Credit MicroStockHub/iStock by Getty Images

Credit MicroStockHub/iStock by Getty Images

Mutual funds that allow investors to buy or sell their shares daily are an important component of the financial system, offering investment opportunities to investors and providing financing to companies and governments.

Open-end investment funds, as they are known, have grown significantly in the past two decades, with $41 trillion in assets globally this year. That represents about one-fifth of the nonbank financial sector’s holdings.

These funds may invest in relatively liquid assets such as stocks and government bonds, or in less-frequently-traded securities like corporate bonds. Those with less-liquid holdings, however, have a major potential vulnerability. Investors can sell shares daily at a price set at the end of each trading session, but it may take fund managers several days to sell assets to meet these redemptions, especially when financial markets are volatile.

Such liquidity mismatch can be a big problem for fund managers during periods of outflows because the price paid to investors may not fully reflect all trading costs associated with the assets they sold. Instead, the remaining investors bear those costs, creating an incentive for redeeming shares before others do, which may lead to outflow pressures if market sentiment dims.

Pressures from these investor runs could force funds to sell assets quickly, which would further depress valuations. That in turn would amplify the impact of the initial shock and potentially undermine the stability of the financial system.

Illiquidity and volatility

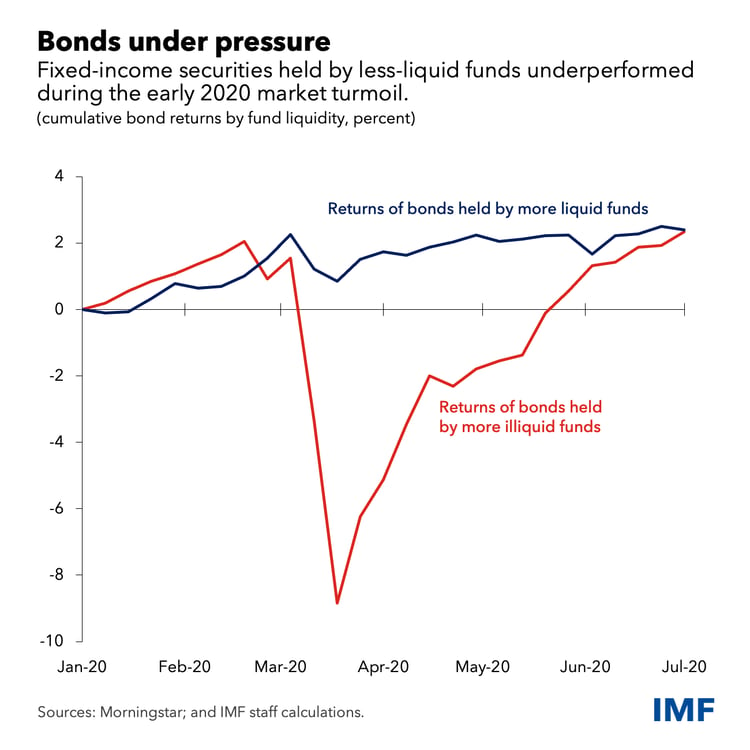

That’s likely the dynamic we saw at play during the market turmoil at the start of the pandemic, as we write in an analytical chapter of the Global Financial Stability Report. Open-end funds were forced to sell assets amid outflows of about 5 percent of their total net asset value, which topped global financial crisis redemptions a decade and a half earlier.

Consequently, assets such as corporate bonds that were held by open-end funds with less-liquid assets in their portfolios fell more sharply in value than those held by liquid funds. Such dislocations posed a serious risk to financial stability, which were addressed only after central banks intervened by purchasing corporate bonds and taking other actions. Looking beyond the pandemic-induced market turmoil, our analysis shows that the returns of assets held by relatively illiquid funds are generally more volatile than comparable holdings that are less exposed to these funds—especially in periods of market stress. For example, if liquidity dries up the way it did in March 2020, the volatility of bonds held by these funds could increase by 20 percent.

This is also of concern to emerging market economies. A decline in the liquidity of funds domiciled in advanced economies can have significant cross-border spillover effects and increase the return volatility of emerging market corporate bonds.

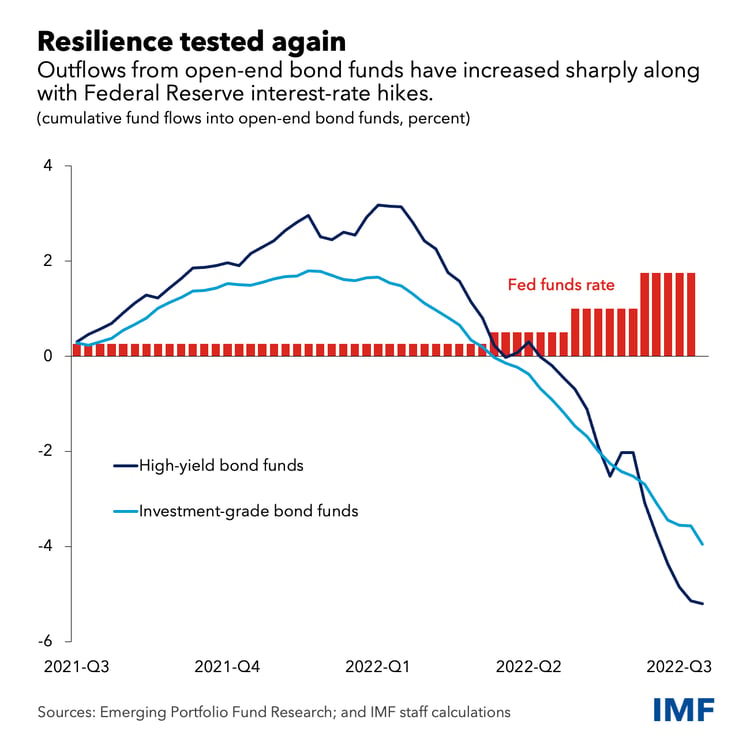

Now the resilience of the open-end fund sector may again be tested, this time amid rising interest rates and high economic uncertainty. Outflows from open-end bond funds have increased in recent months, and a sudden, adverse shock like a disorderly tightening of financial conditions could trigger further outflows and amplify stress in asset markets.

As IMF Managing Director Kristalina Georgieva said in a speech last year, “policymakers worked together to make banks safer after the global financial crisis—now we must do the same for investment funds.”

How should those risks be curbed?

As we write in the chapter, asset volatility induced by open-end funds can be reduced if funds pass on transaction costs to redeeming investors. For example, a practice known as swing pricing allows funds to adjust their end-of-day price downward when facing outflows. This reduces the incentive for investors to redeem before others. Doing so eases outflow pressures faced by funds in times of stress, and the likelihood of forced asset sales.

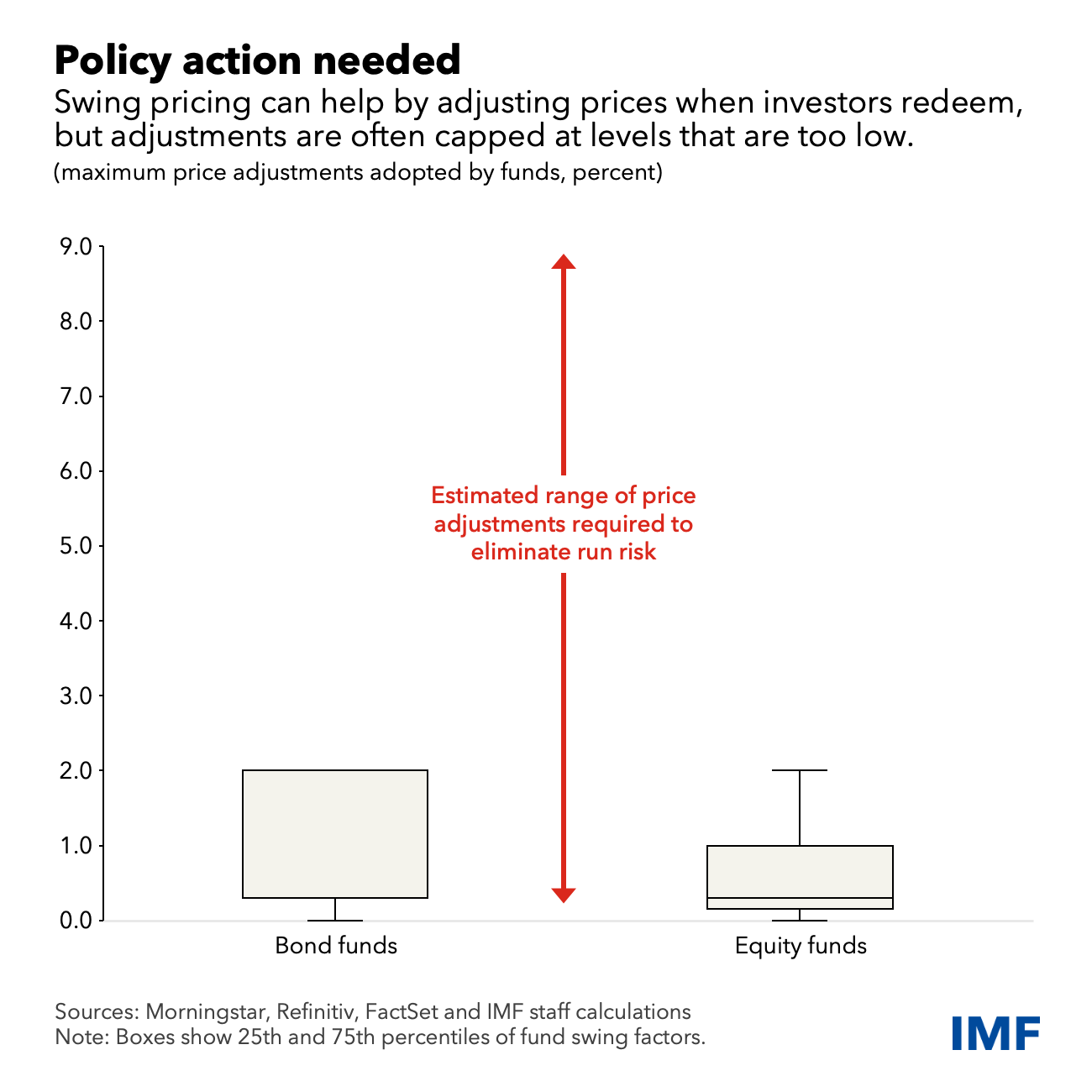

But while swing pricing—and similar tools such as antidilution levies, which pass on transaction costs to redeeming investors by charging a fee—can help mitigate financial stability risks, they must be appropriately calibrated to do so, and that’s not the case right now.

The adjustments that funds can make to the end-of-day prices—known as swing factors—are often capped at insufficient levels, especially in times of market stress. Policymakers therefore need to provide guidance on how to calibrate these tools and monitor their implementation.

For funds holding very illiquid assets, such as real estate, calibrating swing-pricing or similar tools may be difficult even in normal times. In these cases, alternative policies should be considered, like limiting the frequency of investor redemptions. Such policies may also be suitable for funds based in jurisdictions where swing pricing cannot be implemented for operational reasons.

Policymakers should also consider tighter monitoring of liquidity management practices by supervisors and requiring additional disclosures by open-end funds to better assess vulnerabilities. Furthermore, encouraging more trading through central clearinghouses and making bond trades more transparent could help boost liquidity. These actions would reduce risks from liquidity mismatches in open-end funds and make markets more robust in times of stress.

—This blog is based on Chapter 3 of the October 2022 Global Financial Stability Report, “Asset Price Fragility in Times of Stress: The Role of Open-End Investment Funds.”