Natural Resources and Development: Confronting Emerging Challenges in Botswana

Public Lecture at the Bank of Botswana by Mr. Naoyuki Shinohara, Deputy Managing Director

March 30, 2011As prepared for delivery

1. Good morning. Your Excellencies, ladies and gentlemen, I am delighted to be here with you today. I am also honored to share the stage with distinguished cabinet Ministers, and I wish to thank Governor Mohohlo for her kind introduction and for organizing this public lecture.

2. This is my first visit to Botswana and I am keen to learn more about the factors that underlie its impressive economic performance, which has been sustained over many years. In particular, Botswana is a model for resource-rich countries of how to manage resource wealth prudently. Sound macroeconomic policies, good governance, and a high rate of public investment have transformed Botswana from one of the poorest countries in the world at the time of its independence into an upper middle-income country today. This is indeed progress to be proud of. Moreover, although the fallout from the global financial crisis in 2008-09 hit Botswana hard, a rapid and appropriate policy response by the government have mitigated the effects of that shock on the broader economy. Going forward, Botswana’s prospects appear promising, provided there are no new global shocks, about which I will say more later.

3. My presentation today will focus on the central challenge facing Botswana: But before I do that, I will briefly describe the IMF’s latest outlook for the global economy and for sub-Saharan Africa in particular. Then I will discuss Botswana’s need to further harness its natural resources and comparative advantage to achieve sustainable and inclusive growth over the medium term. I will discuss three pillars: (i) reforms to foster private sector-led growth; (ii) measures to tackle high unemployment, income inequality and poverty; and finally, (iii) measures to further strengthen fiscal institutions to smooth shocks and minimize macroeconomic volatility.

4. In a nutshell, the good news is that we expect the global recovery to proceed, led by emerging markets, but the not so good news is that it will remain a multi-speed recovery with considerable downside risks. Although activity in advanced economies moderated less in the second half of 2010 than we expected, growth remains subdued and unemployment is still high. The intensification and broadening of financial sector strains resulting from sovereign and banking sector risks in the euro area is also contributing to downside risks. In addition, the current problems in the Middle East and North Africa region are contributing to rising oil prices, and if higher oil prices persist, it could also pose a risk to the global recovery. By contrast, in many emerging economies, activity remains buoyant. However, there are overheating and inflationary pressures in some, and these are exacerbated by large capital flows and rising commodity prices.

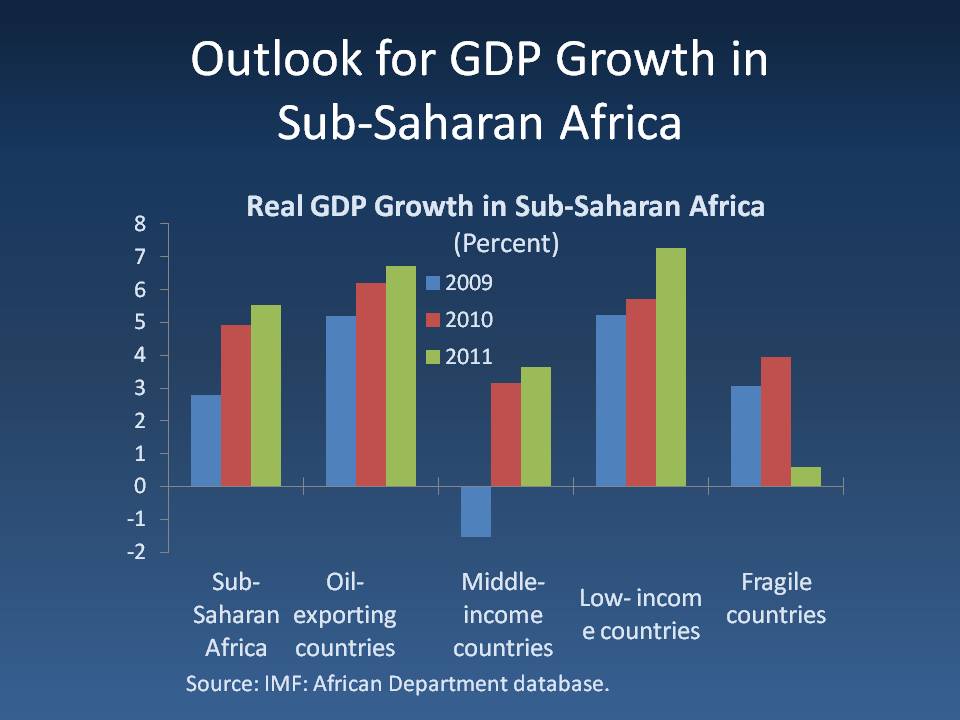

5. In this global economic environment, sub-Saharan Africa is experiencing a solid economic recovery.

• Following a sharp drop in the growth rate to 2½ percent in 2009, the region’s economy expanded by 5 percent in 2010 and is projected to grow by about 5½ percent this year. So after the brief hiatus, economic activity in most sub-Saharan African economies has now reverted fairly close to the heady levels of mid-2000s. Even by the high degree of heterogeneity that normally characterizes sub-Saharan Africa, the economic outlook for the region is particularly bi-polar: in most of the region’s low-income countries, output growth as of this year is set to be back to the average growth rates registered during 2000–08, but sizable output gaps are set to prevail in most of the region’s middle-income countries. For the oil and metal exporters, recent commodity price increases are expected to persist in the near term, but for net oil importers, oil prices at these elevated levels will generate significant external financing needs. However, overall, the aggregate picture is one of a strong recovery from the 2009 downturn.

• But this picture is not without blemishes. First, because of the economic slowdown in 2009, progress toward the poverty reduction target in the Millennium Development Goals has lost momentum due to falling incomes and increasing unemployment. Second, should global growth projections for 2011 not materialize, the prospects for sub-Saharan Africa would also be more circumspect.

• And, of course, there are risks to this positive outlook, including a sustained rise in food and fuel prices. Such rapid movements in key prices create big winners and losers in sub-Saharan Africa and complicate macroeconomic management. The food price increases, particularly if sustained, will disproportionately hurt the poor and can have long-lasting effects. However, elevated food prices can also offer opportunities for many sub-Saharan African countries to adopt policies to stimulate their agricultural sectors.

• In terms of policy response, the first best policy response in these circumstances is to allow the pass through of international prices to domestic prices, and to provide targeted support to the most vulnerable groups. This support can be in the form of subsidies, income support, or direct provision of food items. But of course, in many countries in the region identifying the neediest can be quite challenging, even more so when it has to be done at such short notice. Where such identification is not possible, other, still targeted relief should be considered. This could include temporary lowering of import taxes on essential staple foods. Monetary policy should accommodate first round effects and tighten if second round effects appear to be leading to generalized price pressures. Bearing in mind these risks, the challenge for countries in sub-Saharan Africa now is to rebuild policy buffers and sustain reform efforts and, more generally, to maintain the macroeconomic stability and growth momentum that seem to be taking hold more broadly in the region.

6. Let me now turn to the main theme of my presentation. An analysis of output developments in Botswana over the years show that trend growth has slowed in the last decade. A simple analysis of growth trends for Botswana show that the contribution of productivity growth to overall economic growth has been declining since the year 2000 with the deceleration in the growth of diamond extraction. Also notable is the decline in the contribution of labor to growth. These developments beg the question: how can Botswana transform the structure of its economy to sustain high growth and employment in the future? Indeed, one could argue that Botswana stands at a pivotal point in its history. A key challenge is to search for new engines of growth as the country’s long-term success on the back of natural resource exports seems to be fading.

7. During the last decades, Botswana has by and large pursued a growth strategy based on capital deepening which is centered on public spending. After years of high spending on public investment, Botswana’s infrastructure gap has narrowed considerably. Also, diminishing returns on public expenditure have already set in. Specifically, cross-country analysis show that despite high spending levels, outcomes (for example, educational attainment) are often poorer than in comparable middle-income countries. Thus, going forward, a combination of a leaner public sector (one that would do more with less) and a more dynamic private sector are essential for increasing and sustaining growth in Botswana.

8. The private sector cannot lead the way and unleash its productivity potential unless the public sector establishes an environment conducive to private sector activity. In this context, in addition to preserving macroeconomic stability, government policies need to support private sector activity through regulatory and other structural reforms that would ease the cost of doing business in the country. Recent findings in the October 2010 National Business Confederation report suggests that Botswana needs to do more to improve competitiveness, facilitate cross-border trade, and simplify and reduce the number of procedures required to start a business. In some specific circumstances, the public sector could also partner with the private sector through public-private partnerships. As I understand it, possibilities for such arrangements are being considered for the energy sector in Botswana. In this case and more generally, as international evidence suggests, it will be important that the appropriate legal and regulatory frameworks are in place to ensure that fiscal risks are mitigated and value for money is maximized.

9. In addition, further development of financial markets would be particularly important to ensure a better allocation of capital. This would also expand the benefits of financial intermediation to the large “un-banked” population, and thus contribute to the development of the non-mineral sector. Nonbank financial institution could play an important role in developing local financial markets. Meeting the needs of pension funds to hedge their offshore investments, for example, would offer opportunities to create futures and forward markets. In this respect, Botswana’s potential to develop into a regional financial center where regional governments and corporates may raise capital to finance growth depends upon establishing a benchmark yield curve.

10. Economic diversification will be a necessary anchor for greater private sector development. The search for new sectors could focus on exploiting Botswana’s existing capabilities that put it at a comparative advantage vis-à-vis its competitors given its track record of prudent management of public resources and a stable macroeconomic policy environment. Foreign direct investment, which is now confined to the diamond sector, may be attracted in such areas such as tourism, trade, and telecommunication if the costs of doing business are lowered. From a macroeconomic perspective, diamond exports are expected to plateau over the next decade or thereabout. Thus, current account deficits may become the norm unless efforts to substantially increase non-diamond exports take hold.

11. Ideally, diversification should cover activities whose output and price trends are uncorrelated with diamond prices. In this respect, the government’s focus on the supply of information technology services as well the creation of a regional financial center where regional governments and corporates may raise capital to finance growth could be well placed. On the demand side, Botswana needs to focus on new drivers for export growth. Global economic rebalancing and greater reliance of Asian economies as well as the BRICS (Brazil, Russia, India, and China) on their domestic sources of growth could offer Botswana opportunities to export more traditional products such as zinc, nickel as well as meat and non-traditional exports such as tourism. The ties between the BRICs and countries in sub-Saharan Africa have increased rapidly over the past decade. Thus, BRICs have become new growth drivers for these countries.

12. This leads me to the second pillar of my presentation: tackling high unemployment, income inequality and poverty. Clearly, the issues are linked as limited productive employment opportunities for growing populations contributes to income inequality and poverty. High levels of unemployment are a major concern in many countries and have threatened political stability in the Middle East and North Africa. The challenges are especially difficult for a natural resource-rich economy like Botswana. The combination of a capital intensive mining sector and a “Dutch disease” effect has meant that job creation has not been sufficient to absorb the growing labor force. Moreover, in Botswana, key skills are still imported from abroad, as the skills of the local workforce do not fully match the demands of the labor market.

13. Another fundamental challenge is to ensure natural resource wealth is shared fairly across society. According to the last Household and Income Survey, about 30 percent of the population lives below the country-specific poverty line. Some estimates of the Gini-index suggest high income inequality. Poverty not only limits human development, it can also make countries more vulnerable to shocks—where fewer people have savings for a rainy day, more will suffer when the storm hits. Even in Asia, where remarkable economic advances over the last decades have lifted over half a billion people out of poverty, income inequality has been rising. The leaders of China and India have put tackling income disparities high on their policy agendas. And even in a wealthy nation like Singapore, Prime Minister Lee has noted that the widening income gap is an issue of national concern.

14. How best to respond to these challenges? There is no silver bullet. In broad terms, for Botswana, it is clear that there is a constraint posed by the relatively low growth in the non-mining sector on employment creation.

• This highlights the need to move ahead with reforms mentioned before, to foster private sector growth and economic diversification in order to enhance productivity and attract greater investment in labor intensive industries in the non-mining sector. Improving labor force skills by ensuring that the education system produces workers with skills that are in demand would seem to be critically important. Over the long haul, the most effective way to promote income growth at the lower end of the distribution is to invest in education and skills training in a manner that maximize returns on public spending. The 21st century economy is ultimately a knowledge economy, where returns to education and skills will be tremendously important.

• Policy measures directed at creating a better enabling environment for attracting more foreign direct investment (FDI) could also facilitate additional employment creation. Up until now, foreign direct investment in many countries in sub-Saharan Africa have largely gone to the natural resource sectors. The challenge is to attract more FDI in the non-diamond sectors to support Botswana’s economic diversification strategy. To make these new sectors key to sustained growth and employment creation, Botswana may also need to latch onto multinational supply chains while orchestrating them to local conditions as has been done by many Asian countries, in particular China. These possibilities of linking to global supply chains may be underexploited in the Southern African region and may merit active consideration. In the end, there is no single measure available to address unemployment, and only a combination of carefully designed initiatives as well as faster growth are likely to make significant inroads into unemployment.

15. I am glad to see that the government has initiated commendable efforts to address weaknesses in the labor market and tackle poverty as articulated in the Minister of Finance and Development Planning’s February 7 budget speech. Plans to create a Human Resource Development Council in 2012 could improve skills development. The establishment of a Labor Market Observatory also will enhance the dissemination of labor market information including vacancies, and thereby reduce frictional unemployment. Regarding poverty, there is a deliberate shift in government policy from poverty reduction to poverty eradication, signaling the growing priority to be given to poverty issues. In the context of the recent surge in food and fuel prices, consideration should be given to using fiscal resources to ameliorate the impact on the vulnerable groups. To make these policy initiatives more effective, it would be important to have a coherent and effective social safety net programs to ensure appropriate targeting and overall effectiveness of poverty eradication measures. The Botswana Core Welfare Indicator Survey expected in May 2011 will give an assessment of poverty levels, and should assist the government in making informed decisions on poverty eradication.

16. Finally, let me turn to the third pillar of my presentation namely, the need for stronger fiscal institutions. Strong institutions play a critical role in ensuring that well-designed policies are effective. Strong fiscal institutions help prevent excess spending in times of booms—thus leaving enough resources for times of need. Natural resource-rich economies are heavily affected by commodity prices which are highly volatile. Governments come under repeated political pressures to spend revenues arising from higher resource prices, which give rise to pro-cyclical fiscal policies and associated macroeconomic volatility that tend to adversely affect long-term growth. Yet international experience shows that policy choices are available to smooth this macroeconomic volatility in natural resource- rich economies.

17. Fortunately, Botswana has made significant progress in this area too. Currently, one key fiscal policy objective is to achieve an overall budget balance in Fiscal Year 2012–13. To further strengthen this framework, the IMF has suggested that greater prominence be also given to the non-mining fiscal balance in the formulation of fiscal policy. Decomposing the overall fiscal balance into a mining and a non-mining balance is critical for the interpretation of fiscal policy developments and for determining the macroeconomic impact of fiscal policy. Unlike the non-mining fiscal balance, the overall fiscal balance may not be a reliable indicator of: (i) the impact of fiscal policy on domestic demand, or (ii) the government’s adjustment effort. Indeed, in countries such as Norway, budget documents and fiscal policy discussions focus mainly on the non-oil balance and its impact on the domestic economy. Similarly, the cornerstone of Chile’s impressive fiscal performance has been its structural balance rule. By insulating public spending from short-term copper price fluctuations and the business cycle in Chile, the rule has by and large helped preserve fiscal discipline while leaving room for countercyclical fiscal policies.

18. Along with a budget balance rule, Botswana has introduced a fiscal rule limiting government expenditures to 40 percent of GDP. This rule has the advantage of being simple to understand, and it flags that there should be a balance between public spending and available resources, and between the government sector and the rest of the economy. At the same time, this rule tends to give rise to unintended procyclicality since when the price of diamonds increases, GDP also increases allowing an increase in spending. So one consideration is to complement this rule with a cap on real spending growth—some OECD countries do this (example, Australia and The Netherlands). These together would reduce procyclicality in fiscal policy.

19. A number of countries have faced similar issues as Botswana and as I have noted before, there are different ways to address them. While there is no one-size-fits-all, the key is to learn and draw from international experience. From this perspective, we believe that the critical components of a fiscal policy rule are: (i) a clear and, as simple as possible, set of operating fiscal variables and (ii) sufficient flexibility to respond to unanticipated shocks, so that the rule should not exacerbate the adverse macroeconomic impact of shocks, while avoiding procyclicality.

20. The budgets of many natural resource-rich economies are also typically characterized by short-term horizons, with little reference to longer-term policies and objectives. The achievement and monitoring of the long-term fiscal anchor could be supported by a full-fledged medium-term expenditure framework. Many OECD countries have adopted such medium-term frameworks. Adopting such a framework for fiscal policy formulation and budgeting in Botswana can help connect the annual budget to longer-term policies. This approach would need to be tailored to Botswana’s public financial management system which is undergoing reform. Given the uncertainty of how long higher commodity prices will last, it is important that spending remains restrained and guided by medium-term frameworks.

21. International experience also shows that natural resource revenue flows also create major challenges and opportunities for asset-liability management. The financial assets may be accumulated in the central bank as international reserves or in a sovereign wealth fund managed by a central bank or a separate entity. Over the course of decades, investment strategies or strategic asset allocation framework can make a significant difference to the returns from the natural resources. It can also potentially offset some of the volatility in the revenues. Although Botswana does not have a formal sovereign wealth fund, it has developed a good reputation for managing its accumulated financial assets, which is divided into the Liquidity portfolio designed as a buffer against short-term trade and capital-account fluctuations, and the Pula fund designed to contribute to long-term development by diversifying income away from commodities into global financial assets. This said, like many resource-rich countries, Botswana has access to debt financing options and has indeed begun to contract external debt. Going forward, fiscal institutions could be strengthened by establishing a comprehensive framework for the public sector’s asset and liability management. To support our member’s efforts in this area, the IMF is planning to establish a multi donor trust fund to provide natural resource-rich countries with technical assistance on asset-liability management and related issues.

22. In closing, I would like to emphasize that all of these are serious policy challenges. But they are not insurmountable. The 10th National Development Plan (NDP10) and most recently the Fiscal Year 2011 to 12 Budget Speech by Minister Matambo, nicely describe the government’s plans to face these challenges. The IMF hopes to contribute to this through our surveillance work and technical assistance, as you work to realize this Vision.

23. Thank you.