Table 1.1. Overview of the World Economic Outlook Projections

(Percent change, unless otherwise noted)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

| |

Year over Year |

|

Q4 over Q4 |

| |

|

|

Projections |

|

Difference from

October 2009 WEO Projections |

|

Estimates |

|

Projections |

| |

2008 |

2009 |

2010 |

2011 |

|

2010 |

2011 |

|

2009 |

|

2010 |

2011 |

| |

|

World output1 |

3.0 |

-0.8 |

3.9 |

4.3 |

|

0.8 |

0.1 |

|

1.3 |

|

3.9 |

4.3 |

|

Advanced economies |

0.5 |

-3.2 |

2.1 |

2.4 |

|

0.8 |

-0.1 |

|

-0.7 |

|

2.1 |

2.5 |

|

United States |

0.4 |

-2.5 |

2.7 |

2.4 |

|

1.2 |

-0.4 |

|

-0.3 |

|

2.6 |

2.4 |

|

Euro area |

0.6 |

-3.9 |

1.0 |

1.6 |

|

0.7 |

0.3 |

|

-1.8 |

|

1.1 |

1.8 |

|

Germany |

1.2 |

-4.8 |

1.5 |

1.9 |

|

1.2 |

0.4 |

|

-1.9 |

|

1.0 |

2.5 |

|

France |

0.3 |

-2.3 |

1.4 |

1.7 |

|

0.5 |

-0.1 |

|

-0.5 |

|

1.6 |

1.6 |

|

Italy |

-1.0 |

-4.8 |

1.0 |

1.3 |

|

0.8 |

0.6 |

|

-2.4 |

|

1.3 |

1.1 |

|

Spain |

0.9 |

-3.6 |

-0.6 |

0.9 |

|

0.1 |

0.0 |

|

-3.1 |

|

0.1 |

1.2 |

|

Japan |

-1.2 |

-5.3 |

1.7 |

2.2 |

|

0.0 |

-0.2 |

|

-1.8 |

|

1.8 |

2.5 |

|

United Kingdom |

0.5 |

-4.8 |

1.3 |

2.7 |

|

0.4 |

0.2 |

|

-2.8 |

|

1.9 |

3.1 |

|

Canada |

0.4 |

-2.6 |

2.6 |

3.6 |

|

0.5 |

0.0 |

|

-1.6 |

|

3.6 |

3.5 |

|

Other advanced economies |

1.7 |

-1.3 |

3.3 |

3.6 |

|

0.7 |

-0.1 |

|

3.0 |

|

2.7 |

4.0 |

|

Newly industrialized Asian economies |

1.7 |

-1.2 |

4.8 |

4.7 |

|

1.2 |

0.0 |

|

5.8 |

|

3.1 |

5.4 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Emerging and developing economies2 |

6.1 |

2.1 |

6.0 |

6.3 |

|

0.9 |

0.2 |

|

4.3 |

|

6.4 |

6.9 |

|

Africa |

5.2 |

1.9 |

4.3 |

5.3 |

|

0.3 |

0.1 |

|

... |

|

... |

... |

|

Sub-Sahara |

5.6 |

1.6 |

4.3 |

5.5 |

|

0.2 |

0.0 |

|

... |

|

... |

... |

|

Central and eastern Europe |

3.1 |

-4.3 |

2.0 |

3.7 |

|

0.2 |

-0.1 |

|

1.2 |

|

-0.2 |

5.9 |

|

Commonwealth of Independent States |

5.5 |

-7.5 |

3.8 |

4.0 |

|

1.7 |

0.4 |

|

... |

|

... |

... |

|

Russia |

5.6 |

-9.0 |

3.6 |

3.4 |

|

2.1 |

0.4 |

|

-6.2 |

|

2.4 |

4.3 |

|

Excluding Russia |

5.3 |

-3.9 |

4.3 |

5.1 |

|

0.7 |

0.1 |

|

... |

|

... |

... |

|

Developing Asia |

7.9 |

6.5 |

8.4 |

8.4 |

|

1.1 |

0.3 |

|

... |

|

... |

... |

|

China |

9.6 |

8.7 |

10.0 |

9.7 |

|

1.0 |

0.0 |

|

10.7 |

|

9.3 |

9.4 |

|

India |

7.3 |

5.6 |

7.7 |

7.8 |

|

1.3 |

0.5 |

|

5.9 |

|

9.6 |

8.3 |

|

ASEAN-53 |

4.7 |

1.3 |

4.7 |

5.3 |

|

0.7 |

0.6 |

|

3.6 |

|

4.8 |

5.5 |

|

Middle East |

5.3 |

2.2 |

4.5 |

4.8 |

|

0.3 |

0.2 |

|

... |

|

... |

... |

|

Western Hemisphere |

4.2 |

-2.3 |

3.7 |

3.8 |

|

0.8 |

0.1 |

|

... |

|

... |

... |

|

Brazil |

5.1 |

-0.4 |

4.7 |

3.7 |

|

1.2 |

0.2 |

|

3.1 |

|

3.9 |

3.7 |

|

Mexico |

1.3 |

-6.8 |

4.0 |

4.7 |

|

0.7 |

-0.2 |

|

-3.0 |

|

3.2 |

5.4 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Memorandum |

|

|

|

|

|

|

|

|

|

|

|

|

|

European Union |

1.0 |

-4.0 |

1.0 |

1.9 |

|

0.5 |

0.1 |

|

-1.9 |

|

1.3 |

2.2 |

|

World growth based on market exchange rates |

1.8 |

-2.1 |

3.0 |

3.4 |

|

0.7 |

0.0 |

|

... |

|

... |

... |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

World trade volume (goods and services) |

2.8 |

-12.3 |

5.8 |

6.3 |

|

3.3 |

1.1 |

|

... |

|

... |

... |

|

Imports |

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

0.5 |

-12.2 |

5.5 |

5.5 |

|

4.3 |

1.1 |

|

... |

|

... |

... |

|

Emerging and developing economies |

8.9 |

-13.5 |

6.5 |

7.7 |

|

1.9 |

1.3 |

|

... |

|

... |

... |

|

Exports |

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

1.8 |

-12.1 |

5.9 |

5.6 |

|

3.9 |

0.5 |

|

... |

|

... |

... |

|

Emerging and developing economies |

4.4 |

-11.7 |

5.4 |

7.8 |

|

1.8 |

2.0 |

|

... |

|

... |

... |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Commodity prices (U.S. dollars) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Oil4 |

36.4 |

-36.1 |

22.6 |

7.9 |

|

-1.7 |

4.0 |

|

... |

|

... |

... |

|

Nonfuel (average based on world |

|

|

|

|

|

|

|

|

|

|

|

|

|

commodity export weights) |

7.5 |

-18.9 |

5.8 |

1.6 |

|

3.4 |

-1.3 |

|

... |

|

... |

... |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Consumer prices |

|

|

|

|

|

|

|

|

|

|

|

|

|

Advanced economies |

3.4 |

0.1 |

1.3 |

1.5 |

|

0.2 |

0.2 |

|

0.7 |

|

1.2 |

1.5 |

|

Emerging and developing economies2 |

9.2 |

5.2 |

6.2 |

4.6 |

|

1.3 |

0.1 |

|

4.7 |

|

6.5 |

3.0 |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

London interbank offered rate (percent)5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

On U.S. dollar deposits |

3.0 |

1.1 |

0.7 |

1.8 |

|

-0.7 |

-1.6 |

|

... |

|

... |

... |

|

On euro deposits |

4.6 |

1.2 |

1.3 |

2.3 |

|

-0.3 |

-0.4 |

|

... |

|

... |

... |

|

On Japanese yen deposits |

1.0 |

0.7 |

0.6 |

0.7 |

|

0.0 |

0.0 |

|

... |

|

... |

... |

| |

|

Note: Real effective exchange rates are assumed to remain constant at the levels prevailing during November 19-December 17, 2009. Country weights used to construct aggregate growth rates for groups of countries were revised. When economies are not listed alphabetically, they are ordered on the basis of economic size. |

|

1The quarterly estimates and projections account for 90 percent of the world purchasing-power-parity weights. |

|

2The quarterly estimates and projections account for approximately 77 percent of the emerging and developing economies. |

|

3Indonesia, Malaysia, Philippines, Thailand, and Vietnam. |

|

4Simple average of prices of U.K. Brent, Dubai, and West Texas Intermediate crude oil. The average price of oil in U.S. dollars a barrel was $62.00 in 2009; the assumed price based on future markets is $76.00 in 2010 and $82.00 in 2011. |

|

5Six-month rate for the United States and Japan. Three-month rate for the euro area. |

Recovery is proceeding at varying speeds

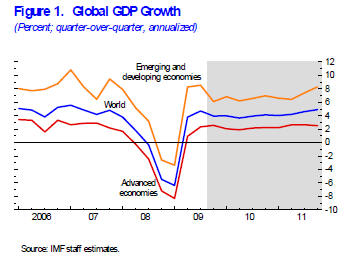

Output in the advanced economies is now expected to expand by 2 percent in 2010, following a sharp decline in output in 2009. The new forecast reflects an upward revision of 3/4 percentage point. In 2011, growth is projected to edge up further to 2½ percent. In spite of the revision, the recovery in advanced economies is still expected to be weak by historical standards, with real output remaining below its pre-crisis level until late 2011. Moreover, high unemployment rates and public debt, as well as not-fully-healed financial systems, and in some countries, weak household balance sheets are presenting further challenges to the recovery in these economies.

Growth in emerging and developing economies is expected to rise to about 6 percent in 2010, following a modest 2 percent in 2009. The new projection reflects an upward revision of almost 1 percentage point. In 2011, output is projected to accelerate further. Stronger economic frameworks and swift policy responses have helped many emerging economies to cushion the impact of the unprecedented external shock and quickly re-attract capital flows.

Within both groups, growth performance is expected to vary considerably across countries and regions, reflecting different initial conditions, external shocks, and policy responses. For instance, key emerging economies in Asia are leading the global recovery. A few advanced European economies and a number of economies in central and eastern Europe and the Commonwealth of Independent States are lagging behind. The rebound of commodity prices is helping support growth in commodity producers in all regions. Many developing countries in sub-Saharan Africa that experienced only a mild slowdown in 2009 are well placed to recover in 2010. Growth paths are diverse for advanced economies as well.

Financial conditions have improved further but remain challenging

Financial markets have recovered faster than expected, helped by strengthening activity. Nevertheless, financial conditions are likely to remain more difficult than before the crisis (see January 2010 Global Financial Stability Report Market Update). Specifically:

- Money markets have stabilized, and the tightening of bank lending standards has moderated. Moreover, most banks in core markets are now less reliant on central bank emergency facilities and government guarantees. Nonetheless, bank lending is likely to remain sluggish, given the need to rebuild capital, the weakness of private securitization, and the possibility of further credit write-downs, notably related to commercial real estate.

- Equity markets have rebounded, and corporate bond issuance has reached record levels, amid a reopening of most high-yield markets. However, the surge in corporate bond issuance has not offset the reduction in bank credit growth to the private sector. Those sectors that have only limited access to capital markets, namely consumers and small and medium-size enterprises, are likely to continue to face credit constraints. So far, public lending programs and guarantees have been critical in channeling credit to these sectors.

- Sovereign debt has come under pressure for some small countries, as they struggle with large government deficits and debt, and as investors increasingly differentiate across countries.

Amid a relatively rapid return to healthy growth in many emerging economies, portfolio flows into these markets have picked up, easing financial conditions and prompting nascent concerns about asset price valuations. By contrast, cross-border bank financing is still contracting in most regions, as global banks continue to delever. This will limit domestic credit growth, especially in regions that had been most reliant on cross-border bank flows.

Commodity prices are rebounding

Commodity prices rose strongly during the early stages of the recovery, despite generally high inventories. To a large extent, this was due to the buoyant recovery in emerging Asia, to the onset of recovery in other emerging and developing economies more generally, and to the improvement in global financial conditions.

Looking ahead, commodity prices are expected to rise a bit further supported by the strength of global demand, especially from emerging economies. However, this upward pressure is expected to be modest, given the above-average inventory levels and substantial spare capacity in many commodity sectors. Accordingly, the IMF’s baseline petroleum price projection is unchanged for 2010 and revised up by a small amount in 2011 (to $82 a barrel, from $79 a barrel in the October 2009 WEO). Other non-fuel commodity prices have also been marked up modestly.

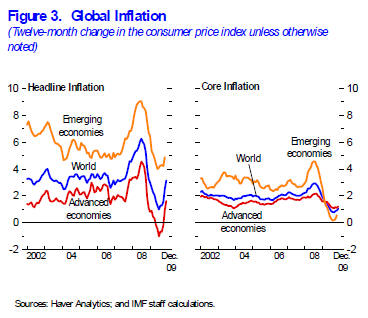

Inflation pressures will remain subdued in most economies

The still-low levels of capacity utilization and well-anchored inflation expectations are expected to contain inflation pressures (Figure 3, view: Data Figure 3). In the advanced economies, headline inflation is expected to pick up from zero in 2009 to 1¼ percent in 2010, as rebounding energy prices more than offset slowing labor costs. In emerging and developing economies, inflation is expected to edge up to 6¼ percent in 2010, as some of these economies may face growing upward pressures due to more limited economic slack and increased capital flows.

There are important risks in both directions

There are still significant risks to the outlook.

On the upside, the reversal of the confidence crisis and the reduction in uncertainty may continue to foster a stronger-than-expected improvement in financial market sentiment and prompt a larger-than-expected rebound in capital flows, trade, and private demand. New policy initiatives in the United States to reduce unemployment could provide a further impetus to both U.S. and global growth.

On the downside, a key risk is that a premature and incoherent exit from supportive policies may undermine global growth and its rebalancing. Another important risk is that impaired financial systems and housing markets or rising unemployment in key advanced economies may hold back the recovery in household spending more than expected. In addition, rising concerns about worsening budgetary positions and fiscal sustainability could unsettle financial markets and stifle the recovery by raising the cost of borrowing for households and companies. Yet another downside risk is that rallying commodity prices may constrain the recovery in advanced economies.

Continued policy efforts are needed to sustain the recovery and prepare for exit

Against this backdrop, policymakers are faced with the daunting policy challenge of achieving the rebalancing of demand away from public and toward private sectors and away from economies with excessive external deficits toward those with excessive surpluses, while repairing financial sectors and fostering restructuring in real sectors. Both rebalancing acts are, however, not proceeding without problems. Many advanced economies continue to struggle with repairing and reforming their financial sectors. Concurrently, various emerging economies are grappling with the challenges posed by surging capital inflows, in some cases resisting exchange rate appreciation that could support stronger domestic demand and a reduction in excessive current account surpluses.

Regarding monetary policy, many central banks can afford to maintain low interest rates over the coming year, as underlying inflation is expected to remain low and unemployment high for some time. At the same time, credible strategies for unwinding monetary policy support need to be prepared and communicated now to anchor expectations and dampen potential fears of inflation or renewed financial instability. Countries that are already enjoying a relatively robust rebound of activity and credit will have to tighten monetary conditions earlier and faster than their counterparts elsewhere.

Due to the still-fragile nature of the recovery, fiscal policies need to remain supportive of economic activity in the near term. The fiscal stimulus planned for 2010 should be fully implemented. However, countries facing growing concerns about fiscal sustainability should make progress in devising and communicating credible exit strategies. In many cases, durable exit will require not only unwinding crisis-related fiscal stimulus but also substantial improvements in primary balances for a sustained period. Fiscal adjustment strategies should include: reducing fiscal deficits mindful of the need to protect spending on the poor and foreign aid and reforming entitlement spending, among others measures.

Once private demand has become self-sustained, the sequencing of exit from accommodative monetary and fiscal policy should be guided by a variety of considerations, including whether: high fiscal deficits and debt are raising concerns about sustainability and sovereign risk—which is the primary consideration in many countries; low interest rates might be contributing to asset price bubbles; the exchange rate is under pressure to appreciate or depreciate as well as its position relative to medium-term fundamentals; and how quickly monetary or fiscal policy can be adjusted to changes in domestic demand.

Crucially, there remains a pressing need to continue repairing the financial sector in advanced and the hardest-hit emerging economies. In these cases, policies are still needed to tackle bank’ impaired assets and restructuring. Unwinding the financial sector support measures put in place since the start of the crisis should be gradual; it can be facilitated by incentives that make measures less attractive as conditions improve. Policymakers will also need to move boldly to reform the financial sector with the objectives of reducing the risks of future instability and rethinking how the potential fallout of financial crises would be borne in the future, while at the same time making the sector more effective and resilient.

At the same time, some emerging market countries will have to manage a surge of capital inflows. This is a complex task and the right responses differ across countries, including some fiscal tightening to ease pressure on interest rates and exchange rate appreciation or greater flexibility. Recognizing that inflows can be very large and partly transitory, depending on circumstances, macro-prudential policies aimed at limiting the emergence of new asset price bubbles, some buildup of reserves, and some capital controls on inflows can be part of the appropriate response.

Lastly, policymakers are facing major structural policy challenges. In advanced and emerging economies with excessive external surpluses and domestic saving rates, global rebalancing could be fostered through structural policies to support domestic demand and the development of non-tradable sectors. On the other hand, economies that relied excessively on domestic demand-led growth will need to shift resources toward the tradable sector.