Government support was vital to help people and firms survive pandemic lockdowns and support the economic recovery.

But where inflation is high and persistent, across-the-board fiscal support is not warranted. Most governments have already dialed back pandemic support, as noted in our October Fiscal Monitor.

With many people still struggling, governments should continue to prioritize helping the most vulnerable to cope with soaring food and energy bills and cover other costs—but governments should also avoid adding to aggregate demand that risks dialing up inflation. In many advanced and emerging economies, fiscal restraint can lower inflation while reducing debt.

Fiscal consolidation, limiting debt

Central banks are raising interest rates to dampen demand and contain inflation, which in many countries is at its highest levels since the 1980s. Because rapid price gains are costly to society and detrimental to stable economic growth, monetary policy must act decisively.

While monetary policy has the tools to subdue inflation, fiscal policy can put the economy on a sounder long-term footing through investment in infrastructure, health care, and education; fair distribution of incomes and opportunities through an equitable tax and transfer system; and provision of basic public services. The overall fiscal balance, however, affects the demand for goods and services, and inflationary pressures.

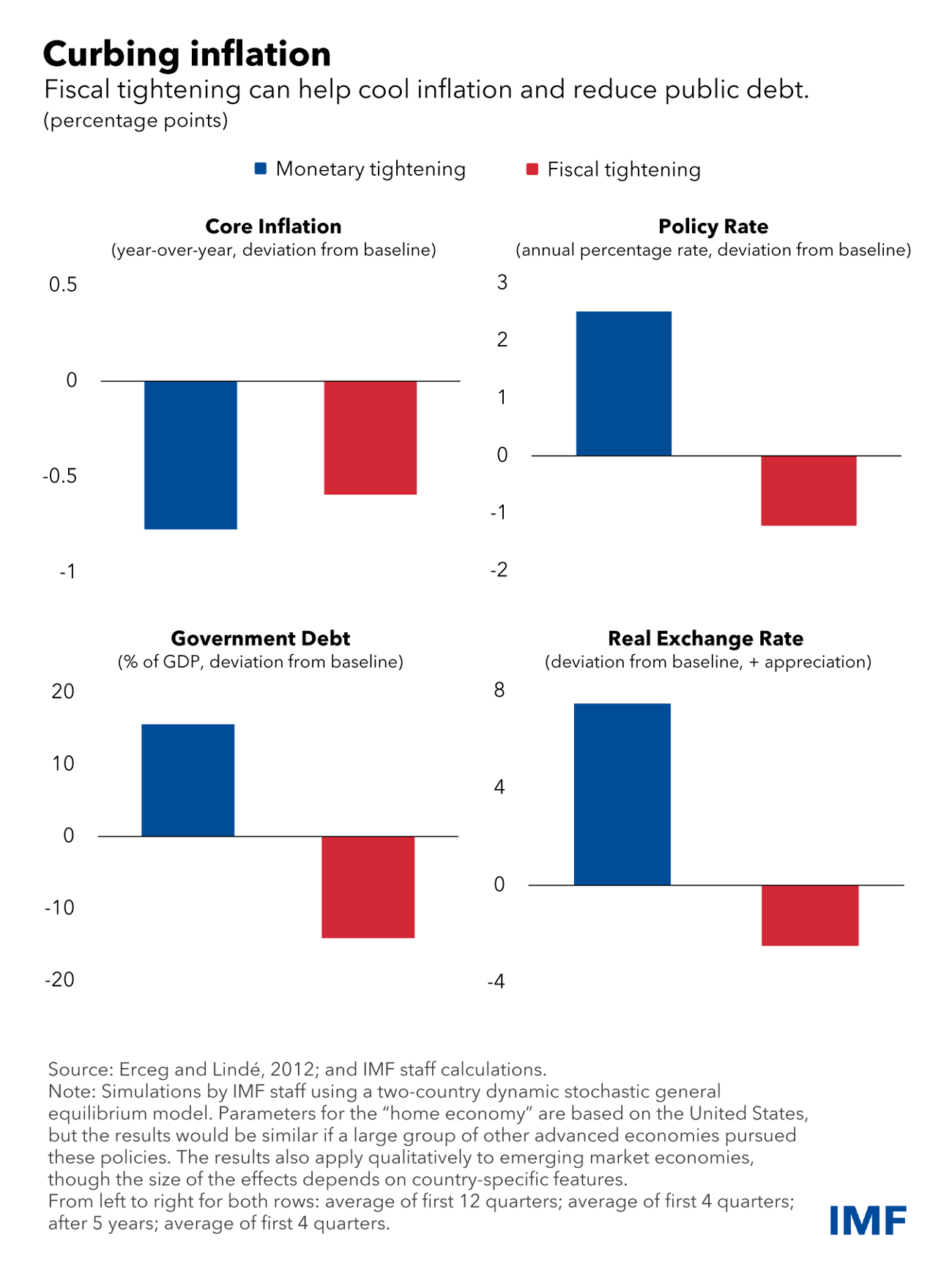

A smaller deficit cools aggregate demand and inflation, so the central bank doesn’t need to raise rates as much. Moreover, with global financial conditions constraining budgets, and public debt ratios above pre-pandemic levels, reducing deficits also addresses debt vulnerabilities.

Conversely, fiscal stimulus in the current high inflation environment would force central banks to slam on the brakes harder to curb inflation. Amid elevated public and private sector debt, this may raise risks for the financial system, as our Global Financial Stability Report described in October.

Demonstrating alignment

Against that backdrop, policymakers have a responsibility to provide strong protections to those in need, while paring back elsewhere or raising additional revenues to reduce the overall deficit. Fiscal responsibility—or even consolidation where needed—demonstrates that policymakers are aligned against inflation.

When fiscal adjustment is sustained, ideally through a medium-term fiscal framework that sketches the direction of policy over the next few years, it also addresses looming pressures on debt sustainability. These include aging populations in most advanced and several emerging economies, and the need to rebuild buffers that can be deployed in future crises or economic downturns.

In our research, we use a stylized two country model (where the “home economy” may be the US or a group of advanced economies). We study two different approaches to curb inflation. The first relies exclusively on monetary tightening to cool the overheating economy, whereas the second involves fiscal consolidation. Both are constructed to have similar effects on economic growth, and each is effective in reducing inflation. Under the first, higher interest rates and the weaker growth contribute to rising public debt. Meanwhile, the currency appreciates as higher yields attract investors.

Under the second approach, fiscal tightening cools demand without the need for interest rates to rise, so the real exchange rate depreciates. And with lower debt-service costs and smaller primary deficits, public debt declines. The real exchange-rate appreciation under tighter monetary policy implies that inflation falls a bit more, but this difference would diminish if more countries pursued these policies.

Faced with high food and energy prices, governments can improve their fiscal position by moving from broad-based support to assisting the most vulnerable—ideally, through targeted cash transfers. Because supply shocks are long-lasting, attempts to limit price increases through price controls, subsidies, or tax cuts will be costly to the budget and ultimately not be effective. Price signals are critical to promote energy conservation and encourage private investment in renewables.

The desirable fiscal stance and measures underpinning it will depend on country-specific circumstances, including current inflation rates and longer-term considerations such as debt levels and developmental needs. In most countries, higher inflation strengthens the case for fiscal restraint, calling for raising revenue or prioritizing spending that preserves social protection and growth-enhancing investments in human or physical capital.

International dimensions

In the United States, the early-1980s disinflation under Federal Reserve Chairman Paul Volcker exemplified the challenges of controlling inflation. Inflation had become entrenched at high levels, and fiscal policy was expansionary. The Fed had to raise rates sharply to rein in inflation, causing a collapse in housing investment and historically large appreciation of the dollar. Manufacturing was hard hit, leading to calls for trade protectionism.

That historical episode is relevant for many countries facing similar challenges today. A more balanced removal of policy stimulus, including fiscal restraint, can reduce the risk that some parts of the economy—especially those most sensitive to interest rates—experience disproportionate effects, or that large swings in the currency heighten trade tensions.

This would also reduce risk globally. Less abrupt interest rate hikes would imply a more gradual tightening of financial conditions and mitigate financial stability risks. This would tend to limit adverse spillovers to emerging market economies and reduce the risk of sovereign debt distress. Avoiding a sharp appreciation of the US dollar or other major currencies would also lessen pressures on emerging markets that borrow in those currencies.

While many central banks are tightening policy in response to the large and persistent rise in global inflation, the policy mix matters. Fiscal restraint will reduce the cost of bringing inflation back to target in a timely way, compared with the alternative of leaving monetary policy alone to act.