Credit IMF Photo/Johis Alarcón

Credit IMF Photo/Johis Alarcón

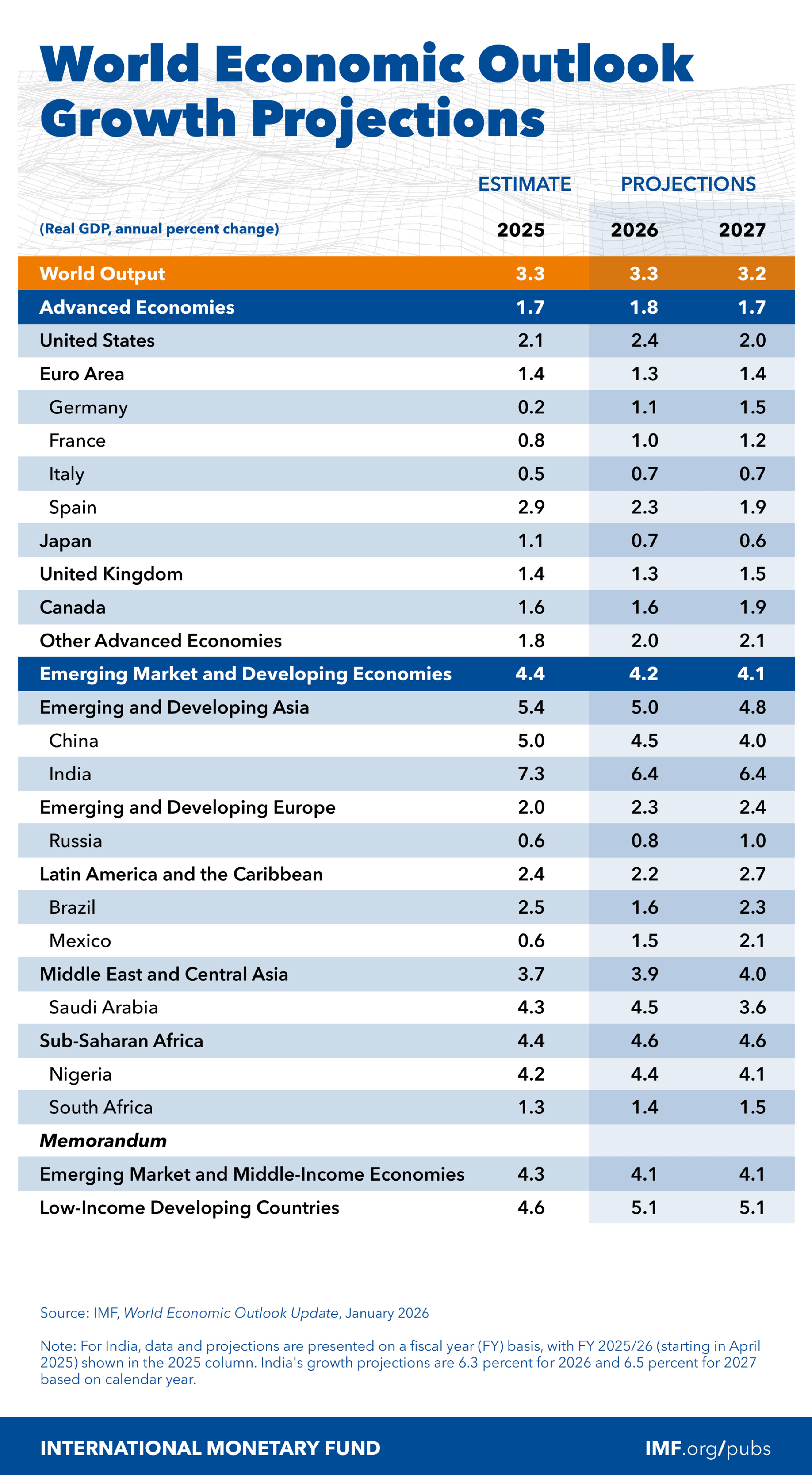

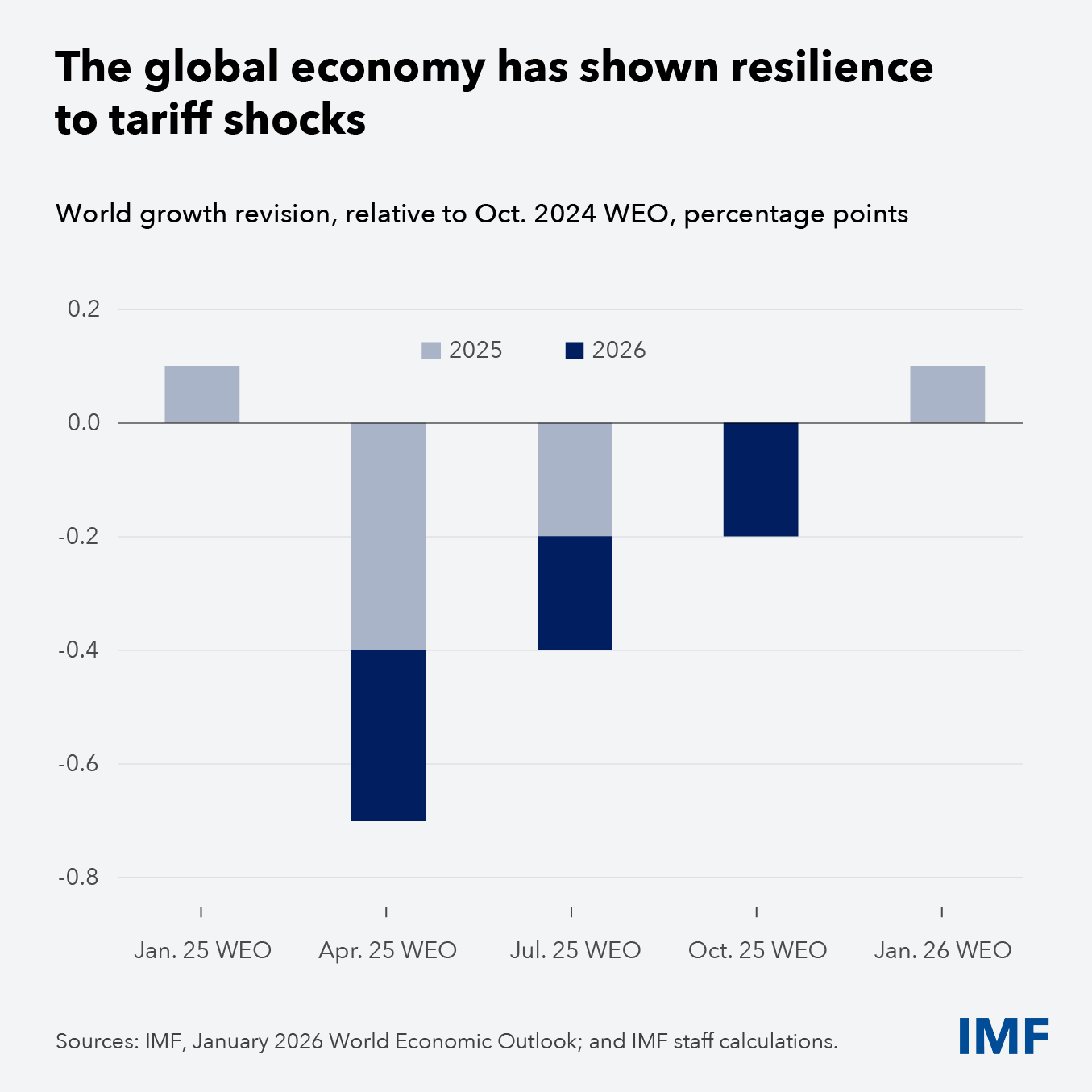

Global economic growth continues to show notable resilience despite significant US-led trade disruptions and heightened uncertainty. Our latest projections indicate that global growth will hold steady at 3.3 percent this year, an upward revision of 0.2 percentage points compared to October estimates, with most of the improvement accounted for by the United States and China. Remarkably, current projections are broadly unchanged from a year earlier, as the global economy shakes off the immediate impact of the tariff shock.

This surprising strength reflects a confluence of factors, including easing trade tensions, higher-than-expected fiscal stimulus, accommodative financial conditions, the agility of the private sector in mitigating trade disruptions and improved policy frameworks especially in emerging market economies.

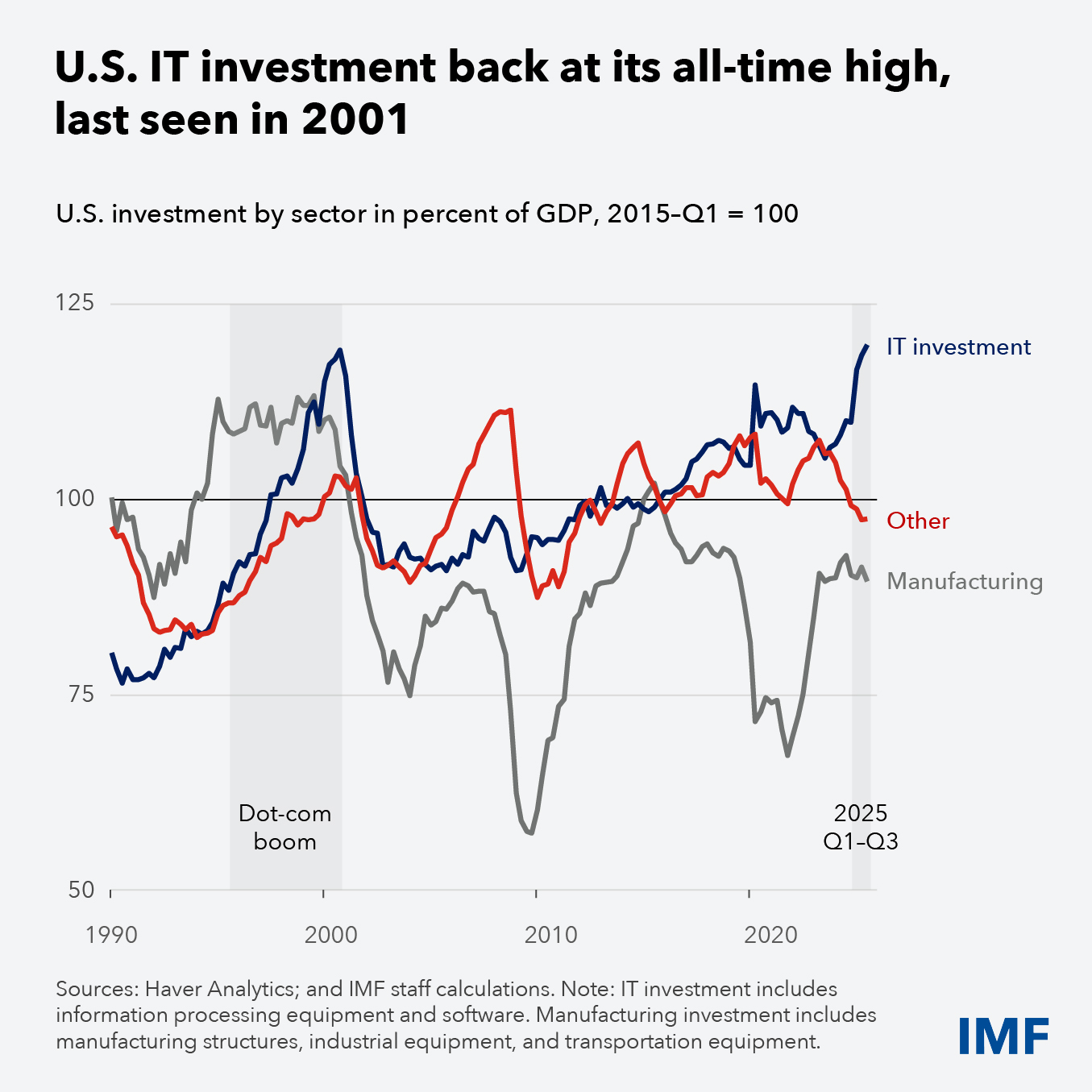

Another key driver of this resilience is the continued surge in investment in the information technology sector—especially in artificial intelligence. While manufacturing activity remains subdued, IT investment as a share of US economic output has surged to the highest level since 2001, providing a major boost to overall business investment and activity. Although this IT surge has been concentrated in the United States, it is also generating positive spillovers globally, most notably to Asia’s technology exports.

Financial conditions fuel expansion

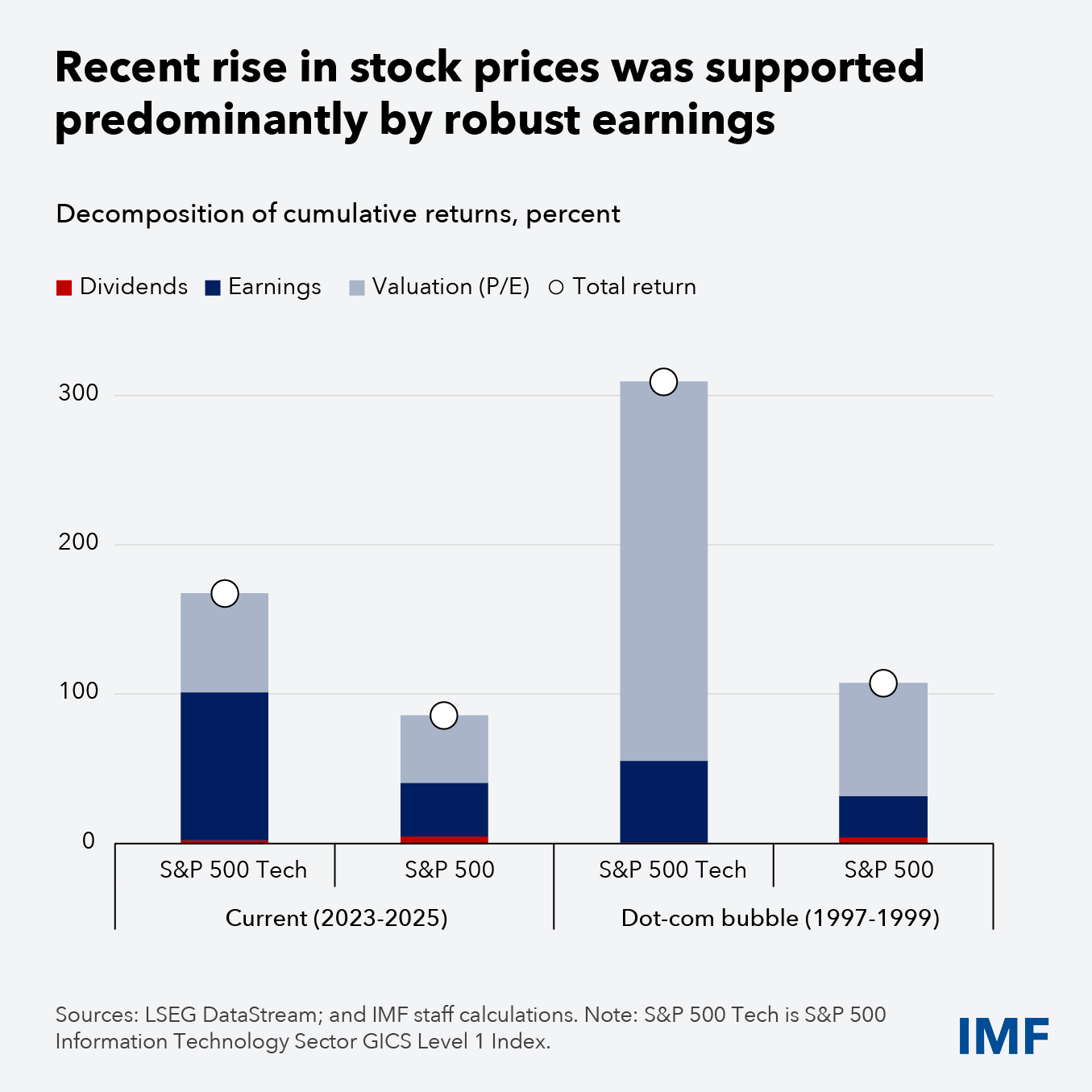

The IT investment boom reflects businesses and markets’ optimism about the transformative potential of recent tech innovations—in automation and AI—to deliver sizable productivity gains and to lift profits. Since late 2022, coinciding with the introduction of the first widely used generative-AI tools, stock prices have risen sharply.

Favorable financial conditions and robust earnings have supported rising stock prices and helped fund new capital spending. But as the expansion accelerates, debt financing is becoming more prevalent, increasing leverage. This shift introduces notable risks: higher leverage could amplify shocks if returns fail to materialize, or if broader financial conditions tighten, adversely impacting firms and raising concerns about spillovers to the broader financial system.

Moreover, profitability could become sensitive to assumptions around depreciation schedules for advanced processors. Frequent equipment upgrades will squeeze profit margins, weigh on earnings, and require significant additional debt financing. These factors underscore the importance of monitoring leverage accumulation and its potential to amplify vulnerabilities.

Lessons from the dot-com era

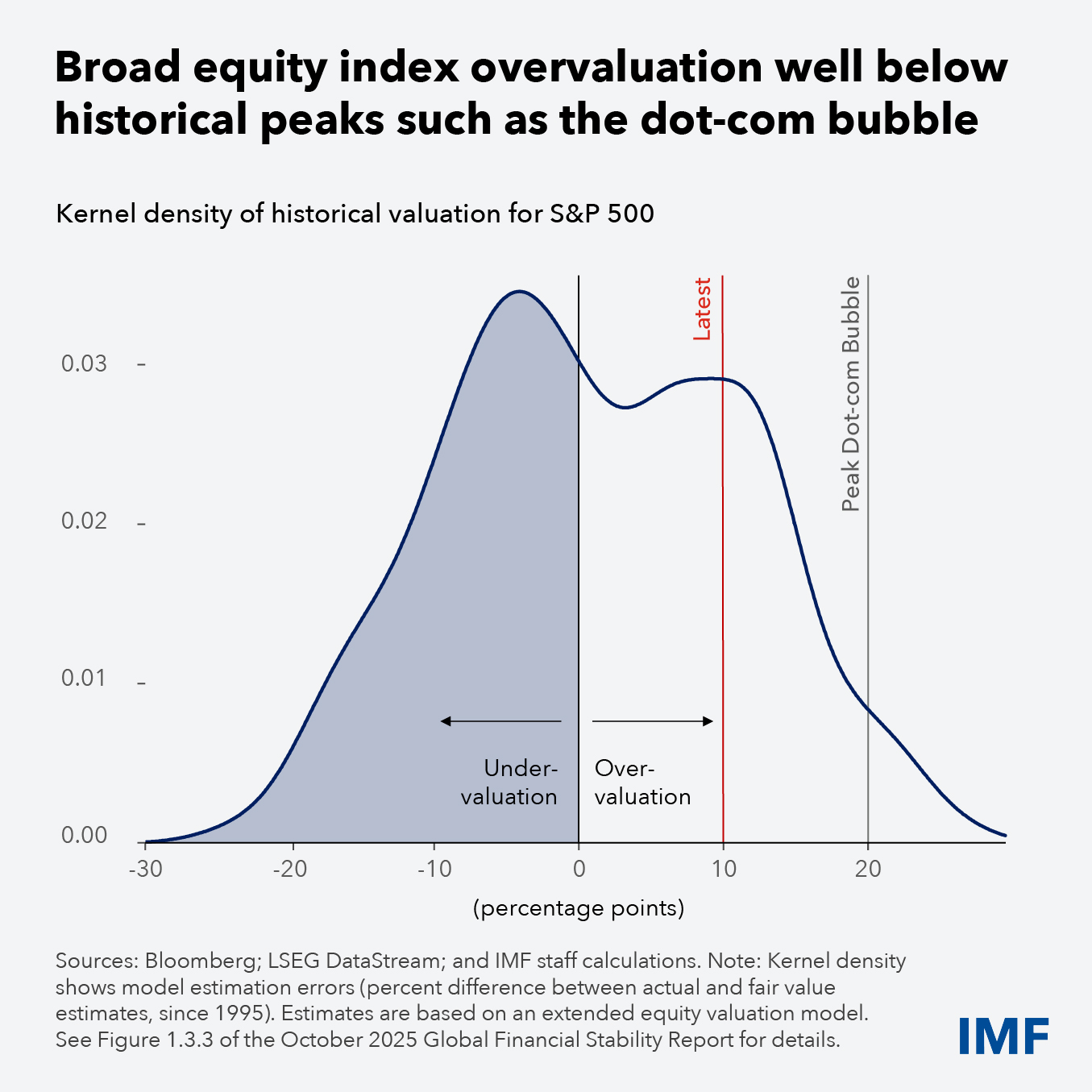

The comparison with the dot-com boom of 1995-2000 is instructive. Even though IT investment as a share of gross domestic product is broadly similar to levels then, the recent rise has been more gradual, accelerating markedly only last year. Furthermore, while market valuations relative to economic output have expanded at a similar pace in both episodes, the rise in price-earnings ratios has been more modest in the current boom given more robust earnings.

Overall, our analysis suggests that potential overvaluation for the broad equity index in the United States is only about half that of the dot-com episode. That said, the overall vulnerability of global macroeconomic growth to a repricing of technology stocks may be substantial for three reasons.

First, rising stock prices over the past few years have been driven predominantly by the technology sector, in particular AI-related stocks, and this narrow group has become a major driver of the index. Second, many critical AI-related firms are not currently listed on stock markets. Their debt borrowings could have consequences that were not seen during the dot-com era. Third, market capitalization is now much higher relative to output, from 132 percent in 2001 to 226 percent now for the United States; so even a more modest correction could have a sizable effect on overall consumption.

Risks to the outlook

Looking ahead, the current tech boom raises important upside and downside risks for the global economy. On the upside, AI could start to deliver on its productivity promises, raising US and global activity by 0.3 percent this year, relative to the baseline.

On the downside, AI firms could fail to deliver earnings commensurate with their lofty valuations, and investor sentiment could sour. For reference, a scenario in our October 2025 World Economic Outlook—which included a moderate correction in AI stock valuations with a tightening of financial conditions—reduces global growth by 0.4 percent relative to the baseline. This could have far-reaching consequences if real investment in technology sectors declines more sharply, triggering a costly reallocation of capital and labor. Combined with lower-than-expected total factor productivity gains, and a more significant correction in equity markets, global output losses could increase further, concentrated in tech-heavy regions such as the United States and Asia.

Given the decade-long increase in foreign ownership of US equities, this sharp correction could also trigger sizable wealth losses outside the United States and exert a drag on consumption, spreading the downturn more globally. Even economies that have little exposure to technology, including many high-debt and low-income countries, would be buffeted by negative external demand spillovers and higher external borrowing costs.

Such downside risks arise at a time of heightened geopolitical uncertainty, increased use of export controls on critical inputs and trade-related restraints, and eroded fiscal space in many countries. This could interact with any reassessment of AI-related productivity growth and repricing of risky asset valuations in a self-reinforcing manner.

Policy for stability, discipline, inclusion

With asset valuations stretched, debt financing on the rise, and uncertainty elevated, strong prudential oversight is essential to safeguard financial stability. Supervision and regulation should ensure robust underwriting standards by banks and nonbanks especially those exposed to the technology sector. Internationally agreed standards on bank capital and liquidity should be adhered to. Policymakers must be ready to deploy contingency plans for diverse risks.

Monetary policy faces a delicate balancing act. If the tech boom continues, it may push real neutral interest rates higher—as occurred during the dot-com era—calling for a monetary policy tightening. This would contract fiscal space, especially in countries that do not get a growth boost from AI.

Should the downside scenario materialize, the rapid decline in aggregate demand will call for a speedy reduction in policy rates.

Proper diagnosis and calibration of the monetary policy to achieve price stability requires that central banks operate within their mandate. Central bank independence remains paramount for monetary and financial stability and economic growth, protecting the credibility of monetary policy and anchoring inflation expectations.

On the fiscal side, governments should renew efforts to reduce public debt and restore fiscal space where needed.

AI’s uneven impact on workers is another important consideration. While innovation drives growth, it risks displacing jobs and depressing wages for certain segments of the workforce. Policies should focus on lowering barriers to adoption, helping workers to invest in the right skills, supporting job mobility through targeted programs, and maintaining competitive markets to facilitate entry and ensure that innovation benefits are broadly shared.

Balancing act

Global growth has been impressively resilient amid trade disruptions, but this masks underlying fragilities tied to the concentration of investment in the tech sector. And the negative growth effects of trade disruptions are likely to build up over time.

AI-driven investment offers transformative potential—but also introduces financial and structural risks that demand vigilance. The challenge for policymakers and investors alike is to balance optimism with prudence, ensuring that today’s tech surge translates into sustainable, inclusive growth rather than another boom-bust cycle. This is especially relevant in an environment marked by intensifying geopolitical strains and growing threats to institutional frameworks which make the implementation of good policies more challenging.