July 18, 2018

Versions in عربي, 中文, Español, Français 日本語, Português, Русский

[caption id="attachment_24063" align="alignnone" width="1024"] Cars to be shipped abroad, Jiangsu, China: trade tariffs have gone into effect and export orders have decreased (photo: Imagine China/Newscom) [/caption]

Cars to be shipped abroad, Jiangsu, China: trade tariffs have gone into effect and export orders have decreased (photo: Imagine China/Newscom) [/caption]

The artist Claude Monet once said, “I worked without stopping, for the tide at this moment is just as I need it.” As the Group of Twenty finance ministers gather this week at the banks of the Rio de la Plata in Buenos Aires they should be inspired by the words of Monet, and take advantage of global growth before the tides change.

On Monday, the IMF released its World Economic Outlook Update that confirmed the April forecast of 3.9 percent global growth for 2019. But this may be the high-water mark. Already growth is beginning to slow in the Euro Area, Japan, and the United Kingdom. US growth, which has been boosted by the recent fiscal stimulus, is projected to moderate in the medium term. In the emerging markets, growth is now more uneven than it was in April, due in part to rising oil prices and currency pressures.

So, the G-20 finance ministers have a full agenda heading into their meeting in Argentina. Where should they concentrate their efforts? There are three major areas where they can make progress this week: Global trade, emerging market vulnerabilities, and the impact of technology on jobs.

Take advantage of global growth before the tides change.

Global trade

Trade tensions are already leaving a mark, but the extent of the damage depends on what policymakers do next. In April, the IMF warned against the self-inflicted economic wounds that result from protectionist measures. Unfortunately, the rhetoric has morphed into reality, and a series of tariffs and counter-tariffs have gone into effect over the last month. Recent data from Europe and Asia points to a decrease in new export orders and wavering confidence among some car-exporting countries, including Germany.

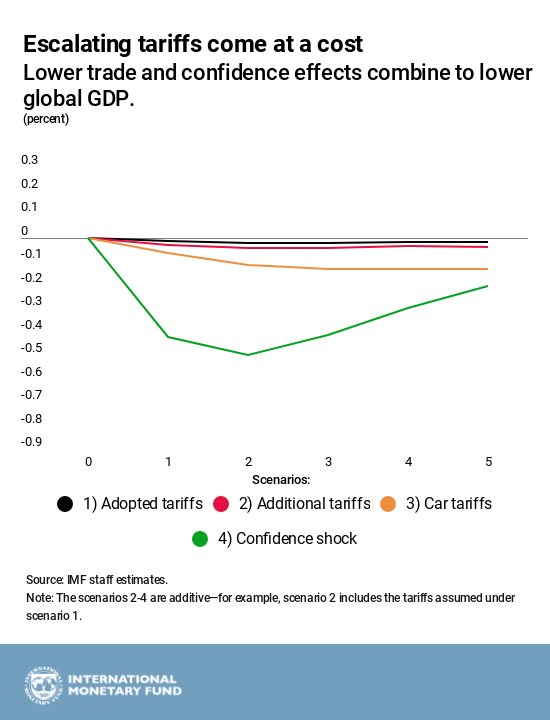

Our G-20 Surveillance Note, released today, simulates four hypothetical trade scenarios for the global economy. Under one scenario, if all currently announced tariffs go into effect, global output would be reduced by 0.1 percent in 2020. And if investor confidence is shaken by these tariffs, our simulation shows that global GDP could decrease by ½ percent—or roughly US$430 billion—below the current projection for 2020.

Our analysis also looked at the impact by region. While all countries will ultimately be worse off in a trade conflict, the US economy is especially vulnerable because so much of its global trade will be subject to retaliatory measures. And GDP loss is not the only cost.

Amidst the churn of trade tensions, we are now in danger of losing sight of the horizon. As I said recently, “The future of trade is the future of data.” Modernizing trade rules to address intellectual property rights and adopting innovative agreements on e-commerce and digital services should be at the center of trade discussions. Policymakers can use this G-20 meeting to move past self-defeating tit-for-tat tariffs and instead develop multilateral solutions that will improve the global trading system.

Emerging market vulnerabilities

Conflicts over trade are also exacerbating an already complicated situation in emerging markets. Rising interest rates in the US have put pressure on many developing economies, including Brazil and Turkey. In total, investors withdrew over 14 billion dollars from emerging markets in May and June of this year. In response, policymakers in several emerging markets have raised interest rates and some have directly intervened to support their domestic currency.

To date, most of the pressure has been limited to a few countries and is nowhere near as widespread as the Taper Tantrum of 2013. However, as US interest rates continue to rise there is a risk that more countries could face increased pressure. What can emerging markets do? Use all the tools at their disposal.

- Exchanges rates should remain flexible and act as a shock absorber to help countries weather the departure of investors’ money.

- Regulators should coordinate to prevent excessive credit growth from turning into another crisis, including by ensuring liquidity in financial markets.

- With high debt levels in many countries, fiscal policy should be used to preserve and rebuild buffers where needed.

The IMF will continue to provide guidance in this area, and we are committed to doing everything we can to help our members strengthen their economies and increase resilience in the face of headwinds.

The impact of technology on jobs

Even as we confront the immediate threats to the global economy we cannot afford to ignore the long-term challenges. One of these is the impact of technology on jobs. Advances in artificial intelligence and automation all promise to raise productivity and growth—but what happens next? As workers lose jobs inequality could worsen and in turn our social fabric may fray even further.

The first step to solving the problem is understanding its size. Our new G-20 paper on the future of work shows that many nations are not getting an accurate picture of how technology is changing the workforce.

Labor market statistics are hampered by a lack of information about the scope of the gig economy. Meanwhile estimates of our productivity—the value added to the economy from our work—often overlook the way technology is increasing efficiency. Think of your digital watch, for example. The word watch does not fully capture its value. In 2018 your watch can also be a cellphone, a movie theater, a navigation tool, and a supercomputer. Our statistics sometimes miss this reality.

Of course, better measurements are only part of the puzzle. Any new data will be wasted without bold actions that help citizens deal with the consequences of automation and the disruptions that come from new technologies. These actions include modernizing social safety nets, reforming education systems to provide for lifelong learning, and committing to major investments in digital infrastructure. Singapore, which is participating in this year’s G-20, is a good model. Over the last decade Singapore has made infrastructure a priority and today they possess the most advanced digital infrastructure of any nation in the world.

There is no doubt that each country has different gaps to fill but one thing is clear for all countries—it is time to prepare for the technological disruption that will only accelerate in the years ahead.

I believe we can manage all the challenges facing the global economy—and even turn them into advantages—but only if we recognize that this moment of growth will not last forever.

Each day when the tide recedes the shoreline is revealed. The question for the G-20 members is what will they choose to build along that shoreline. Will it be a fragile system susceptible to storms or a solid economic foundation as reliable as bedrock? Since the Global Financial Crisis nearly ten years ago the G-20 nations have consistently chosen the latter, and in the process, they have made a positive difference for billions of people around the world. I trust the finance ministers will continue on this path in the days ahead and make the most of their opportunity in Buenos Aires.