As Latin American countries continue to grapple with the effects of two previous shocks, the pandemic and Russia’s invasion of Ukraine, they face a third shock: the tightening of global financial conditions.

Growth momentum is currently positive, reflecting the return of service sectors and employment to pre-pandemic levels, and the overall support of favorable external conditions—high commodity prices, strong external demand and remittances , and rebounding tourism. This has led to several upward revisions to growth this year.

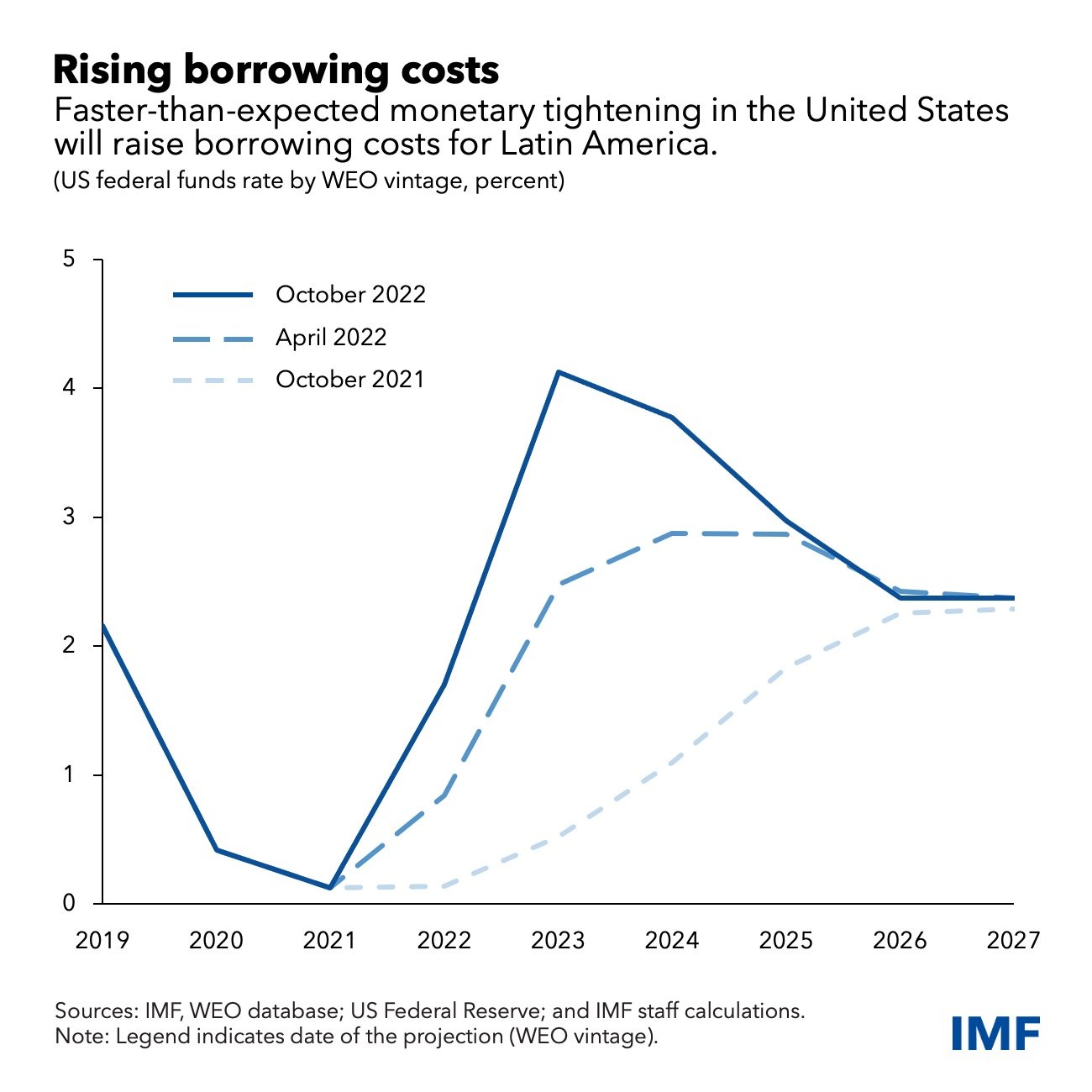

But financing is becoming scarcer and costlier as major central banks raise interest rates to tame inflation. Capital inflows to emerging markets are slowing and external borrowing costs are increasing. Domestic interest rates in emerging markets are also rising as their central banks are hiking rates to battle inflation as well, but also because of reduced investors’ appetite for risker assets.

For Latin America, these factors result in a deceleration in activity as higher borrowing costs weight on domestic credit, private consumption, and investment.

Earlier this year, surging commodity prices and solid growth momentum helped offset the effects of tighter global financial conditions, as investors were attracted by a region that hosts major commodity exporters amid global needs for food and energy supplies. But higher interest rates are pushing commodity prices down as the global economy decelerates, reducing their cushioning effect. The slowdown may also reduce exports, remittances, and tourism to the region.

Uncertainty about global interest rates and whether inflation can be

brought back under control smoothly—a so called ‘soft landing’—means spikes

in volatility and investor risk aversion are also possible. In other words,

the transition to higher global interest rates may be bumpy.

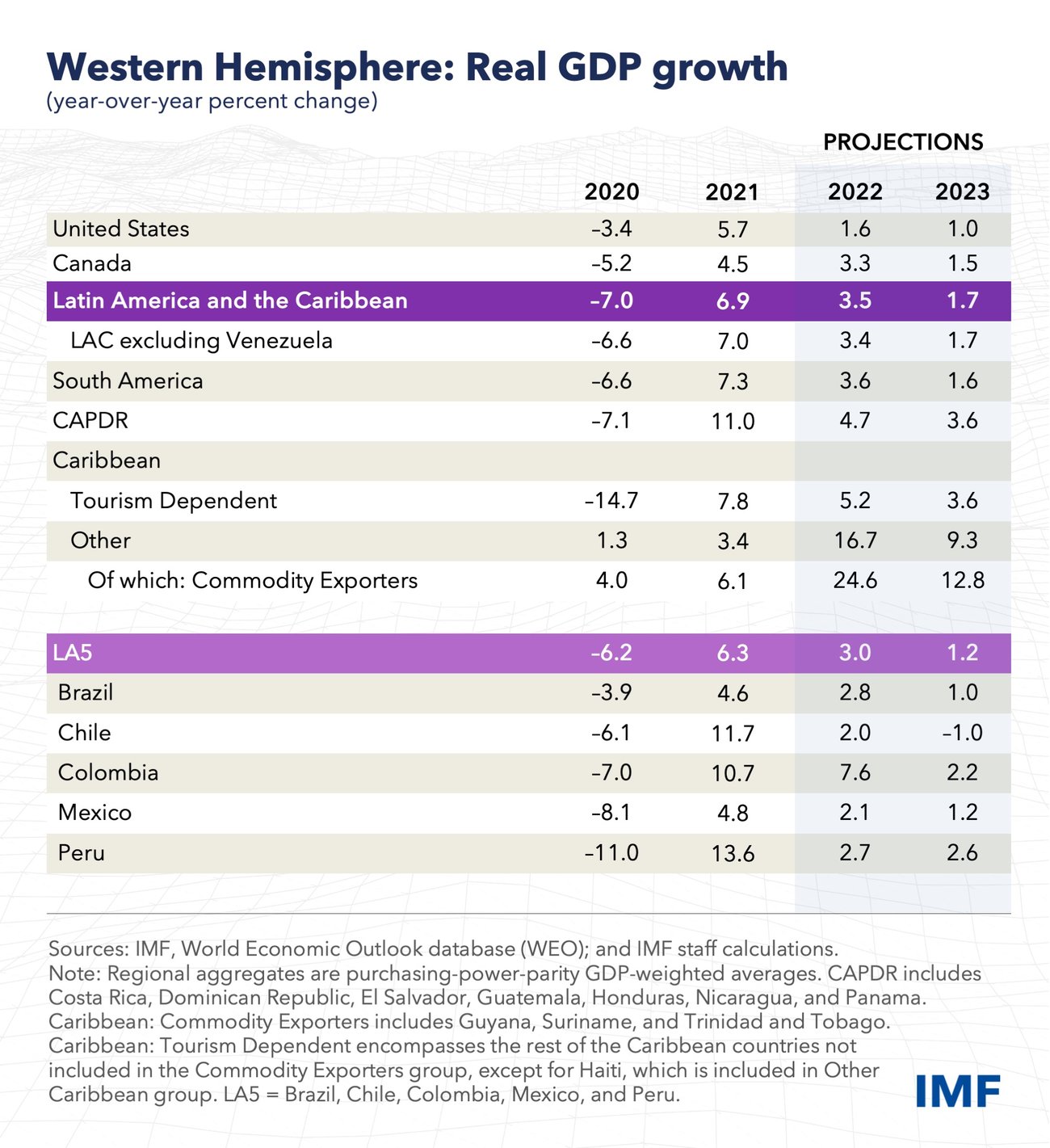

Solid growth but deceleration

Amid positive surprises in activity, we have upgraded our growth projection for Latin America and the Caribbean this year to 3.5 percent from 3 percent in July.

But with the changing winds ahead, growth next year is poised to decelerate more rapidly than we projected in July, slowing to 1.7 percent.

Commodity exporters—South American countries, Mexico and some Caribbean economies—are likely to see their growth rates halved next year, as lower commodity prices amplify the impact of rising interest rates.

The economies of Central America, Panama and the Dominican Republic will also slow as trade with the United States and incoming remittances weaken, though they will benefit from lower commodity prices. Tourism-dependent Caribbean economies will continue recovering, albeit slower-than-anticipated in July amid weaker tourism prospects.

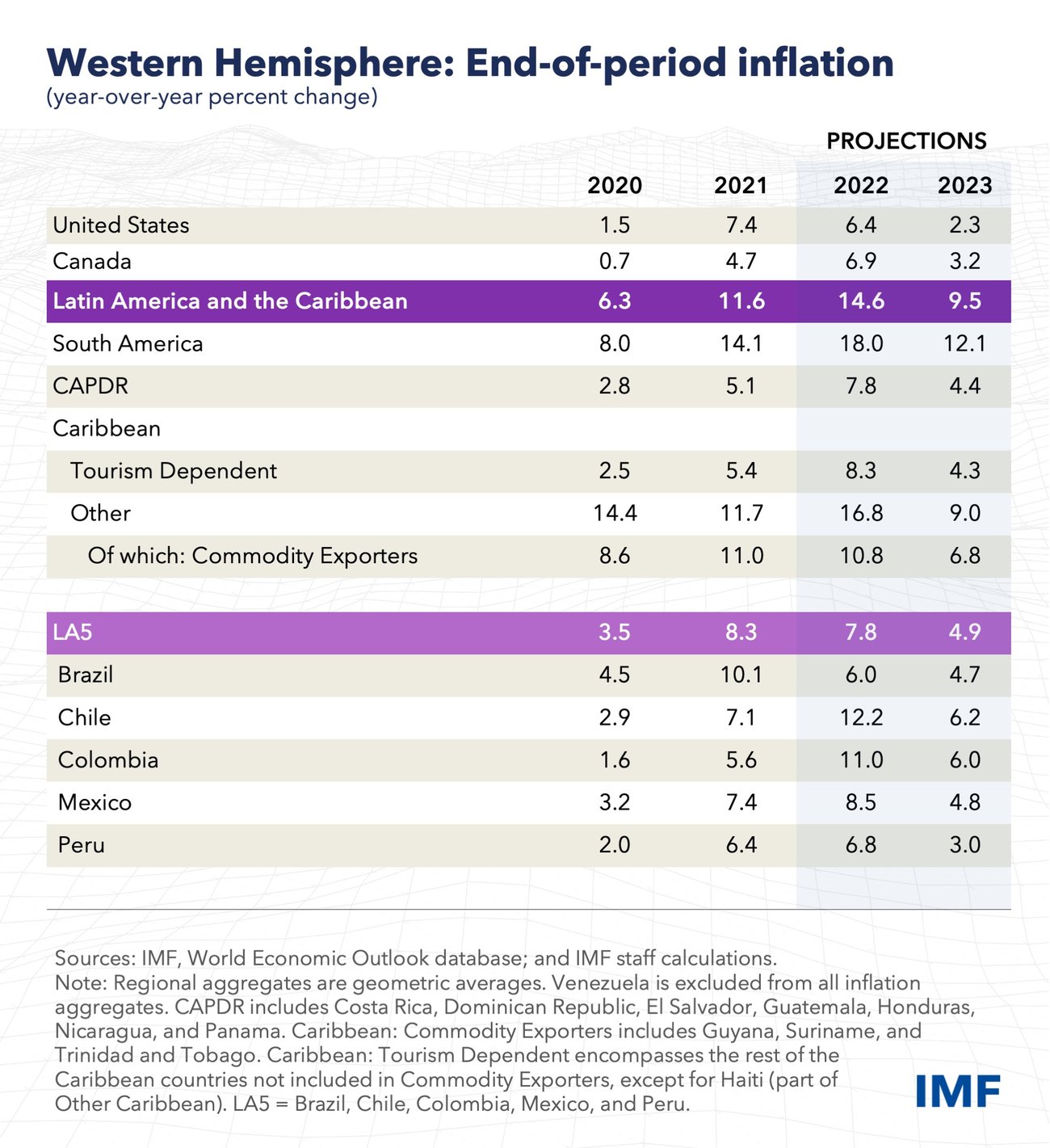

Fighting stubborn inflation

Despite slowing growth, Latin America will continue facing high inflation for some time.

The swift response of major central banks in the region, which hiked interest rates ahead of other emerging market and advanced economies, will help bring down inflation, but this will take time as monetary policy needs to tame domestic demand to exert downward pressure on prices.

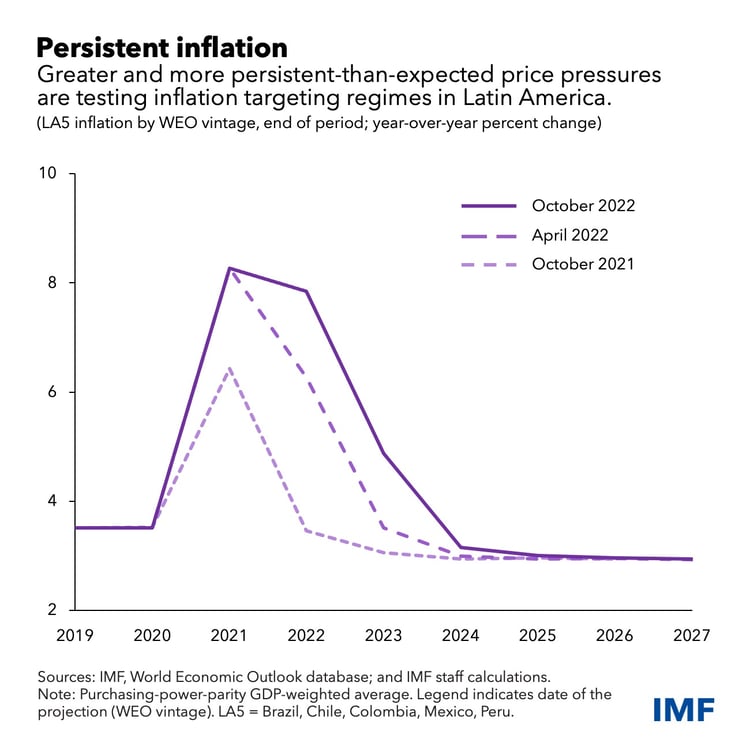

Also, price pressures have recently broadened, affecting items of the consumption baskets beyond food and energy. This has been the case in Brazil, Chile, Colombia, Mexico and Peru, where inflation recently reached a two-decade high of 10 percent and is testing the hard-won credibility of inflation targeting frameworks.

We have, therefore, raised our inflation forecasts. Price increases for those five countries will reach around 7.8 percent by year-end and remain elevated at about 4.9 percent—still above central banks’ tolerance bands in most cases—by the end of next year.

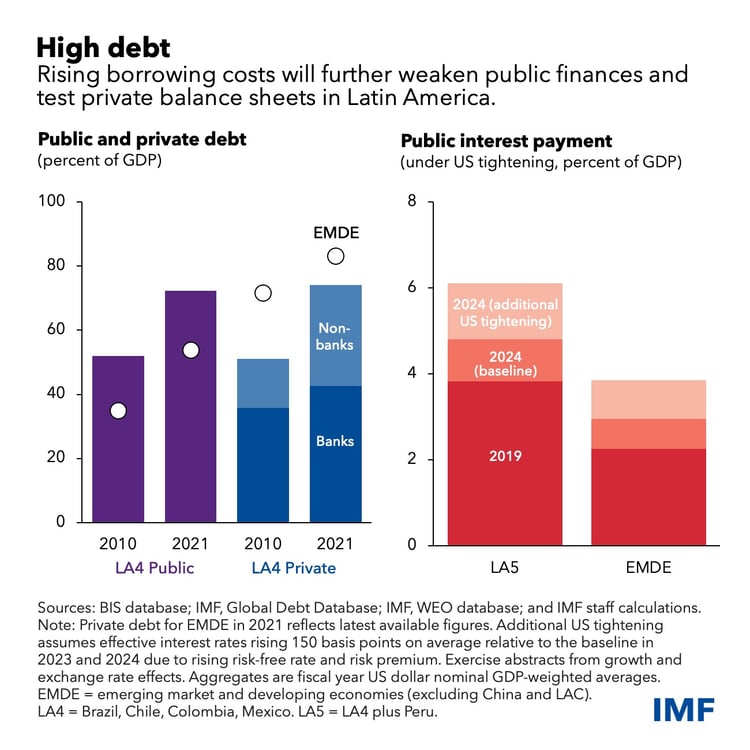

Healthy banks, debt risks

Rising global interest rates will also test the resilience of private and public balance sheets. The region’s generally healthy banking systems mitigate the risk of financial distress, and regulation and supervision have improved in many countries.

But pockets of vulnerabilities remain. For example, corporate debt has grown considerably over the last decade, especially outside the banking system. Monitoring these vulnerabilities will be key to identify potential sources of stress and take early action.

While the region’s high levels of international reserves and strong central

bank credibility will help mitigate the impact of tighter financial

conditions, rising borrowing costs will test public finances through higher

interest payments, as public debt and financing needs remain elevated.

Balancing act

Central banks in the region have acted fast and kept long-term inflation expectations anchored.

Going forward, monetary policy should stay the course and not ease prematurely. Setting monetary policy amid high uncertainty is challenging, but having to restore price stability later if inflation becomes entrenched would be very costly.

Fiscal policy should focus on rebuilding policy space, where needed. This will require reining in public spending, improving the design of the tax systems, and strengthening fiscal frameworks to secure sustained discipline.

With dire social needs in the region, however, policies to reduce debt and deficits can only be effective and durable if they are inclusive—that is, if they protect the poor.

Even where fiscal space exists, fiscal policy should also go hand in hand with monetary policy, focusing on supporting vulnerable groups, especially while high inflation persists and growth weakens, but without fueling domestic demand. This will require careful calibration to offset spending measures to protect the poor.

Getting this balancing act right is key to achieving inclusive and sustainable growth, and this is the best way to build resilience against future shocks.