| Guyana and the IMF | |

|

|

March 19, 2003 Ordering Information

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Introduction and Background1 Philippe Egoumé-Bossogo |

|||

|

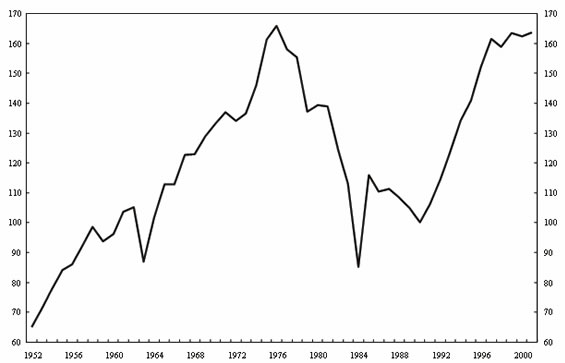

Stabilization and structural adjustment experiences in many transition and developing countries have been widely documented. Guyana represents the unique perspective of a Caribbean developing country, which has moved from a state-controlled to a market-based economy with a measure of success.1 This paper analyzes this process and the challenges that Guyana faces in the period ahead. Guyana is a poor country with characteristics similar to many developing countries, namely per capita income below US$1,000, heavy reliance on a few raw materials for foreign exchange earnings, underdeveloped physical and institutional infrastructure, high external indebtedness, and weak social indicators. Guyana is also, in some respects, a transition economy. The country experienced state economic planning for almost two decades (1971–89), which led to a significant economic contraction and rise in poverty. As a result, the adjustments to a market economy during the 1990s were broader and deeper than in an ordinary developing country. Figure 1.1 illustrates the three distinct periods of the recent economic history in Guyana: (i) the decade before and after independence (in 1966); (ii) the period subsequent to the adoption of state planning in 1975; and (iii) the period after the launch of the Economic Recovery Program (ERP) in 1989. Guyana gained its independence from the United Kingdom in 1966. The post-independence government initially focuses on attracting foreign capital. Economic growth in the immediate post-independence period continued, strengthened in part by pro-market policies including the positive investment climate. However, beginning in February 1970 economic policy gradually was shifted toward state control and Guyana was declared a Cooperative Republic in 1975. The second national development plan (1972–76) reflected this fundamental shift away from market-oriented policies. During 1971–76, the government nationalized all major production and distribution enterprises, including the large bauxite and sugar industries in 1971 and 1973, respectively, increasing the size of the public sector to about two-thirds of the economy, and public employment rose to over 10 percent of the population. Despite sharp increases in sugar prices in 1975 and 1979, the years that followed were marked by economic decline, massive emigration of skilled workers, and a growing and pervasive role for the public sector.

During 1976–88, state control over the economy intensified and widened to all sectors of the economy, including the financial sector with the nationalization of foreign-owned banks. The government instituted foreign exchange rationing and price controls and imposed restrictions on external current and capital accounts transactions. The resulting resource misallocation coupled with poor policy implementation led to a sharp decline in real economic activity. During this period, cumulatively real GDP per capita declined by 31 percent, inflation accelerated eight-fold, government debt rose from 31 percent of GDP to 475 percent of GDP, and import coverage of reserve dwindled to less than a week. By 1984, real GDP had fallen to its lowest level since 1955. In 1985, a new government took office and initiated timid measures to reduce the role of the public sector and jump-start macroeconomic stabilization and economic reforms (for example, through consecutive devaluations over 1986–88). But the approach was not comprehensive enough to improve the economy. In 1989, faced with the failure of the planned economy reflected in large and rising external payments arrears, lack of access to international capital, and a debilitated economy, Guyana launched the Economic Recovery Program (ERP). The comprehensive ERP combined macroeconomic stabilization policies and far-reaching structural reforms to restore sustainable output and employment growth in the context of a market-based economy. With substantial support from international financial institutions and bilateral donors, the reform effort continued throughout the 1990s, shifting Guyana back from state planning to a market-oriented economy and restoring macroeconomic stability and economic growth (Table 1.1). This paper analyzes the policies implemented and results achieved during this period. During most of the 1990s, the combination of a sharp recovery in economic growth following the implementation of market-oriented policies and the strengthening of social programs resulted in poverty reduction. There also was a gradual improvement in the delivery of essential social services, especially education and health services. Most groups in the country appear to have benefited from the stabilization and adjustment programs in the 1990s (Chapter 2). Fiscal policy focused on reducing the prevailing large fiscal deficits, which had resulted in an unsustainable public sector debt. Structural reforms in the public sector (i) improved tax collection through streamlining the tax system and better tax administration; (ii) restrained expenditures; (iii) fostered the business environment through price liberalization, and regulatory and land reform; (iv) reduced the size and cost of the civil service and made it function more efficiently; and (v) privatized most public enterprises (Chapter 3). Exchange rate policy contributed to the successful adjustment process in Guyana initially through devaluations and beginning in 1991 through a flexible exchange rate regime. The weaker Guyana dollar helped make the economy more competitive, encouraged private investment, and provided incentives to export. Also, restrictions to current and capital account transactions were lifted (Chapter 4). Along with reduced fiscal deficits, tighter monetary policy led to a decline in inflation, buildup of gross international reserves, stabilization of the exchange rate after floating, and increased credit to the private sector. Monetary authorities were given greater autonomy to conduct monetary policy and regulate and supervise the financial system. They developed more and better instruments of monetary policy and enhanced prudential regulations and their supervisory capacity. Moreover, the privatization of several financial institutions and the entry of new private banks increased competition in and the efficiency of the banking sector. In the wake of the financial sector reforms during the 1990s, financial intermediation recovered as real money demand increased and interest rate spreads began to decline (Chapter 5). Guyana's external debt reached unsustainable levels in the 1980s (276 percent of GDP by 1989) and the country defaulted on its obligations. The transition began in 1987 when Guyana signaled its intention to regularize its debt obligations. Together with the ERP and normalization of relations with foreign creditors, the successive debt rescheduling agreements (on Venice, Toronto, London, Naples, and Lyons terms; (twice) under the Heavily Indebted Poor Countries Initiative, and with other official and private sector creditors) led to a significant reduction in the stock of outstanding public debt and debt service. Guyana was able to restore and strengthen its creditworthiness during the transition to a market-oriented economy (Chapter 6). The transition to a market-oriented economy was accompanied by trade reforms with an outward-oriented focus. Trade liberalization, which developed in the Caribbean regional context, increased trade and improved the efficiency and resource allocation, especially through facilitating access to imported inputs. Trade also fostered the diversification of the export base and encouraged domestic and foreign investment (Chapter 7). To better understand the economic performance, Chapter 8 analyzes the sources of economic growth and shows that the implementation of sound macroeconomic policies in Guyana has helped spur growth. As illustrated in Figure 1.1, during the transition period, real GDP grew steadily and by end-2000 it had recovered to around its peak in 1976 (though it has somewhat stagnated between 1998−2000). Chapter 9 outlines the next steps toward poverty reduction and the risks and challenges ahead. It draws largely from the authorities' draft poverty reduction strategy paper (PRSP). Bibliography Government of Guyana, 2000, "Interim Poverty Reduction Strategy Paper," (Georgetown). International Monetary Fund, 1996, "Guyana—Recent Economic Developments and Selected Issues," Staff Country Reports No. 96/123 (Washington). ———, 1998, "Guyana—Statistical Appendix," Staff Country Reports No. 98/13 (Washington). ———, 1999, "Guyana—Recent Economic Developments," Staff Country Reports No. 99/52 (Washington). 1Guyana is a small, English-speaking, Caribbean country sandwiched between Venezuela to the west, Suriname to the east, and Brazil to the south. It is a former British colony, which gained independence in 1966. Its population and population growth were estimated in 2000 at 772,000 and less than 1 percent a year, respectively. It is estimated that at least as many people of Guyanese extraction live abroad, mainly in North America, the United Kingdom, and in other English-speaking Caribbean countries. The population is composed mostly of people of East Indian and African origins. Mixed people, Amerindians, Chinese, and whites constitute small minorities. GDP per capita in 2000 was around US$800. The country's main export products (in declining order of importance based on 2000 export values) are sugar, gold, bauxite, rice, shrimp, and timber. |