Twenty years ago, the IMF released its inaugural Global Financial Stability Report to strengthen surveillance of financial markets after a series of crises in emerging market economies and the dot-com bust.

This semiannual publication by the Monetary and Capital Markets Department has since evolved through years of seismic shifts in the global economic and financial landscape into one of our key multilateral surveillance tools. Along with the World Economic Outlook and the Fiscal Monitor, this flagship report aims to foster international monetary and financial stability.

The beginning

Monitoring the health and outlook of the global economy and member countries is the bedrock of the Fund’s work. This surveillance role, outlined in amendments to our Articles of Agreement first adopted at the 1944 Bretton Woods Conference, charges us with overseeing and safeguarding the international monetary system.

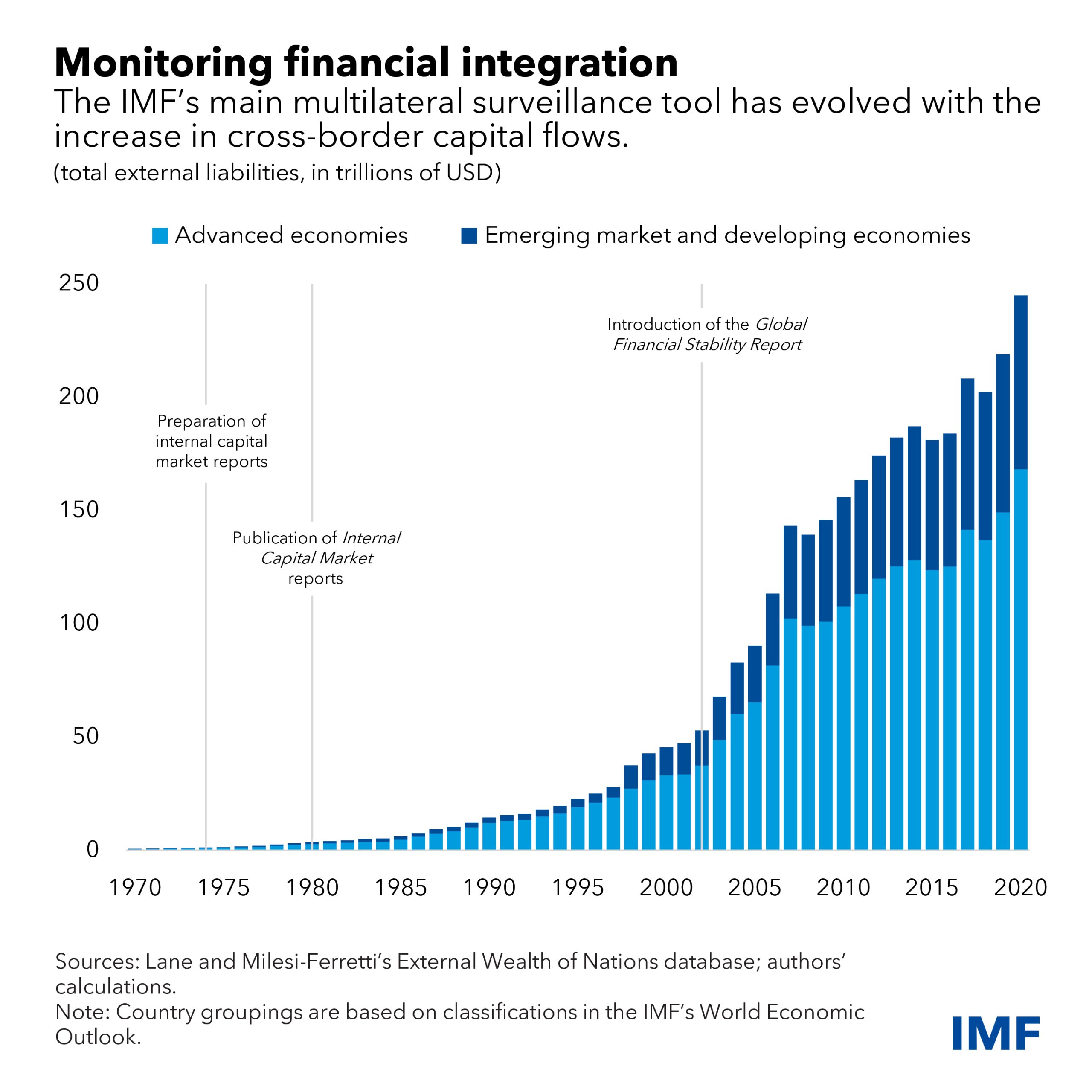

In the early years, surveillance focused on the macroeconomic and exchange-rate policies of member nations, but growth in international banking in the early 1970s highlighted a need to better track global capital markets and assess financial-stability implications. Consequently, the Fund started discussions with monetary authorities in major financial centers and in 1974 initiated internal reports on market developments and prospects.

Starting in 1980, the report known as International Capital Markets became our main vehicle to monitor conditions in financial markets, warn of risks, and analyze disruptions like Latin America’s debt crisis of the 1980s or Europe’s exchange-rate mechanism crisis in the early 1990s. But that era’s rapid expansion and integration of global capital markets, and the ensuing financial crises in Asia and several other emerging markets, highlighted the need to better assess systemic risks.

The introduction of the Global Financial Stability Report marked an important step toward a more comprehensive and frequent assessment of cross-border capital flows and financial market risks. In his forward to the first GFSR, the then-Managing Director Horst Köhler noted how the report had its roots in crisis.

“The rapid expansion of financial markets has underlined the importance of a constant evaluation of the private sector capital flows that are the engine of world economic growth, but sometimes at the core of crisis developments as well,” he wrote. “Opportunities offered by the international capital markets for enhancing global prosperity must be balanced by a commitment to prevent debilitating financial crises.”

Turning point

The GFSR has since focused on identifying cyclical and structural vulnerabilities in the bank and nonbank sectors of advanced and emerging market economies, the risks they pose, and the policy options to mitigate these risks.

Vulnerabilities such as leverage tend to build up when financial conditions are easy and investor risk appetite is strong. And in times like that, our stability reports place more emphasis on potential threats we see building.

One of the most pivotal moments for the GFSR arrived in 2007, when contagion from the US housing slump shook the world’s economies and markets. In a tightly integrated world, the global financial crisis underscored just how critical it is to better connect the dots between institutions, sectors, and countries.

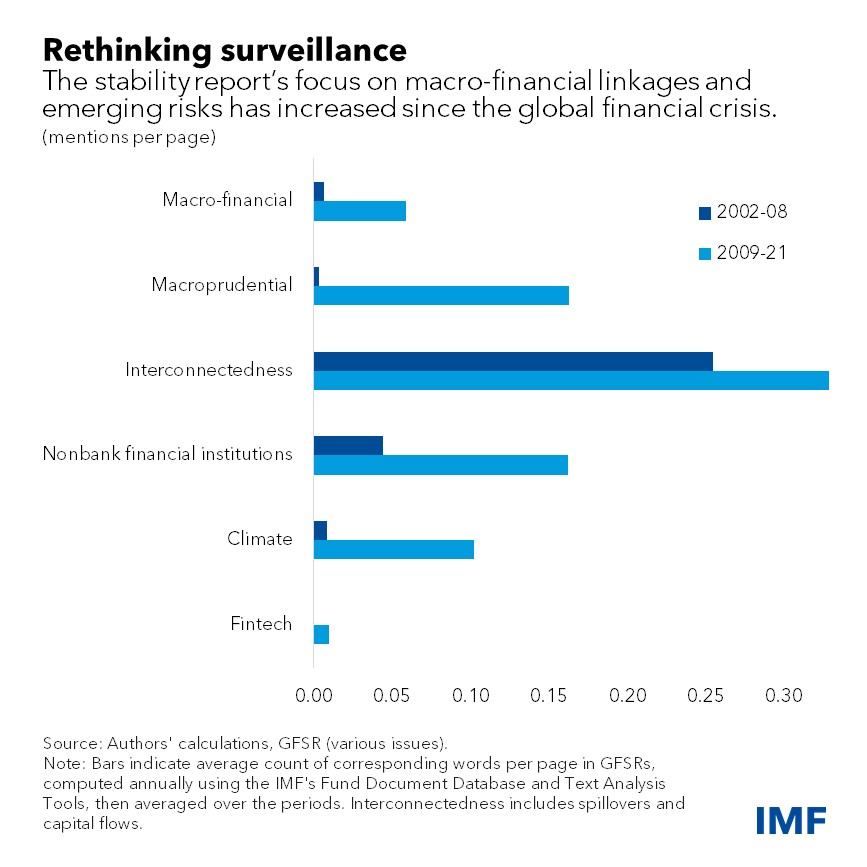

Since then, the Fund has increased its efforts to analyze and understand interlinkages and systemic risks, cross-border interconnectedness and spillovers, and the role of macroprudential policies in strengthening financial system resilience.

In recent years, we have adopted a conceptual framework for more systematic assessment and monitoring of financial stability risks. It centers around vulnerabilities that amplify negative shocks, creating an adverse feedback loop between falling asset prices and tightening financial conditions, deleveraging by financial firms, and weakening economic activity.

The empirical implementation of the framework relies on two tools: a broad set of key vulnerability indicators for the financial and real sectors (such as debt-servicing capacity and the ratio of liquid assets to short-term liabilities) that can serve as intermediate targets for macroprudential policies (such as capital buffers and liquidity coverage ratios); and an aggregate measure of how financial stability risks could affect expected global economic activity, which we call “growth at risk.”

These tools are complementary for monitoring and policymaking purposes, as a granular analysis of specific exposures provides the necessary nuance and depth to the summary measure of threats to economic growth.

The GFSR has also actively called for an overhaul of the international regulatory landscape to address the gaps revealed by the global financial crisis. In addition, it has backed strengthening oversight of nonbank financial institutions, which have taken on a bigger role in intermediation since the crisis and could make the system more vulnerable.

Constant vigilance

Though we have made progress, the continuous evolution in global financial markets—not least because of the dizzying pace of technological innovation—is always introducing new vulnerabilities and risks that demand constant vigilance. For instance, the advent of fast and highly sophisticated computer technology has facilitated the growth of high-frequency trading, which can improve market efficiency but can also be a source of market instability.

Other emerging technologies such as artificial intelligence and distributed ledger are revolutionizing financial markets through fintech and crypto assets that carry opportunities but also fundamental risks that the GFSR is bringing to the fore. Climate change poses another stability threat that we are increasingly analyzing, along with the role that sustainable finance and the private sector can play in fostering a green transition.

And now, as our recent reports have highlighted, the enduring pandemic and war in Ukraine have further compounded financial risks by exacerbating pre-existing fragilities, contributing to the greatest inflationary pressures in decades, and confronting international capital markets with greater risk of fragmentation.

More than ever, rapid technological change as well as frequent and varied shocks make our surveillance crucial for safeguarding international monetary and financial stability in order to promote growth and inclusion. And it’s increasingly clear that, to do so, we must constantly adapt and sharpen our tools for assessing risk to better scan the global financial landscape and strengthen its resilience.