(Versions in عربي, 中文, Français, Русский, 日本語and Español)

Anyone can easily picture an economy where instability, stagnation and runaway government deficits converge into a perfect storm. Yet the simple mirror image of stability, growth, and balanced budgets currently seems odd to many. And with monetary policy looking breathless, some even wonder whether sacrificing fiscal sanity for short-term growth might not be worth a try.

In any economic debate, looking at the data is always a good starting point. And the latest issue of the Fiscal Monitor does exactly that. Our study looks at the experience with fiscal stabilization during the past three decades in a broad sample of 85 advanced, emerging market, and developing economies. The message is loud and clear: governments can use fiscal policy to smooth fluctuations in economic activity, and this can lead to higher medium-term growth. This essentially means governments need to save in good times so that they can use the budget to stabilize output in bad times. In advanced economies, making fiscal policies more stabilizing could cut output volatility by about 15 percent, with a growth dividend of about 0.3 percentage point annually.

Of course, using the budget to stabilize output requires healthy public accounts that can take hard hits during severe storms. And when the sunshine returns, policymakers must be wise enough to repair public accounts in preparation for future storms. That’s how stability, growth, and sustainability go hand in hand.

How does fiscal policy stabilize output?

Fiscal policy has a stabilizing effect on an economy if the budget balance—the difference between expenditure and revenue—increases when output rises and decreases when it falls. For instance, if output suddenly contracts, policymakers can let tax revenues fall along with income (or even deliberately cut tax rates) and let unemployment benefits increase with the number of unemployed. This maintains income and purchasing power for individuals, and supports demand. Policymakers can also raise demand directly by deliberately spending more. Either way, higher deficit (or a lower surplus) effectively cushions the blow on output.

The response of the government budget balance to economic activity is clearly the key to understanding the contribution of fiscal policy to output stability. To gauge overall fiscal stabilization, our study measured the impact of what a one percentage-point change in output can have on the budget balance (in percent of GDP). For example, a coefficient equal to 1 means that the fiscal response is exactly of the same size as the initial shock. Chart 1 shows that these so-called “fiscal stabilization coefficients” can be quite sizable, especially in advanced economies. However, in emerging markets and developing economies fiscal stabilization is generally more modest and less frequent, though there are some that have large coefficients.

The overall reduction in output volatility due to fiscal stabilization is evident from simple cross-country correlations between volatility and the stabilization coefficients (see chart 2), which are clearly negative. The analysis in the Fiscal Monitor also suggests that a more stable macroeconomic environment created by fiscal stabilization has positive effects on medium-term growth. One plausible explanation is that less uncertainty tends to encourage investment in all its forms (physical, human, and social).

Adapting fiscal policy

Continuously adapting fiscal policy to output variations looks impossible to do in practice. It would seem to require definite responses to a long list of “How To” questions: How to gauge the state of the economy in real time? How to design the appropriate policy response? How to ensure political approval? How to implement it in a timely manner?

In fact, it is not so complicated, thanks to automatic stabilizers which comprise tax payments that move in sync with income and spending, and social transfers, such as unemployment benefits which automatically boost aggregate demand during downturns and moderate them during upswings. It is because they operate in real time, without decision or implementation lags, that they are a very effective way to make fiscal policy stabilizing.

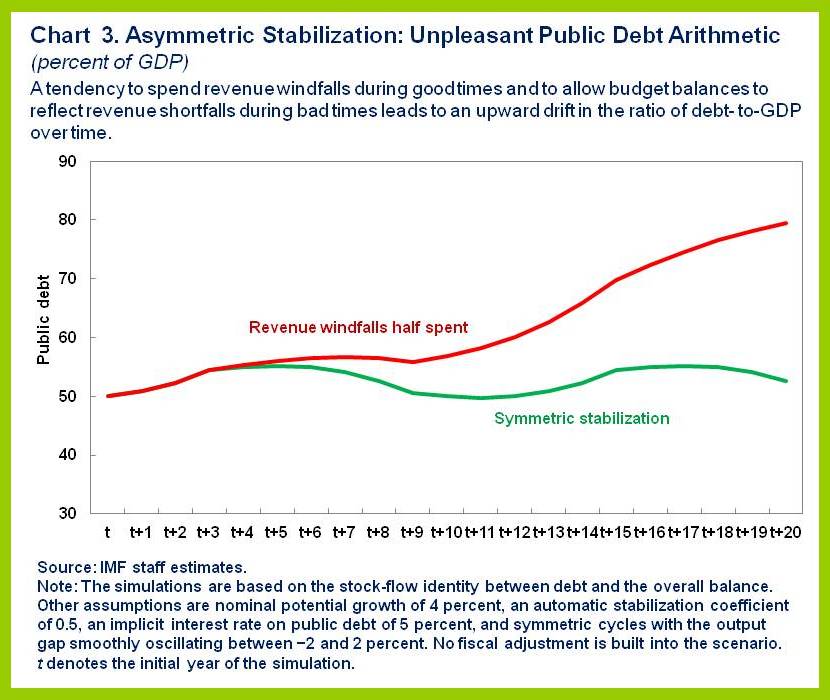

Yet fiscal actions often end up undermining automatic stabilizers. A widespread tendency to spend the revenue windfalls during good times is the main culprit. This is not just bad for output stability; it is also bad for public debt. The figure below is striking. The simulations first describe a stable public debt path over time. It reflects “symmetric stabilization” because deficit reductions in good times fully offset deficit increases in bad times. Debt can also go on an upward path by spending just half of the revenue increases (due to above average growth) while letting deficits fully absorb the impact of downturn.

Steady as she grows

The policy implications are clear. Stability, growth and debt sustainability could all greatly benefit if measures that destabilizes output, such as spending increases in good times, were avoided. That’s the kind of policies a well-designed fiscal framework can encourage (see the recent blog by Vitor Gaspar, Richard Hughes and Laura Jaramillo on Dams and Dikes for Public Finances). Countries could also augment automatic stabilizers but this should not be done through undue increases in taxes and transfer programs, which can have undesirable side effects on growth and employment. The Fiscal Monitor discusses options to boost stabilizers while avoiding these caveats. A good starting point would be preventing certain tax deductions from increasing during booms and decreasing during recessions.