The pandemic-induced economic crisis is set to leave deep scars. Human capital erosion from prolonged high unemployment and school closures, value destruction from bankruptcies, and constraints on future fiscal policy from elevated public debt top the list. Groups that were already poor and vulnerable are set to see the largest setbacks.

Swift and unprecedented action by policymakers, including among the Group of Twenty (G20) advanced and emerging market economies, helped avert an even worse economic crisis in the wake of COVID-19 than what has been witnessed. The G20 has provided around US$11 trillion in necessary support to individuals, businesses, and the healthcare sector since the start of the pandemic.

However, much of the fiscal support is now gradually winding down, and many benefits such as cash transfers to households, deferred tax payments, or temporary loans to businesses have expired or are set to expire by the end of this year.

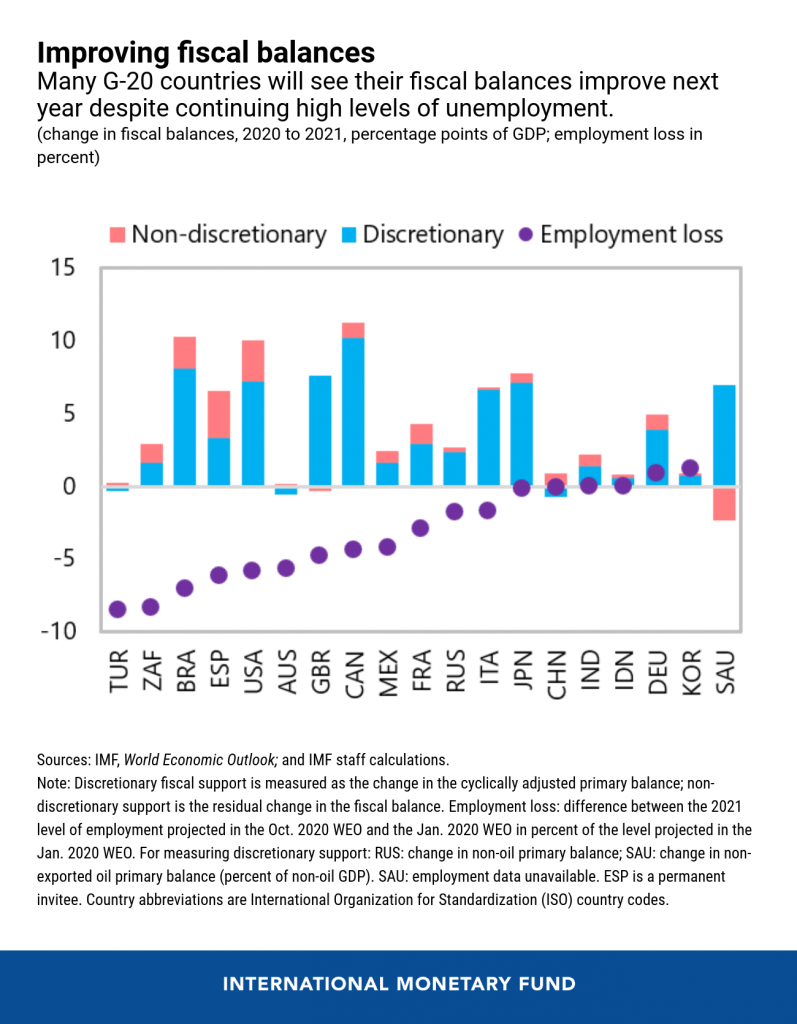

The analysis in our G20 Report on Strong, Sustainable, Balanced, and Inclusive Growth illustrates how fiscal deficits in almost all G20 economies are projected to shrink next year, based on announced budgets and current policies.

In economies where deficits widened sharply this year, fiscal balances are now expected to narrow by more than 5 percent of GDP in 2021. While part of this reflects that growth is projected to strengthen, the largest contributor to improving fiscal balances is a sharp withdrawal of “discretionary” support—relief measures that had been introduced to counter the effects of the crisis.

This withdrawal of support is occurring at a time when employment losses from the crisis are still projected to be sizable, as evidenced by massive shortfalls in projected employment relative to pre-pandemic trends.

So, what is to be done?

First, support should be maintained throughout the crisis. A premature withdrawal of support would impose further harm on livelihoods and heighten the likelihood of widespread bankruptcies, which in turn could jeopardize the recovery. In such a scenario, the scars from the crisis would likely become much deeper. Where possible, economies should therefore resist tightening fiscal policy too early and instead ensure continued support for healthcare, individuals, and firms. In economies constrained in their ability to spend, a reprioritization of spending may be warranted to protect the most vulnerable.

Second, as we begin to gradually understand what’s in store in the post-pandemic world, policies will need to be geared toward the new reality and build resilience. For instance, policies that promote investment and hiring in expanding sectors and provide reskilling and training opportunities to the unemployed will strengthen the recovery and make it more sustainable. Investments to promote decarbonization can not only lift employment in the near term but also increase resilience down the road.

The road to strong, sustainable, balanced, and inclusive growth will be long and difficult. Now is the time to spend wisely and work together to build a better future.