View this Issue Archive of F&D Issues Subscribe to Print Edition Write to us F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to: fanddletters@imf.org. F&D Magazine Free Email Notification Receive emails when we post new

items of interest to you. |

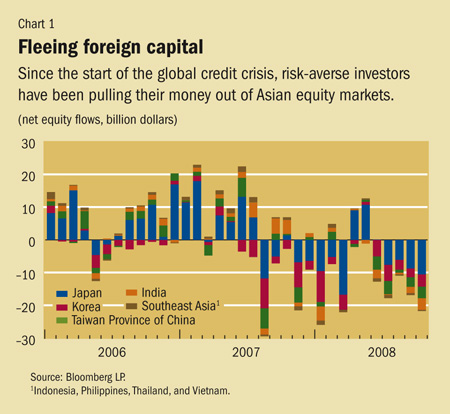

As the global financial crisis spreads, how will Asia weather the storm? Compared with other regions, Asia appeared at first better positioned to weather the storm created by the global fiancial crisis, thanks to its substantial official reserves cushion, improved policy frameworks, and generally robust corporate balance sheets and banking sectors. However, after the collapse of Lehman Brothers in mid-September and the ensuing rise in global risk aversion, the crisis spread to Asia and rattled many of its markets. Any hope that the region would escape the crisis unscathed has by now evaporated. With global growth expected to slow markedly next year and deleveraging to continue, Asia will likely face a difficult period ahead. How Asia withstands the shock of both slower global growth and a spreading financial crisis is critical not only for the region, but for the world as a whole. Asia's financial systems But given the region's large trade and financial integration with the rest of the world, investors' views of Asia soured as the global turmoil intensified and perceptions grew that the global economy was in for a major slowdown. Large net equity outflows have driven down stock prices sharply (see Chart 1). Asia-focused hedge funds have been among the worst performers worldwide, with their returns consistently below those of other emerging market funds.

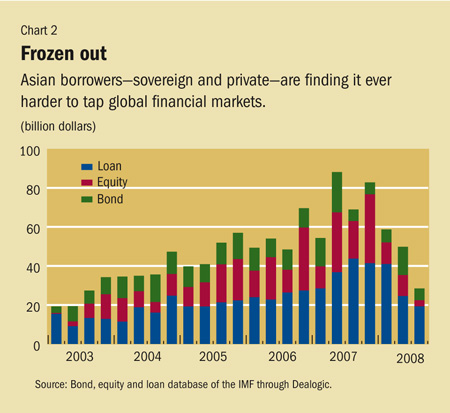

Capital outflows have also significantly weakened currencies in some countries, notably India, Korea, New Zealand, and Vietnam. And several countries have responded by intervening to support their currencies, in stark contrast to the past several years, when most Asian countries were concerned about the rapid appreciation of their currencies. With the rise in global risk aversion, Asian governments, corporations, and financial institutions have found it more difficult to access the global financial markets (see Chart 2). Countries with banking systems that rely more on wholesale financing and less on retail deposits (Australia, India, Korea, New Zealand) have experienced a higher rise in borrowing costs, partly because of concerns they will face difficulties rolling over their debts. As a result of these tightened conditions, the region's private external financing has fallen sharply.

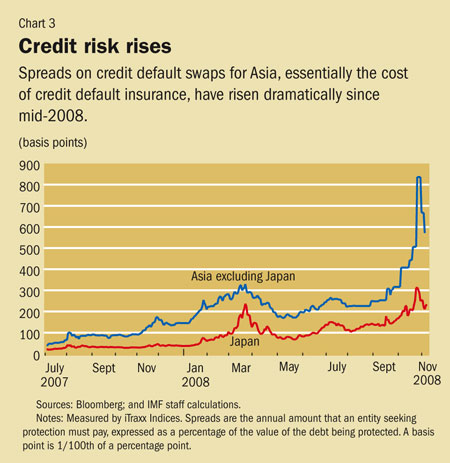

Domestic interbank and money markets have also come under stress from the global turmoil. In financial centers (Hong Kong SAR, Singapore, and Tokyo), interbank spreads over comparable government yields (so-called TED spreads) have risen, reflecting concerns about counterparty risk with foreign banks as well as a flight to quality. Spreads on credit default swaps for Asia—the cost of insurance against default on corporate bonds—have widened substantially (see Chart 3). The cash market for domestic structured products also remains effectively shut down as investors continue to turn away from securitized instruments. Most worrisome for a region highly dependent on external trade is the mounting evidence that trade financing is drying up. Finally, the global shortage of dollar liquidity is spilling over to affect local currency markets, such as those for swaps and repurchase agreements, leading to some market dysfunction and higher domestic funding rates.

A range of policy responses What the region faces Preparing for the worst • Managing exposure to large leveraged institutions. The failures of several large distressed institutions in the advanced economies have raised concerns about potential exposure to other highly leveraged players, including those in Asia. Early disclosure of exposure can help ease market concerns and allow investors to differentiate across institutions and countries. (For example, the Japanese Financial Services Agency publishes holdings of subprime and other structured products by deposit-taking institutions.) Further defaults can be expected, and policymakers should review contingency plans, including addressing possible fallout on the interbank market and ensuring the adequacy of deposit insurance (or guarantees) and public recapitalization programs. In addition, greater cross-border collaboration among supervisors would help strengthen monitoring of financial distress from overseas and, where financial systems are interconnected, lay the groundwork for more effective coordinated actions. • Enhancing liquidity risk management. Supervisors must ensure that banks follow proper regulatory standards for liquidity risk management—for example, through avoiding maturity mismatches. They also must ensure that banks perform stress testing and contingency planning that incorporate extreme events such as cutoffs of foreign financing. Central banks should also consider reviewing the range of available liquidity instruments, including in foreign currency, and the possibility of extending liquidity provision to a broader set of institutions and against a wider range of collateral. • Safeguarding access to cross-border funding, including trade financing. Domestic banks depend heavily on foreign bank subsidiaries for U.S. dollar liquidity, as well as on foreign exchange swap markets, which have come under stress during periods of high risk aversion and, in turn, affected other local funding markets. To ensure smooth cross-border funding, regulators should examine counterparty risks in these markets and ensure that local banks have alternatives to foreign funding if they are temporarily cut off from these markets. Extending guarantees to cover trade finance in the event of a cutoff should also be considered. • Strengthening risk management. With slowing growth, corporate default rates and nonperforming loans can be expected to rise. Regional banks with exposure to sectors that are especially vulnerable to a domestic slowdown, such as housing and small and medium-sized enterprises, may be at greater risk. Supervisors will need to ensure that local banks properly classify loans and set aside adequate provisions for problem loans. • Standing ready to recapitalize banking systems, if needed. At this stage, the possibility of a larger than expected wave of corporate defaults leading to bank failures cannot be ruled out. Authorities should thus consider contingency plans, if public funds are required to prop up the capital base of financial institutions. • Implementing longer-term financial reforms. Although the crisis is still unfolding and lessons are still being learned, policymakers may take this opportunity to implement longer-term reforms to strengthen their financial systems. These might include strengthening risk-based supervision, addressing the procyclical risks from leverage, further developing local bond markets, and enhancing the monitoring of systemically important institutions, including those outside the banking system.

|