Financial Market Turbulence and Global Imbalances

Remarks at Conference on European Economic IntegrationAustrian National Bank

John Lipsky, First Deputy Managing Director

International Monetary Fund

November 19, 2007

It is a pleasure to be here in Vienna. I'd like to thank the Austrian National Bank for giving me the opportunity to speak today about the dual goal of sustaining global growth while reducing global imbalances. Achieving these dual outcomes is a central challenge for the IMF, and for its 185 member countries [Slide 1].

{kind=link}

The existence of record international payments imbalances has been seen by many in recent years as a risk to both global growth and stability. The unexpected post-2001 resilience of the global expansion—and it's largely unanticipated ubiquity—has created unprecedented optimism about the prospects for prospective advances in many aspects, including poverty reduction. If strong growth could be sustained, it would help provide the resources for key social goals such as environmental protection, improved medical care, and coping with the profound demographic changes that are fast approaching. Thus, the importance of sustaining global growth has become even more clear than in the past. And the prospects of success seem more plausible than at any time in recent decades, following such hopeful developments as the recent gains in real per-capita income in Sub-Saharan Africa.

Nonetheless, the emergence of record international payments imbalances—even in the context of strong and globally balanced GDP growth—has underscored a key vulnerability of the expansion. These imbalances have reflected—among other things—significant differences in the pace of domestic demand growth between many key economies. The phenomenon often referred to as the "global saving glut" in fact has been accompanied by weak investment and sluggish consumption gains in many key economies. It has long been recognized that attaining better balance in the strength of domestic demand gains will be needed if the strong global expansion is to be extended in the coming years. In fact, the persistence of large payments imbalances has been seen widely as a sign of the vulnerability of the past few years' exceptionally favorable performance.

Thus, it is not surprising that the financial market turbulence of the past months has heightened the unease regarding the near-term outlook. In this context, it is important that policymakers continue to take the steps necessary to underpin the orderly and effective functioning of global financial markets. Moreover, it is necessary to bolster confidence that global markets will continue to offer the unprecedented opportunities for progress that have been seized in recent years by emerging and developing economies. For example, success in the Doha round of trade negotiations would provide a powerful and positive signal around the world.

Overview

My talk today revolves around three key considerations:

• First, global risks attached to imbalances are being re-evaluated in light of recent financial turmoil and oil price gyrations. A key consideration is whether recent developments, including exchange rate shifts, have been supportive of attaining our dual goals. The IMF's conclusion is that while the latest developments have increased risks, the most likely outcome remains a favorable one—if the appropriate policies are implemented, especially in key economies.

• Second, the appropriate strategy remains the implementation of a credible set of policy measures that will be maintained over the medium term, not an attempt at a short-term fix. Imbalances will decline gradually—but significantly—if the appropriate policies are adopted. Failure to do so will risk more abrupt—and potentially disruptive—adjustment that could threaten the expansion.

• And finally, an appropriate set of strategies are precisely those embodied in the policy roadmap proposed in the context of the IMF's Multilateral Consultations on Global Imbalances. It is now vital that this agenda be implemented fully, and that the recent market turbulence isn't allowed to distort or delay the needed policy adjustments [Slide 2].

{kind=link}

Global Risks

Let me begin by discussing risks posed by recent developments. First of all, it is likely that the combination of financial market turbulence and the new rise in oil prices—if sustained—will tend to dampen growth and heighten the downside risks to growth in the coming year or so [Slide 3].

{kind=link}

While it is still too soon to draw firm conclusions, here is a rough estimation of what the growth outlook might look like if the latest rise in energy prices is sustained more or less in line with current futures prices [Slide 4].

{kind=link}

The principal point here is straightforward. It has been widely asserted that one of the important aspects of the current environment is that global growth has decoupled from that of the United States, and to an important degree, the expansion of the key emerging economies has become independent of that of the industrial economies. However, the latest challenges have been rather broader in nature, affecting virtually all economies [Slide 5].

{kind=link}

A new challenge to global growth is the latest rise in oil prices.

• As we all know, oil prices in recent weeks have touched new all-time highs in dollar terms-despite only minor supply disruptions. Oil demand remains robust-particularly from emerging markets, where in many cases earlier price increases have not been passed through fully or uniformly to consumers. Heightened supply concerns also appear to have played a role in the latest increases. The cumulative evidence of tight supply conditions, a falling dollar, and rising geopolitical tensions have played key roles in the recent run-up.

• Spare production capacity remains appreciably below its historical `comfort zone' And this situation is not likely to improve anytime soon. With oil market conditions so tight, the recent prices rises could persist and any significant supply disruption likely would push prices dramatically higher [Slide 6].

{kind=link}

Higher oil prices have important distributional consequences, including for global trade balances.

• Oil importers-especially, low-income countries-are likely to be hard hit; the impact of the recent oil price surge on trade imbalances could be 2-3 percent of GDP or more in many countries in Sub-Saharan Africa, and, to a lesser extent, in the Caribbean and Central America.

• For some importers, however, the impact of higher oil prices has been cushioned by dollar depreciation, other commodity price gains, or limited pass-through to domestic energy prices facing consumers [Slide 7].

{kind=link}

Other factors—such as the weakness in housing markets—could have a broader impact than is often recognized. For example, housing markets in several European countries have weakened, as well as in the United States [Slide 8].

{kind=link}

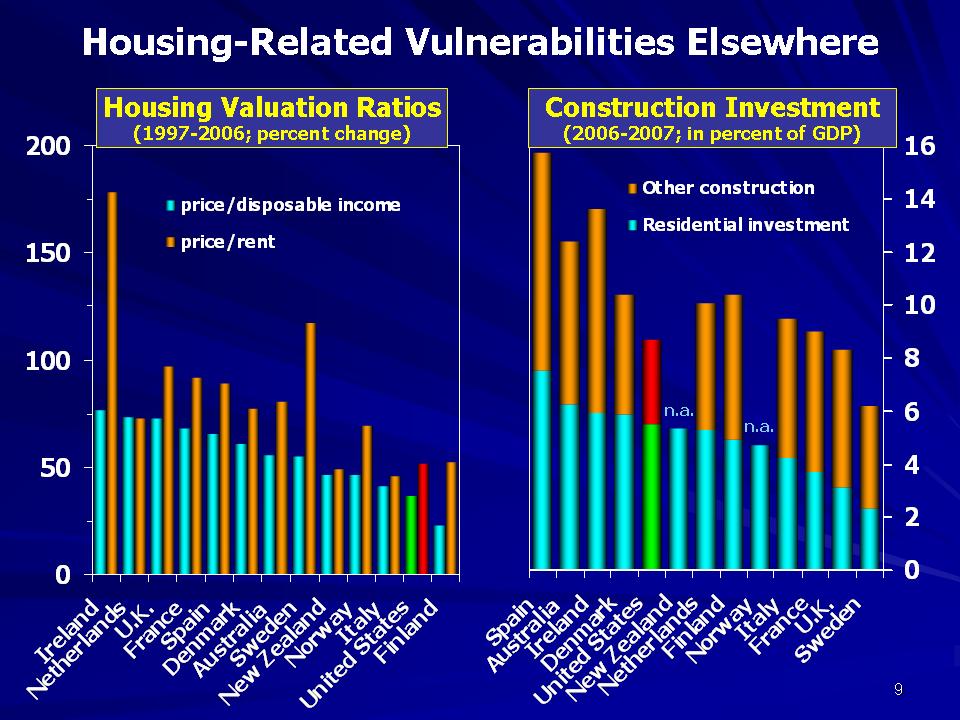

Moreover, while it is not always acknowledged, housing valuations and the relative importance of construction activity in the United States are not unusual when seen in a global context [Slide 9].

{kind=link}

At the same time, financial market strains are visible in many markets. And the second-round impact of the continued difficulties in interbank funding markets—exacerbated by doubts about the reliability of valuations on balance sheets—and even by potential worries about the size of excess capital cushions in some financial institutions—does not look like it is going to dissipate quickly [Slide 10].

{kind=link}

The impact on credit conditions of recent market strains shows that the risks posed to the expansion by potential pro-cyclical tightening of credit is widely shared, at least in European markets [Slide 11].

{kind=link}

In sum, the combination of higher oil prices and financial market strains could slow—at least to some degree—the narrowing of global current account imbalances.

• Past declines in the dollar have contributed to the U.S. current account deficit moderating faster than expected. However, the oil trade imbalance is now likely to deteriorate further because of higher oil prices, offsetting some of the reduction in the current account deficit attributable to the dollar depreciation.

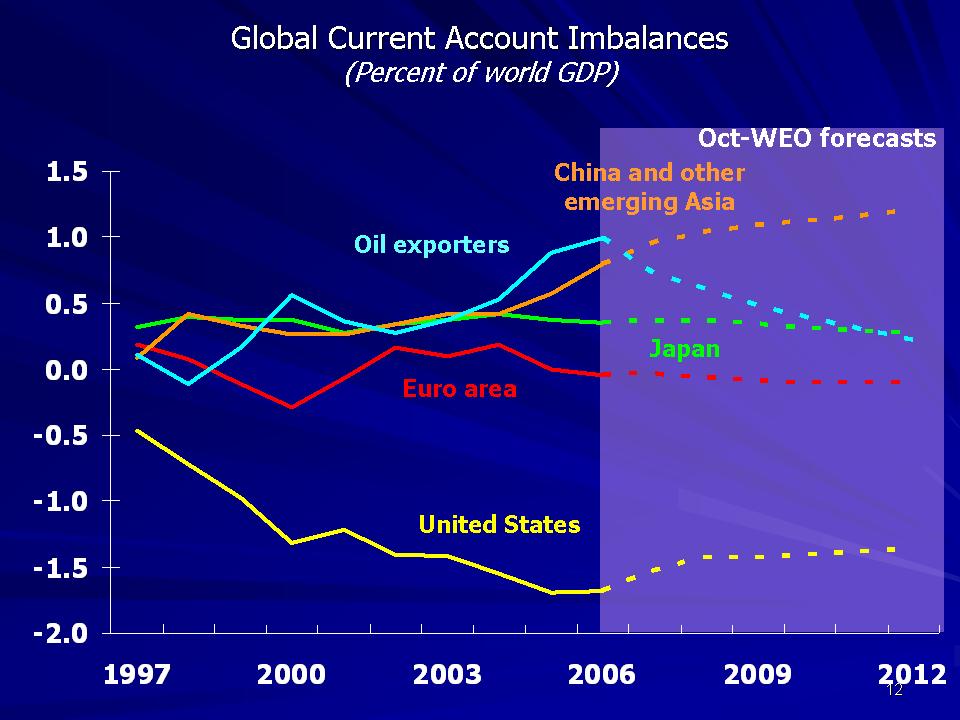

• The expected reduction in oil exporters' surpluses may be less rapid than previously projected-shown here based on the October 2007 WEO (where the oil price baseline was about 20 percent lower than it is today) [Slide 12]

{kind=link}

.

Recent financial turmoil-particularly the impact on the market for asset-backed securities-raises new questions and requires some rethinking about the financial flows providing the counterpart of global current account imbalances [Slide 13].

{kind=link}

Up to now, the U.S. current account deficit has been easily financed, but this should not be taken for granted. Financial flows to the United States reflected, in part, the packaging of marketable financial claims in the world's deepest, most liquid, and sophisticated financial markets. But doubts have risen about pricing and liquidity in certain key financial markets, and this has already contributed to the recent weakening trend of the US dollar.

• Financial turmoil has left a noticeable imprint on U.S. net portfolio inflows, which have been unusually weak since July. This includes reduced foreign purchases of U.S. asset-backed securities—which accounted for somewhere between one-quarter to one-third of recent net financial inflows. The slowdown in these inflows has reflected rising concerns about the quality of the underlying assets, questions about proper valuation and ratings, and illiquidity in some of these markets.

• A further weakening of the US dollar, could both reflect and contribute to a softening of demand for U.S. assets.

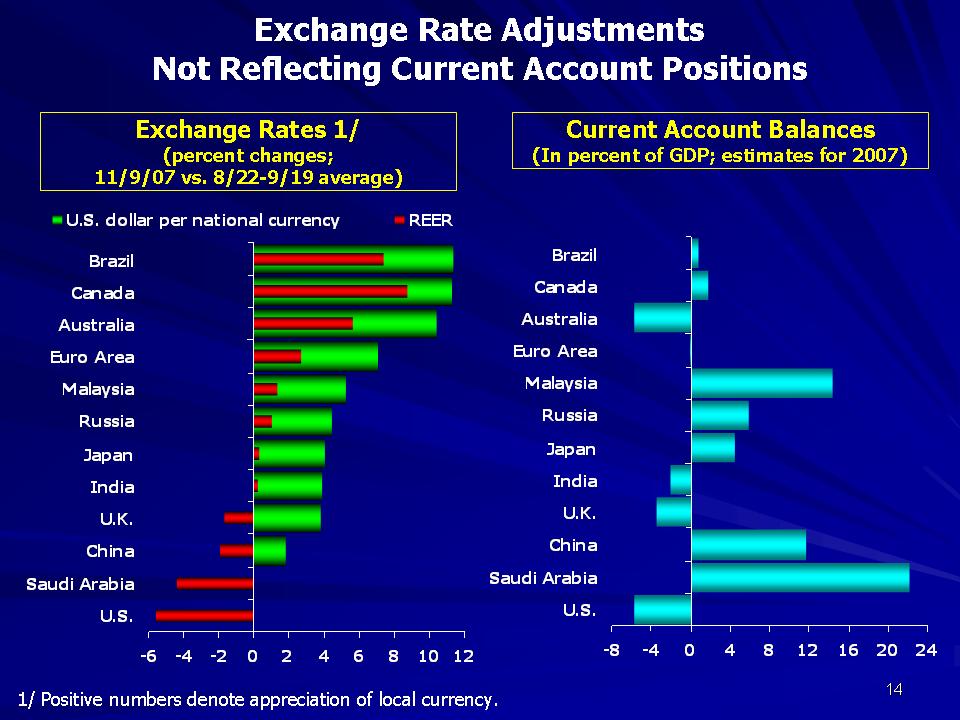

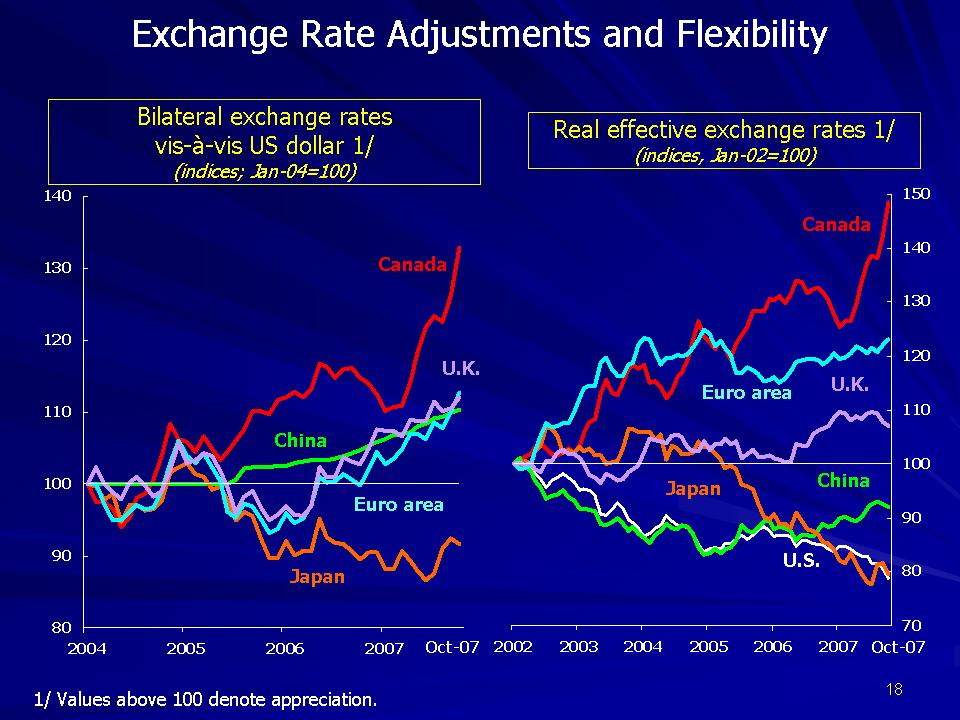

The recent pattern of adjustment in exchange rates has not corresponded to the pattern of current account deficits nor has it matched the shifts that were anticipated as likely by the participants in the Multilateral Consultations on Global Imbalances.

• The dollar's significant depreciation since the turmoil began- that has amounted to about 5 percent in effective terms—has been concentrated against some currencies, with little movement against other key monies. The composition of the shifts has had little direct correlation to the pattern of external imbalances. As a result, the adjustment burdens appear to be falling disproportionately on countries with more flexible exchange rate regimes.

• This could be a recipe for fueling tensions between trading partners that carries added risks, including the threat posed by rising protectionist pressures that could become aggravated if global growth were to slow.

• It is clear that a set of broad-based and better-balanced fundamental and financial adjustments are needed. The dollar's depreciation so far has moved in an appropriate direction and it has reduced the currency's medium-term misalignment based on the Fund's exchange rate analysis. However, some key surplus economies' currencies remain undervalued relative to medium-term fundamentals, while some more flexible currencies—including the euro—may have strengthened somewhat more than would appear warranted from a medium-term perspective [Slide 14].

{kind=link}

To summarize, we need to guard against assuming that global imbalances will take care of themselves smoothly, evenly, and in a growth-friendly manner. There is a risk that barring appropriate policy action, global rebalancing may be weakened or delayed or that the burden of adjustment would not be shared broadly. Moreover, in order to sustain global growth, domestic demand gains outside the United States will need to strengthen.

Appropriate Strategy

What is the appropriate policy strategy to mitigate these global risks? Discussions on how to address global imbalances have tended to follow two separate tracks. The first emphasizes that an imbalance between desired savings and realized investment around the world lies at the heart of the current account imbalances. The second emphasizes the role of exchange rates- particularly those that have remained relatively inflexible in a world of globalized trade and finance-as a key factor behind the evolution and the resolution of the imbalances .

But these two tracks are not mutually exclusive. There is a role for both a rebalancing of saving and investment through macroeconomic policies, as well as a role for exchange rates in safely reducing imbalances in a manner that does not induce unnecessary volatility in output. In fact, these two approaches are mutually reinforcing, as changes in real exchange rates help to achieve the necessary shift in resources between tradable and non-tradable sectors without major disruptions.

A potentially successful three-pronged strategy- in effect the strategy endorsed by the IMFC and embedded in the Multilateral Consultations- involves:

• Raising U.S. saving

• Raising productivity growth, investment, and boosting domestic demand growth in the rest of the world

• Allowing for greater exchange rate flexibility in certain surplus countries.

If progress towards these goals is made in a steady and sustained fashion, global imbalances are likely to be resolved in the desired manner-i.e., one that supports global growth while reducing risks [Slide 15].

{kind=link}

Let me turn to each of these key strategic components in turn, and identify where further progress is clearly needed. Beginning with industrial countries, the outlook for U.S. private and public saving has improved.

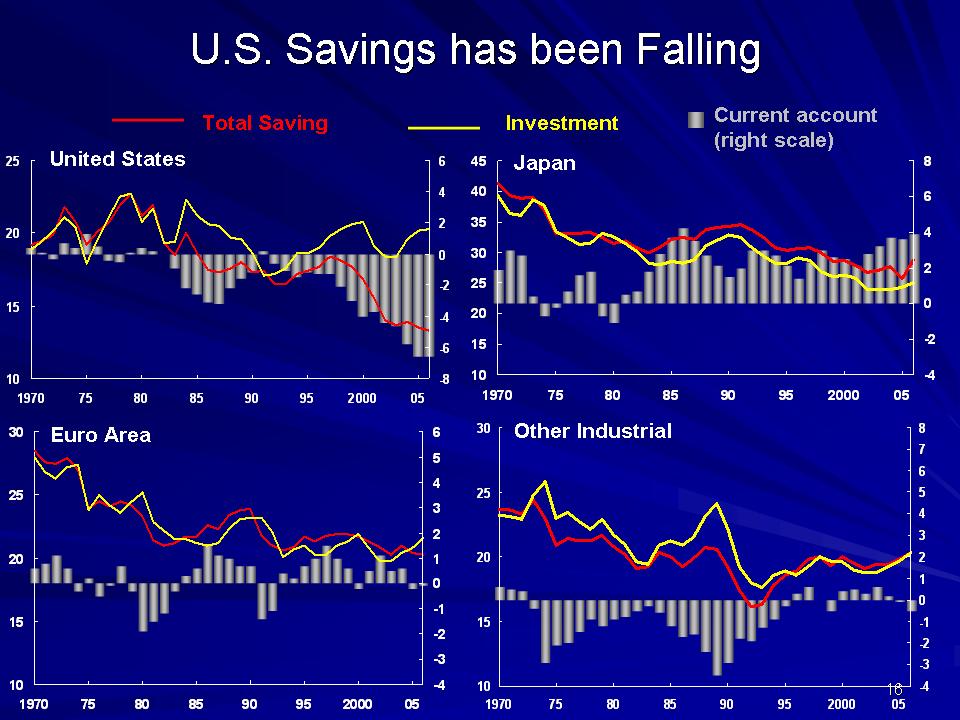

• After the significant fall in U.S. national saving that began around the mid- to late-1990s, and that played a leading role in the rising U.S. current account deficit after 2000, saving now appears to have stabilized. Given recent developments in U.S. housing and credit markets, the partly wealth-driven decline in household saving rates appears to have bottomed and is set to begin reversing. There are strong reasons to anticipate that US household saving out of current income is going to normalize in the coming years.

• The US. fiscal deficit has declined significantly—helped by buoyant revenues, although longer-run pressures on public finances remain a concern.

• Given recent exchange rate trends and the relative balance of risks to demand growth at home and abroad, the U.S. external deficit could be reduced more rapidly than projected. The latest trade data and the positive contribution of net exports to third-quarter growth are evidence in this direction.

In Japan, while the downward trend has eased, investment has yet to recover fully.

• Investment, which generally declined in advanced economies since the late 1990s and 2000, has broadly returned to prior levels only in 2006, except in Japan. Addressing past excesses, Japanese corporations have reduced debt over a protracted, decade-long deleveraging process, helped by surging profits, but investment still remains relatively low.

• The value of the yen and the level of domestic interest rates also remain low by historical standards-amid lingering concerns about the underlying vigor of domestic demand. In recent weeks, some unwinding of carry trades has led to yen appreciation.

• The underlying strength of productivity, given an aging work force, and competition in key sectors have remained key concerns for the economy.

In the euro area, saving-investment imbalances have been relatively modest, but economic growth and productivity performance have been lackluster. While growth has improved in the past year or so, structural concerns continue to weigh on longer term growth prospects [Slide 16].

{kind=link}

In emerging markets, saving remains high while investment generally remains sluggish.

• Saving rates have increased sharply this decade in most emerging market regions. In Latin America, the fiscal retrenchment undertaken in the late 1990s, combined with higher commodity revenues has resulted in higher public saving. Yet, investment-both in the public and private sectors-has been sluggish.

• Meanwhile, the sharp rise in oil prices and revenues is likely to push saving and current account surpluses higher for oil exporters. So far, oil producing economies have on average spent 30-40 percent of their extra oil revenues on increased imports, although there is substantial variation across countries.

• In East Asia, while high saving rates have moved essentially sideways, there was an almost uniform drop in investment across the region following the Asian crisis. More recently, there are signs of a gradual investment recovery, and if this were to persist, it would help to alleviate imbalances.

• China has seen strong investment, but saving has more than kept pace. Led by rising corporate saving, China's very high domestic saving rate-which reached 53 percent of GDP in 2006-continues to produce growing external surpluses despite rapid investment growth [Slide 17].

{kind=link}

There has been some progress on improving exchange rate flexibility, but more is needed.

• Renminbi flexibility against the dollar, for example, has modestly increased. Since the regime change in mid-2005, the currency has appreciated bilaterally against the dollar, and (surprising to some) to a similar degree as the euro over that period. But as noted previously, the degree of bilateral appreciation has been relatively muted recently since the turmoil in financial markets began. The renminbi has appreciated by less than 2 percent against the dollar and has, in fact, depreciated slightly in real effective terms since end-July 2007.

• Also, the renminbi's real appreciation (about 8 ½ percent between May 2006 and August 2007) has also come through faster domestic inflation, led by surging food prices, and the inability of monetary policy to durably rein in domestic liquidity growth [Slide 18].

{kind=link}

The role of the exchange rate and stronger growth in trading partners will be helpful for global rebalancing.

• Exchange rates have helped in the past with external adjustment. Across countries, IMF research finds that exchange rate depreciations can moderate output losses that occur during current account reversals.

• Adjustment of the U.S. external deficit in the late 1980s, for example, involved both a 40 percent depreciation of the U.S. dollar in real effective terms, and a decline in the U.S. growth differential with trading partners. This adjustment was primarily induced by stronger growth abroad, rather than lower growth in the United States. The large real exchange rate depreciation contributed to the surge in real export growth and helped stabilize economic activity.

• What about now? The 16 percent real effective depreciation of the U.S. dollar since mid-2002 is now starting to have an impact on the non-oil trade deficit as a ratio to GDP. Consistent with the finding of low pass-through of exchange rate movements to U.S. import prices and high pass-through to import prices abroad, the effect of the dollar depreciation came mainly through a strong acceleration in export volumes. The slower growth of the U.S. economy relative to that of its trading partners also seems to have started having an impact on import volumes in 2006. Of course, these movements tend to be obscured by rising oil prices.

• I would also like to point out a feature of today's world that differs significantly from times past. In 1985, 70 percent of the world's current account surpluses were accounted for by five countries. Today, that same share is accounted for by ten countries, with more diverse exchange rate regimes. This makes the necessary adjustment of exchange rates to bring down imbalances more complicated, both economically and politically. It might also take longer [Slide 19].

{kind=link}

Multilateral Consultations

The goal of the IMF's Multilateral Consultation on Global Imbalances has been to meet the dual objectives that I mentioned at the outset-that is, to help position the global economy on an adjustment path toward a more durable and credible pattern of domestic demand growth while maintaining robust global GDP growth [Slide 20].

{kind=link}

The Consultation was launched in mid 2006. The five participants-comprising the euro area, China, Japan, Saudi Arabia and the United States, together with Fund staff-presented a progress report to the April 2007 meeting of the International Monetary and Financial Committee (IMFC). The formal presentations to that meeting were released to the public and they are available on the Fund's website. This includes a joint explanatory note plus the participants' individual policy plans.

This represents a major accomplishment, in that all the participants agreed that bringing down imbalances is a shared responsibility, and that the policy plans submitted by each participant is in line with their own best interests. To achieve a narrowing of imbalances, the policy road map that was put forth intended to address the key prongs I discussed earlier to reduce saving-investment imbalances through broad-based adjustment, more flexibly, and in a manner supportive of global growth.

I will very briefly discuss key elements in each participants' plan, and comment on how the Fund staff foresees potential progress and challenges in achieving these plans. The euro area's plans revolve around sustaining domestic demand growth, which will make a contribution toward improving global performance.

• The integration and transformation of the euro area (and EU) financial markets will provide an key impetus for improving the efficiency of the area's product and service markets. The renewed Lisbon Agenda reforms are critical to achieving this goal, including through labor market reforms.

• Consistent with the plans submitted, some progress has already been achieved in the area of financial markets in improving the efficiency of clearing and settlements. Looking ahead, it is important that the resolve to carry on with structural reforms continue, despite clear political pressures that exist to turn back.

China's policy undertakings are structured around three cornerstones and have seen some progress.

• First, rebalancing growth relatively more towards consumption while slowing investment growth and improving investment efficiency. Second, deepening financial sector reform. And, third, increasing the flexibility of the RMB. A more effective, market-driven financial system would help to strengthen domestic demand growth, while improving investment efficiency and increasing the usefulness of monetary policy instruments for maintaining macroeconomic balance. Experience has shown that such a sectoral and systemic transition is more easily managed with a flexible exchange rate policy.

• The announcements of monetary policy measures, and the widening of the daily trading band for the RMB have been consistent with China's policy plans.

Saudi Arabia's public spending plans in the energy sector and on needed infrastructure and social projects remains on track.

• The scale of recent revenue increases relative to the size of their economies implies that oil exporters' adjustment will have to be gradual. After all, adjustment must be undertaken in line with absorption capacity.

• Saudi Arabia is taking a lead in increasing social outlays where returns are high, including on education, health, and social safety nets. In addition, Saudi Arabia is implementing ambitious investment plans, including in the hydrocarbon sector. The net effect of these efforts is already impressive.

In Japan, deeper structural reforms are needed to improve growth potential and safeguard living standards, and this would support global growth.

• The reform priorities are to increase labor market flexibility, promote competition through greater market opening, and deepen trade integration. New structural measures will hopefully catalyze and sustain the still-tentative expansion. As consumption spending and investment strengthen, the current account surplus should narrow as a percent of GDP. Over the longer term, the trend toward a narrowing surplus also will be supported by demographic factors.

• Recent progress in these areas has been promising, but the agenda is far from finished. Recently, we have seen concrete progress on the liberalization of FDI inflows, as well as in advances on job training and placement. However, the areas where progress with respect to its policy plans remains a challenge is in boosting productivity in the anemic non-tradables sector of its economy.

The linchpin of the U.S. policy statement to the Multilateral Consultation appropriately focuses on raising national saving-both through policy incentives to raise private sector saving, and through plans to eliminate the fiscal deficit (ex-social security) by 2012.

• There are positive signs of progress. As I said, the current account deficit is shrinking, and 2007 may well mark the first year in twelve, that net exports will make a positive contribution to growth.

• Fiscal balances have also strengthened, in line with the multilateral consultation plans, but there are longer-term pressures on public finances, on which there needs to be a stronger political consensus for a solution. The full elimination of the fiscal deficit by 2012 is till going to take some hard work.

Overall, while there has been some progress, much more is needed to achieve full implementation of these policy plans-and, in my view, doing so has become all the more important [Slide 21].

{kind=link}

Why is full implementation so instrumental? Will it make a difference? To examine the potential impact of the five participants' Multilateral Consultation policy plans, Fund staff conducted simulations (subject to the usual caveats) using our Global Macroeconomic Model (or GEM).

• Specifically, we compared the effects of the five policy plans against two alternative scenarios: One alternative was a benign "no policy adjustment scenario," where all the adjustment in the saving-investment balance is driven by gradual private sector action. For benchmarking purposes, we called this the baseline scenario. We also used a "disruptive adjustment scenario," involving a loss of appetite for U.S. assets and a sharp correction in exchange rates, leading to an output contraction. The "Multilateral Consultation policy adjustment scenario" including the participants' policy plans provided the most stable and enduring adjustment to the U.S. current account deficit.

• In terms of the pattern of adjustment in the other participants, this policy adjustment scenario produced a smoother current account normalization in emerging Asia (where the current account surpluses are highest) than the disruptive adjustment scenario, while producing an earlier normalization relative to the baseline scenario [Slide 22].

{kind=link}

Turning now to growth, the Multilateral Consultation policy adjustment scenario produces a more gentle slowing of U.S. growth, than would a disruptive adjustment, while bringing output back towards the baseline more rapidly. The counterpart to this pattern for Emerging Asia is also similar—the gentler slowing of US output growth also cushions the fall in growth, relative to the baseline [Slide 23].

{kind=link}

As I had mentioned earlier, the roles of Japan and the Euro area come out much more clearly in terms of their roles in re-balancing global growth, not so much from current account adjustments. This slide shows the changes in output, in the multilateral consultation policy adjustment scenario, relative to the other two scenarios. Without the policy commitments they have made, the task of preserving global growth while bringing down the imbalances would be considerably more onerous [Slide 24].

{kind=link}

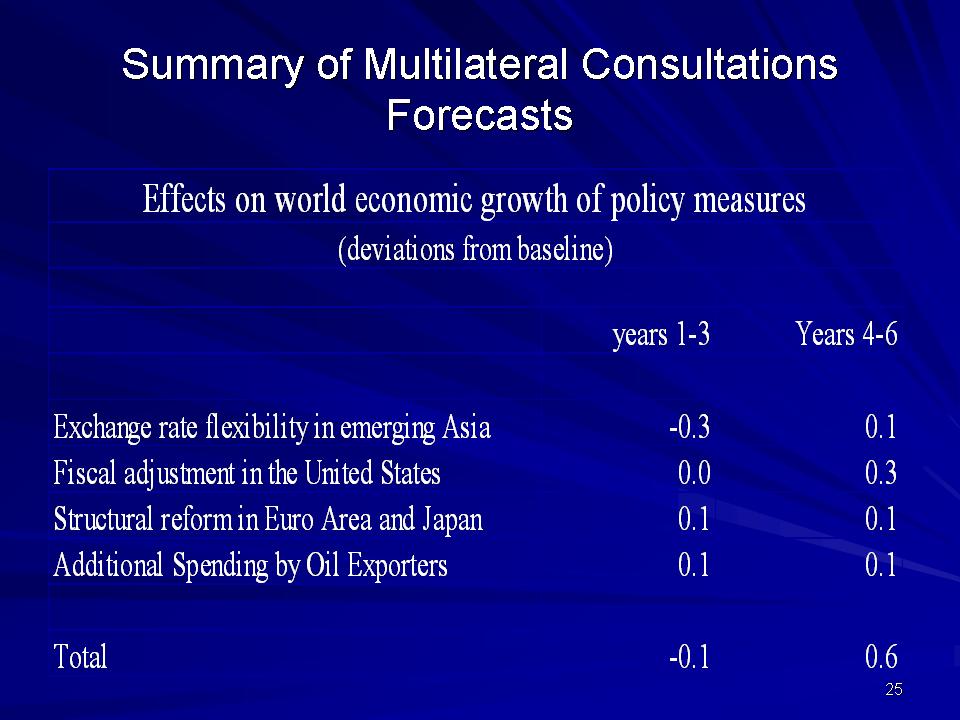

We also simulated all the spill-over effects of the policy adjustment scenario, and calculated the relative effects of this scenario on global growth over the next six years. Relative to the baseline, global growth would be virtually unchanged in the first three years. However, the following three years generate an increase in global growth rates of 0.6 percent per year .

Moreover, global growth would be better balanced over the medium term. From 2009 onwards, Japan, the Euro area, and emerging Asia would all grow 1.5- 2 percent more relative to the baseline, while US growth would be virtually unchanged from the baseline. The result would be a significant reduction in global payments imbalances [Slide 25].

{kind=link}

The Multilateral Consultations have created a potentially powerful tool for addressing the challenges posed by global imbalances, but the full implementation of these plans is key to achieving the dual goals of bringing down imbalances without sacrificing global growth. In a context of heightened uncertainty and market turmoil, follow-through has gained importance. The Multilateral Consultations were intended precisely to provide guideposts in an uncertain environment, and we hope that they will fully serve that function [Slide 26].

{kind=link}

Thank you.