Credit (Photo: IMF Photo/Ryan-Rayburn)

Credit (Photo: IMF Photo/Ryan-Rayburn)

The war in Ukraine and related sanctions have triggered a sharp increase in commodity prices, which will add to the challenges facing countries in the Middle East and North Africa—particularly the region’s oil importers.

After leaping to a peak of $130 per barrel following Russia’s invasion, oil prices are expected to settle at an annual average of around $107 in 2022, up $38 from 2021, according to the IMF’s latest World Economic Outlook. Similarly, food prices are expected to increase by an additional 14 percent in 2022, after reaching historical highs in 2021.

This surge in prices comes at a precarious time for the region’s recovery. In our Regional Economic Outlook, we revised up our forecast for growth in the Middle East and North Africa as a whole by 0.9 percentage points to 5 percent, but this reflects improved prospects for oil exporters helped by rising oil and gas prices.

For oil-importing countries, we marked down our projections, as higher commodity prices add to the challenges stemming from elevated inflation and debt, tightening global financial conditions, uneven vaccination progress, and underlying fragilities and conflict in some countries.

The effect of high commodity prices

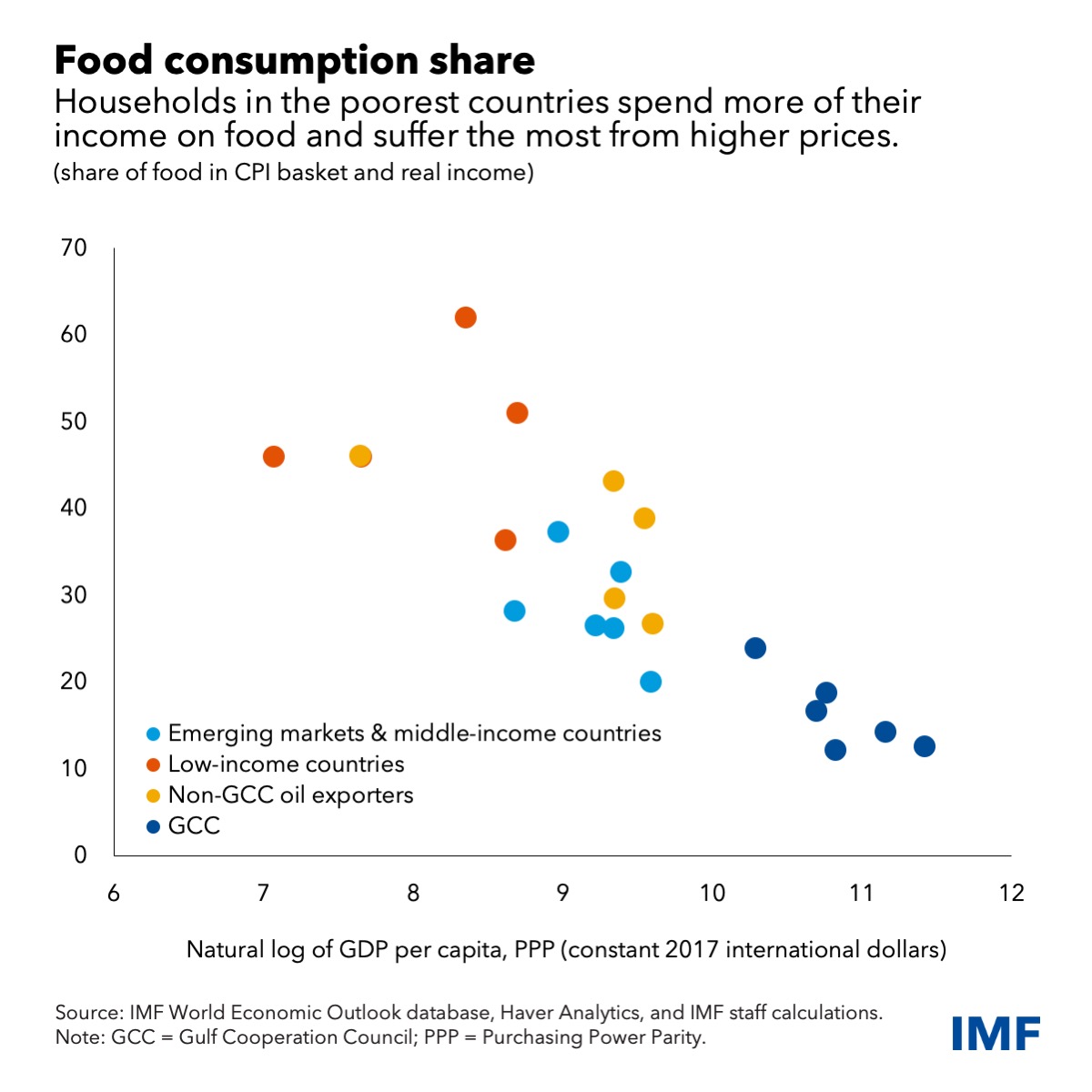

Higher inflation is one of the most direct impacts of rising commodity prices. Food prices accounted for about 60 percent of last year’s increase in headline inflation in the Middle East and North Africa, excluding the countries of the Gulf Cooperation Council. Hence, we project inflation to remain elevated in the region in 2022 at 13.9 percent—a significant upward revision relative to our previous projections in October.

This is no surprise given the high dependence of many economies in the region on shipments of foreign food (about one-fifth of total imports), and the heavy weighting of food in consumption baskets (more than one-third on average) and even higher in the case of low-income countries.

The war has also heightened concerns about food insecurity, given the region’s dependence on wheat imports from Russia and Ukraine and the rise in prices, which makes it harder for people to afford food.

The situation is particularly concerning for fragile and conflict-affected states, since strategic reserves cover less than 2.5 months of net domestic consumption. Overall, rising food prices and potential wheat shortages affect the poor more because they allocate a higher share of their expenditure to food. This will add to poverty and inequality and heighten the risk of social unrest.

Commodity price increases will also have a significant negative impact on oil importers’ external accounts. We project that these countries’ current account balances will deteriorate by 1 percentage point of GDP, on average. For low-income countries, higher wheat prices alone will be a significant blow, worsening current accounts by around 1.2 percent of GDP on average.

How are countries responding? Some are using targeted measures to ease the burden on their people, while others have resorted to more subsidies and price controls to limit the inflationary effects of higher international prices—but this will worsen fiscal balances in the absence of offsetting measures.

Energy subsidies alone could increase by up to $22 billion for oil-importing countries in 2022. This represents money that could otherwise have been spent on more targeted support or other priority measures. In addition to existing subsidies, some countries have introduced measures to smooth the impact of higher prices, such as direct transfers and lower tariffs on food, which will add to fiscal costs.

What should policymakers do?

Near-term policy trade-offs have become increasingly complex for oil-importing countries in the Middle East and North Africa. Containing inflation is a key priority, despite fragile recoveries. In countries where there are risks of inflation expectations rising or price pressures broadening, policy rates need to increase. Clear and transparent communication will be critical to guide markets.

It is also urgent that countries address food security risks and mitigate the impact of high international prices on the poor. The most effective way is to ensure vulnerable households are protected with targeted, temporary, and transparent transfers. Where safety nets are less strong, prices could be raised gradually. For low-income countries, sustained financial support from the international community is crucial.

For countries with high debt, these measures should be accompanied by offsetting measures elsewhere—for example, cutting unnecessary spending, promoting additional tax equity, or a combination of the two—to safeguard debt sustainability given limited fiscal space.

Coordinating fiscal and monetary policies and anchoring them in credible medium-term policy frameworks will help ease these trade-offs.

These challenges underscore the importance of pressing ahead with structural reforms, which will help countries weather future macroeconomic shocks and accelerate recovery. Measures that bolster the efficiency of government expenditure and revenue collection, including through digitalization, promote private sector activity, and strengthen social safety nets will all be important priorities.

As countries throughout the Middle East and North Africa work to adapt their macroeconomic policies to new geopolitical realities, the IMF will continue to help through policy advice, financing, and capacity development.