عربي, Español, Français, 日本語, Português,

When the Group of Twenty industrialized and emerging market economies (G-20) finance ministers and central bank governors last met in April, the world was in the midst of the Great Lockdown forced by the outbreak of COVID-19. As they meet virtually this week, many countries are gradually reopening, even as the pandemic remains with us. Clearly, we have entered a new phase of the crisis—one that will require further policy agility and action to secure a durable and shared recovery.

I believe that despite the pain and suffering that the pandemic has caused, we can aspire to transform our world.

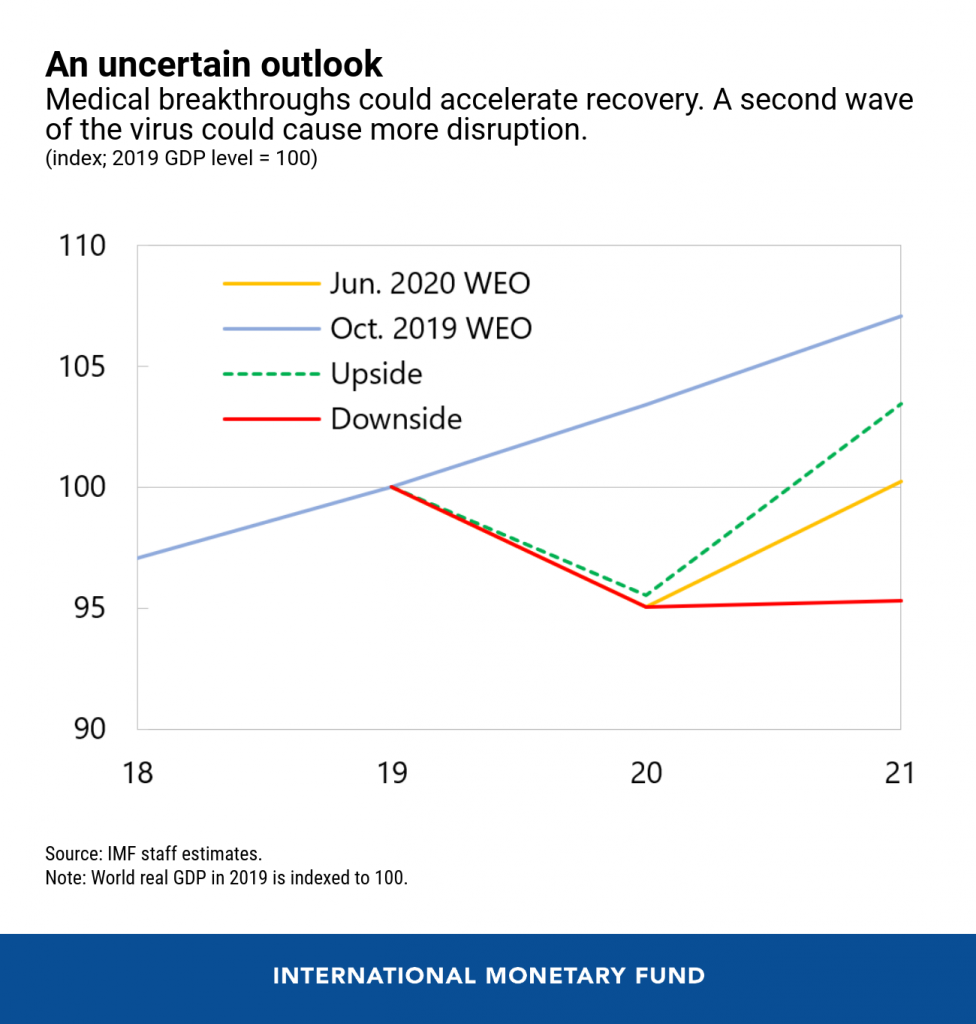

Last month, the IMF reported a worsened economic outlook and projected global growth to contract by 4.9 percent this year. Some better news is that global economic activity, which posted an unprecedented decline earlier this year, has started to gradually strengthen. A partial recovery is expected to continue in 2021. The exceptional action taken by many countries, including the G-20—through fiscal measures of about US$11 trillion and massive central bank liquidity injections—put a floor under the global economy. This extraordinary effort should not be underestimated.

But we are not out of the woods yet. A second major global wave of the disease could lead to further disruptions in economic activity. Other risks include stretched asset valuations, volatile commodity prices, rising protectionism, and political instability.

On the positive side, medical breakthroughs on vaccines and treatments could lift confidence and economic activity. These alternative scenarios highlight that uncertainty remains exceptionally high.

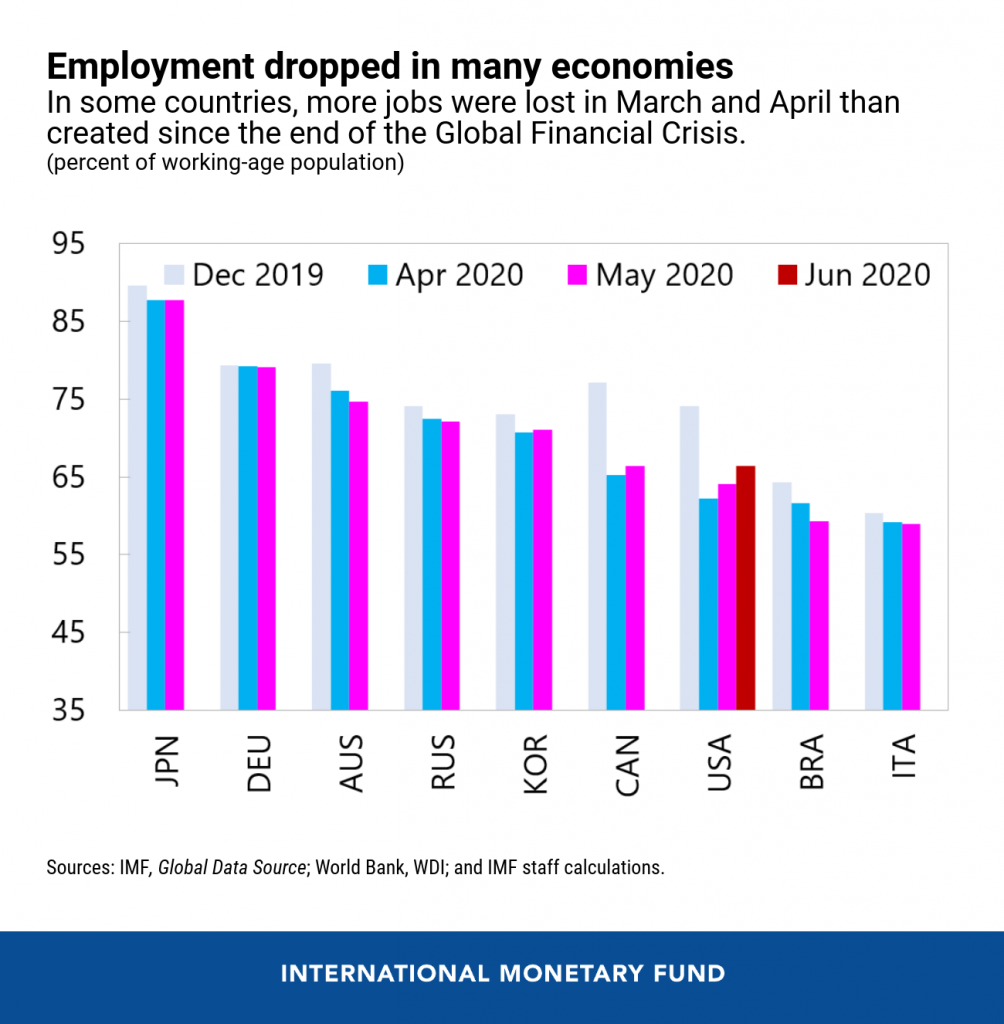

Many countries will be deeply affected by the economic scars of this crisis. Severe labor market dislocations are a major concern. In some countries, more jobs were lost in March and April than were created since the end of the global financial crisis. School closings also impacted people’s—in particular women’s—ability to participate in the labor market. Though fortunately some jobs have since been regained, the employed share of the working-age population stands much lower than in early 2020. Moreover, the full extent of the impact on the labor market is likely much higher as many employed people are facing reduced hours.

Bankruptcies also are becoming more common as firms exhaust their cash buffers.

And human capital is at risk: the education of over a billion learners across 162 countries has been disrupted, for example.

The bottom line is that the pandemic is likely to increase poverty and inequality, further painfully exposing weaknesses in health systems, the precariousness of work, and the challenging prospects for the young of accessing opportunities they desperately need.

For a more inclusive and resilient recovery, we need further action in two key spheres: (1) domestic policies and (2) collective efforts.

1. Domestic Policies: Sustaining Targeted Lifelines

Countries are at different stages of the pandemic, so their responses will differ as well. As the IMF has emphasized, emerging market and developing countries will be the hardest hit by this crisis—they face bigger challenges and steeper trade-offs than the advanced economies—and they will need more support for longer. That said, there are several domestic policy imperatives that apply broadly.

Protect People and Workers. Across the world, countries have ramped up economic lifelines to individuals and workers. These safety nets must be maintained as needed and, in some cases, expanded: from paid sick leave for low-income families, to access to health care and unemployment insurance, to broader cash and in-kind transfers for those in the informal sector—with digital mechanisms often best for delivery. Encouragingly, countries with higher inequality have devoted larger shares of support to households, including vulnerable groups.![]()

At the same time, many jobs lost will never come back with the crisis triggering long-lasting changes in spending patterns. So workers must continue to be supported, including through reskilling, to help them move away from shrinking sectors and toward expanding ones.

Support Firms. People and workers are also supported when lifelines are extended to viable businesses. Across the G-20, more firms have been supported through relief from taxes or social security contributions, grants, and interest rate subsidies. A significant portion was directed to small and medium enterprises (SMEs)—especially important since SMEs are a major engine of employment. Without such support, staff analysis suggests that SME bankruptcies could triple from an average of 4 percent before the pandemic to 12 percent in 2020, threatening to add to unemployment and harm bank balance sheets.

Increasing bankruptcies will leave governments with difficult choices on whether and how to support firms. Sound analysis of liquidity and solvency prospects of firms can help guide these choices. Liquidity provision might be enough for industries where revenue losses are temporary, for example, while equity injections may be needed for some insolvent firms that are essential for fighting the pandemic or on which many lives and livelihoods depend.

The fiscal costs of this support are substantial and rising debt levels are a serious concern. At this stage in the crisis, however, the costs of premature withdrawal are greater than continued support where it is needed. Of course, measures must be targeted and budgets assessed with an eye to cost-effectiveness—and to medium-term debt sustainability.

Preserve Financial Stability. Job losses, bankruptcies, and industry restructuring could pose significant challenges for the financial sector—including credit losses to financial institutions and investors. Regulation and supervision should support the flexible use of existing capital and liquidity buffers in line with international standards—which in turn would facilitate the continued provision of credit to viable businesses. Monetary policy should remain accommodative where output gaps are significant and inflation is below target, as is the case in many countries during this crisis.

An important domestic priority for policymakers is to ensure that money markets, foreign exchange markets, and securities markets can function effectively. Coordination across central banks and appropriate support from international financial institutions will also continue to be essential in that regard.

2. Collective Efforts: Capturing Opportunities for a Better Future

Indeed, international cooperation is vital to minimize the duration of the crisis and ensure a resilient recovery. Areas where collective action is key include:

-

Guaranteeing adequate health supplies: through cooperation on the production, purchase, and fair distribution of effective therapeutics and vaccines, including across borders.

-

Avoiding further ruptures in the global trade system: countries should do their best to keep global supply chains open, accelerate efforts to reform the World Trade Organization, and seek a comprehensive agreement on digital taxation.

-

Ensuring that developing countries can finance critical spending needs and meet debt sustainability challenges: continued progress on the G-20 Debt Service Suspension Initiative is especially important.

-

Strengthening the global financial safety net: including consideration of further extensions to swap lines and enhanced use of the IMF’s special drawing rights (SDRs).

The IMF, for its part, has responded to this crisis in an unprecedented way—including emergency financing for 72 countries in three months. With the support of our 189 member nations, we aim to do even more in this next critical phase.

We can take inspiration from the great Lebanese poet, Khalil Gibran, who once said: “To understand the heart and mind of a person, look not at what he has already achieved, but at what he aspires to.”

I believe that despite the pain and suffering that the pandemic has caused, we can aspire to transform our world. We have a once-in-a-century shot at building forward better: a world that is fairer and more equitable; greener and more sustainable; smarter and, above all, more resilient.

To seize this opportunity and achieve greater resilience, action is needed to: (1) invest in people—in education, health, social protection, and in preventing the sharp increase in inequality this crisis could produce; (2) support low-carbon and climate-resilient growth, including through smart allocation of public spending; and (3) take advantage of the digital transformation, whether through greater use of e-government platforms to enhance efficiency and transparency while cutting red tape, e-learning, or remote work.

G-20 policymakers—and all of us working together—must seize the opportunity to make this future a reality.