Latin America: When Is Fiscal Stimulus Right?

Finance & Development, June 2009, Volume 46, Number 2

Nicolás Eyzaguirre, Benedict Clements, and Jorge Canales-Kriljenko

For some countries stimulus is appropriate during the global economic crisis. But for others the answer is less clear

The role of fiscal policy in ameliorating the adverse effects of the global economic downturn is at the center of the policy debate in Latin America, as it is in other parts of the globe. Economic growth in the region is projected to decline from a healthy 4 percent in 2008 into negative territory in 2009, reversing some of the impressive gains in employment and poverty reduction of recent years. Fiscal, or government, revenues are also coming under pressure, making it difficult for countries to achieve targets for budget deficits, even without new spending initiatives. At the same time, many countries are constrained by limited access to financing and still-high levels of public debt, making it difficult to expand public borrowing. In these circumstances, how do policymakers assess whether or not a fiscal stimulus is appropriate? Under what conditions are markets likely to permit this kind of fiscal expansion to be effective in helping support living standards during a period of economic downturn?

Fiscal effects of the downturn

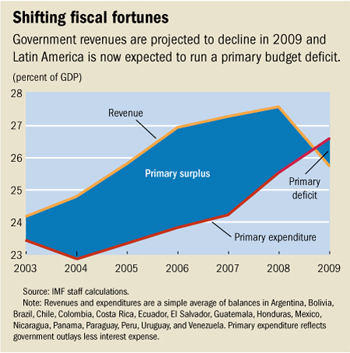

The contraction in economic activity and falling commodity prices are placing substantial pressure on government revenue. After several years of increases, revenue-to-GDP ratios for Latin American countries, on average, are  projected to fall by about 2 percentage points of GDP in 2009 (see chart). The revenue declines among commodity producers are especially noteworthy. Fiscal revenues are likely to drop significantly below their estimated long-run levels, and a key issue is whether it is desirable and feasible to protect public spending from falling as well.

projected to fall by about 2 percentage points of GDP in 2009 (see chart). The revenue declines among commodity producers are especially noteworthy. Fiscal revenues are likely to drop significantly below their estimated long-run levels, and a key issue is whether it is desirable and feasible to protect public spending from falling as well.

In deciding on the appropriate fiscal stance, an important consideration for policymakers is the effect of the budget deficit on financing conditions and interest rates. An increase in the government's budget deficit raises the demand for funds and public debt levels, and under some circumstances may raise interest rates substantially.

In emerging markets in Latin America, the effects of higher budget deficits on interest rates are potentially much stronger than in advanced economies. Many governments have yet to establish credible medium-term, typically three- to five-year, fiscal frameworks to assure markets that extraordinary increases in deficits will be reversed once economic activity recovers. As a result, the path for public debt—and public borrowing needs over the medium term—may appear uncertain. In addition, most governments are unable to borrow for as long a period as those in industrial countries. That means that they have to refinance, or roll over, a substantial share of the public debt in any given year. The debt of emerging market countries is also highly vulnerable to shifts in investors' risk appetite. This last factor is especially important, because shifting perceptions of risks regarding fiscal sustainability—or the government's ability to finance a higher deficit over the medium term—can lead to substantial upward pressure on interest rates and capital outflows. Furthermore, the large increase in public debt levels in industrial countries adds to uncertainty with respect to world interest rates and the availability of financing for emerging markets over the medium term.

Fiscal policy effectiveness

Consider the case of a government that enjoys a high level of credibility in the fiscal framework and a low public debt burden. Under normal financing conditions, an increase in government expenditure, financed by the issuance of domestic debt, can lead to higher output growth. Interest rates rise relative to what they would have been (the baseline), in part because of higher levels of public debt. These effects are unlikely to constrain the effectiveness of fiscal policy, however, in part because the current baseline already incorporates low interest rates caused by the global slowdown and glut of savings.

For example, in a simulation exercise on a representative small Latin American economy, using the IMF's Global Integrated Monetary and Fiscal Model (Kumhof and Laxton, 2007), an increase in public investment of about half a percent of GDP could raise output, on average, by slightly less than half a percentage point in the first year. The net results of fiscal expansion on growth also depend on the response of monetary policy and the initial conditions assumed in the baseline.

However, in a situation in which the higher deficit leads to concerns about financing over the medium term or the sustainability of public debt, fiscal policy is much less effective in stabilizing output. Under these types of circumstances, concerns about financing lead investors to demand a higher risk premium for holding government debt, which pushes up interest rates. In economies with flexible exchange rates, the higher risk premium also contributes to a depreciation of the exchange rate—which boosts the cost of imported inputs, switches spending toward home goods, and reallocates resources toward exports and import-substituting activities. In economies with predetermined exchange rate policies (such as a fixed exchange rate or a crawling peg), interest rates must increase by even more to protect the exchange rate, undermining the effect of the fiscal expansion on economic activity. Depending on the credibility of the fiscal framework, the public debt level, and the monetary policy framework, these higher interest rates can even lead to a decline in output in response to higher budget deficits.

Composition of stimulus matters

Beyond issues of financing, the efficiency of the proposed measures as an instrument of fiscal stimulus must also be considered. The general lessons for Latin America, in this regard, are similar to those for other regions. As indicated in Spilimbergo and others (2008), preference should be given to measures that have large fiscal multipliers, can be implemented quickly, and can be reversed once the economy stabilizes. Policy actions that meet these criteria include accelerating planned investment and/or maintenance, temporary tax cuts targeting those with a high propensity to consume (rather than save the cut), and the expansion of unemployment benefits. Spending that cannot be easily reversed once the economy stabilizes, and is not well targeted—for example, an increase in public wages—is less desirable from this standpoint. The long-term trend in Latin American spending toward rising primary current outlays (expenditure minus interest payments) also suggests caution in this regard. These outlays, for example, increased by about 2 percentage points of GDP between 2000 and 2008.

The bottom line is that the scope for fiscal stimulus must be analyzed on a case-by-case basis. In several countries, the slowdown in private sector activity may provide room for a temporary and well-designed fiscal stimulus. Governments with high policy credibility, low debt burdens, and flexible monetary frameworks are well positioned to conduct effective countercyclical fiscal policy. In countries with low credibility, however, countercyclical fiscal policy efforts may be counterproductive. In intermediate cases, efforts to boost credibility may pay handsome dividends.

For example, governments that have not already done so will benefit from making additional progress in developing sustainable medium-term fiscal frameworks. These frameworks should incorporate specific strategies of the government for dealing with transitory shocks (such as a deterioration in the global environment or commodity prices that sharply reduces economic growth). They should also include specific plans for addressing long-term fiscal challenges, such as pension spending. Finally, they should also delineate how the government would react if contingent or possible fiscal risks materialize. Building this kind of credible, rules-based framework will assure markets that there is sufficient room for fiscal expansion in the shorter term, without threatening fiscal sustainability over the longer term.

References:

Kumhof, Michael, and Douglas Laxton, 2007, “A Party Without a Hangover? On the Effects of U.S. Government Defi cits,” IMF Working Paper 07/202 (Washington: International Monetary Fund).

Spilimbergo, Antonio, Steve Symansky, Olivier Blanchard, and Carlo Cottarelli, 2008, “Fiscal Policy for the Crisis,” IMF Staff Position Note 08/01, December (Washington: International Monetary Fund).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org