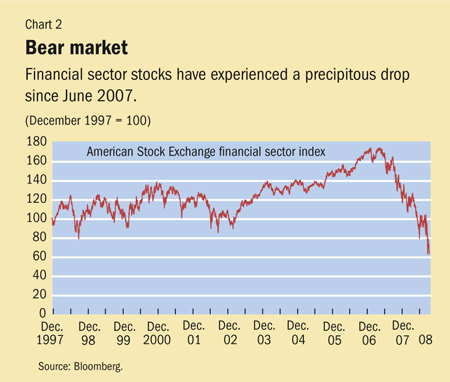

Initially, the majority of policymakers and market participants felt that the damage could be isolated and contained. This partly reflected unfounded confidence in the host of modern risk management techniques that had been enabled by the proliferation of derivative and structured products. And it partly reflected inadequate information about the extent to which subprime exposure had infected a number of balance sheets. The financial sector. The financial sector was the second major segment to experience a downturn, starting in 2007 (see Chart 2). At first the process was orderly. Institutions sought, and largely succeeded in mobilizing, new capital to support their strained balance sheets. And as they raised capital, they recognized their losses and looked to move forward.

But with the housing downturn accelerating and its impact spreading, banks had to run faster just to stay in place. The resulting repeated dilution of shareholders became apparent to all, and was quite costly. As a result, most providers of capital ended up saying "no more" and retreated to the sidelines. In such circumstances, and notwithstanding attempts to curtail credit elsewhere, banks were left with two strategic options: sell assets and/or dispose of businesses. But what made sense for an individual institution overwhelmed the system as a whole. In a classic example of a vicious "fallacy of composition," the system could not even come close to accommodating everyone's desire to sell without fueling further asset price deflation. This, in turn, accentuated the initial problems. Consumer demand in the United States. These negative developments were amplified by the third segment that started to weaken in 2008: consumers in the United States. After a prolonged period during which consumers spent well in excess of their income, they started to succumb to the combined pressures of higher prices, employment losses, and reduced availability of credit. With housing values declining, mortgage refinancing no longer provided an easy way to monetize residual equity in homes. As a result, consumers could no longer use their homes as cash machines. Weakening consumer demand also served as an important reminder of a largely hidden but equally disruptive feature of the crisis: the operation of negative feedback loops. Weakening consumer demand has further depressed the demand for housing. The robustness of car loans and credit card receivables has also been undermined, increasing the pressure on the balance sheets of financial institutions. And as banks have retreated further from the business of lending, the pressure on consumers has intensified.

The circuit breakers

But the accelerating and generalized nature of deleveraging has blunted these stabilizing forces. SWFs have retreated to the sidelines, waiting for markets to settle down and abiding by the time-tested wisdom of disrupted markets: "There are times when you worry about the return on your capital, and there are times when you worry about the return of your capital."

The decoupling angle

The most recent evidence shows that growth in emerging economies has started to moderate—partly in response to lower U.S. demand for their exports, and partly in response to the 2008 second-quarter tightening in monetary policy, designed to offset higher inflation pressures. This slowing has served to crystallize what, to date, has been an oversimplification of the debate about the evolving relationship between emerging and industrial economies. The debate should be framed not in terms of decoupling versus recoupling, but whether the decoupling is "strong" or "weak." The weak variant calls for growth in emerging economies to slow less than it has historically, given developments in industrial countries. In the process, emerging economies would benefit from offsetting factors such as pent-up local consumer demand, high domestic savings, large international reserves, and considerable room for maneuvering when it comes to countercyclical macroeconomic policies.

Yet even if the weak variant of the decoupling hypothesis proves true, it is unlikely to counter the adverse impact of deleveraging on global growth, poverty reduction, and welfare in any meaningful way. That explains recent bold policy actions around the world aimed at While these policy actions went into effect, the deleveraging dynamics fundamentally redefined the U.S. financial landscape. Just think: in 2008, the differences between commercial and investment banks have been eliminated; some icons of investment banking, such as Bear Stearns and Lehman Brothers, no longer exist; Merrill Lynch is now part of Bank of America; two high-profile banks, Wachovia and Washington Mutual, were absorbed by healthier institutions; and the world's largest insurance company, AIG, received an emergency capital injection from the Federal Reserve.

The IMF: initially missing in action No doubt many conclusions will be drawn—some valid, and others less so. I believe the one that will resonate most is that global financial activities ended up far outpacing the system's ability to accommodate those activities in an orderly manner. Simply put, the system's infrastructure—at both the national and global levels—failed us. At the global level, the debate will undoubtedly focus on the IMF's lack of active involvement—until now, at least, when it is supporting vulnerable emerging economies. After all, the deleveraging was nothing short of a systemic crisis that struck at the heart of the global financial system. It affected "global public goods" that are critical to the well-being of a large number of countries (such as the reserve currency status of the dollar, the predictability of the most liquid government market in the world, and the smooth functioning of the payments and settlement system used by most countries). Ironically, there was no lack of analysis at the IMF. The institution identified early the shared national responsibility for correcting the growing global imbalances. Moreover, there was general buy-in to the policy responses advocated by the IMF and others. And while the IMF was retooling and enhancing its financial sector analyses, its work identified some of the key policy issues. But the IMF's views and advice were largely ignored, and it did not fulfill the role of "knowledgeable trusted advisor." Meanwhile, the global system reached the point of debt exhaustion before embarking on the messy deleveraging process we find ourselves in now. By initially eschewing the superior policy solution—coming up with a coordinated multilateral response—the global system has incurred significant costs. These include forgone income growth, financial instability, and unemployment. And let us not forget that the most vulnerable segments of our society are most at risk.

Prisoners' dilemma Lacking sufficient legitimacy and representation, the multilateral framework was too weak to provide the necessary assurances that an individual country's preventive policies would be accompanied by supportive action on the part of others. As a result, no country moved decisively and in a timely manner to fix the imbalances. This lesson should be held front and center as the global system embarks on what is likely to be a prolonged period of rehabilitation and reform. An interconnected world requires more than timely national policies if it is to achieve high growth, poverty reduction, and financial stability. It needs national policies that pay greater attention to a range of cross-border effects. None of this will happen without a bold modernization of the system of international policy coordination. If we do not update our global financial architecture now, we are destined to repeat the mistakes of the past.

|