Snapshot of Another Monetary Union

Finance & Development, March 2012, Vol. 49, No. 1

PDF version

![]() IMF podcast: Caribbean Union Faces Similar Challenges to Euro Area

IMF podcast: Caribbean Union Faces Similar Challenges to Euro Area

Moving forward with reforms should help the Eastern Caribbean Currency Union weather the current economic uncertainties

THE Eastern Caribbean Currency Union (ECCU), one of four monetary unions in the world, is—despite some differences—in many respects a microcosm of the European Economic and Monetary Union. Surging fiscal deficits, a lack of fiscal integration, unsustainable debt, and challenges in the financial sector are threatening the ECCU’s very foundation. As in the euro area, the common currency’s continued success rests on the region’s ability to collectively enforce fiscal discipline and harmonize financial sector regulation and supervision.

Six of the members of the ECCU are independent countries—Antigua and Barbuda, Dominica, Grenada, St. Kitts and Nevis, St. Lucia, and St. Vincent and the Grenadines. Two are territories of the United Kingdom—Anguilla and Montserrat. All eight are small, open island economies that depend to a large extent on tourism, especially from the United States, the countries’ major trading partner. As such, they are highly vulnerable to external shocks.

Economies of scale, risk sharing, rationalizing public services, and stronger representation in international settings are benefits the ECCU stands to gain from closer integration. Unlike the euro area, and given the small size of the economies, benefits from increased intraregional trade will be more limited.

But the 2008–09 global economic and financial crisis exposed significant weaknesses in the setup of the currency union. The crisis led to a surge in already very high public debt and revealed shortcomings in the financial sector. The authorities have responded on a number of fronts, but policies have been piecemeal and uneven, and many difficulties remain.

It’s not all bad news

The Eastern Caribbean dollar is pegged to the U.S. dollar and underpinned by a quasi-currency-board arrangement, which has contributed to macroeconomic stability and low inflation rates and a relatively sophisticated financial system. With bank assets topping 200 percent of GDP, the region is among the world’s most highly monetized economies.

The Eastern Caribbean Central Bank (ECCB) is responsible for monetary policy and for regulating and supervising the banking sector. Given the quasi-currency-board arrangement, which—unlike in the euro area—limits the use of monetary policy tools and lender-of-last-resort capacity, the ECCB’s main job is preserving the currency’s external value. It also manages a common pool of reserves and extends credit to governments and banks when needed—up to a limit determined both by the reserve coverage and by individual country limits. Under the quasi-currency-board arrangement, the ECCB must hold foreign exchange equivalent to at least 60 percent of its demand liabilities (mainly currency in circulation and commercial banks’ non-interest-earning reserves), but operationally it targets 80 percent coverage; and in practice it has been close to 100 percent.

In addition to having a monetary union and a regional central bank, the Eastern Caribbean region is a free trade area—but still an incomplete customs union and common market. A customs union is in place in most sectors of the economy, but tariffs are not fully harmonized and the countries still depend on import-related revenue. As for a common market, so far, free movement of labor is limited to skilled labor and the informal sector, but the region is implementing measures to ensure the free movement of its citizens. With an open capital account and companies and financial institutions free to operate anywhere in the region, the financial sector is already well integrated. And despite its small size, the region has started to develop a relatively well-functioning regional government securities market for treasury bills and bonds.

Forging ahead

Faced with the impact of the global economic and financial crisis, the region has accelerated its efforts to integrate. In 2010, the Caribbean heads of government committed themselves to stabilizing their economies and creating better conditions for strong economic growth. Shortly thereafter, the region ratified a revised economic union treaty. The revised treaty will strengthen governance by delegating some legislative authority directly to the heads of government. In another step, the region agreed to establish an assembly comprising elected parliamentarians from each member of the currency union (including both ruling and opposition parties), which could serve as a precursor to a regional parliament. The revised union treaty also mentions fiscal policy coordination, but unlike trade, financial, and monetary policy, it remains the sole purview of national governments.

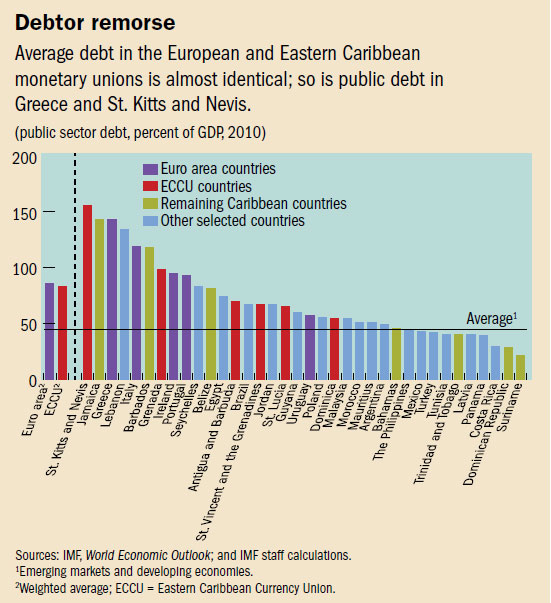

As the European experience shows, coordinating fiscal policy can be especially difficult, and in the ECCU, it remains in its infancy. A ceiling on debt-to-GDP ratios of 60 percent—to be achieved by 2020—was supposed to bring significant peer pressure to bear on budget policies, but has proven difficult to achieve. Some of the members of the currency union are among the most highly indebted in the world (see chart), and all independent countries, except Dominica, exceed the target debt-to-GDP ratio of 60 percent.

The weakest link

The success of the common currency will depend on simultaneously satisfying eight national budget constraints, since cross-border spillovers—especially via the financial sector—from the weakest member could undermine confidence and trigger a regionwide crisis.

The current high debt calls for a short-term mechanism to enforce fiscal discipline. In the medium term a fiscal union or a more centralized regional fiscal authority should be considered. As a first step, in 2011, the governments announced annual fiscal targets, and a number of countries have successfully implemented comprehensive fiscal reforms to address the debt overhang (see box on St. Kitts and Nevis). However, other countries must set more ambitious targets to achieve the 2020 public-debt-to-GDP ratio goal of 60 percent, and the union currently lacks enforcement mechanisms.

Coming out from under

With public debt at almost 160 percent of GDP—a ratio similar to that in Greece—St. Kitts and Nevis is the most indebted country in the Eastern Caribbean Currency Union and one of the most heavily indebted countries in the world. The majority of the debt is domestic, and the government has relied heavily on short-term financing, which exposes it to significant rollover risks. To address these challenges, the government embarked on a comprehensive and multipronged reform program with the objective of bringing the debt-to-GDP ratio to 60 percent by 2020.

•Fiscal adjustment: The cornerstone of the program included a new value-added tax, a drastic 80 percent increase in electricity tariffs, as well as measures to contain wages. Although the fiscal adjustment would reduce public debt to about 130 percent of GDP by 2016, that debt remains unsustainable and extremely susceptible to growth shocks.

•Debt restructuring: In June 2011, the government publicly announced the start of a comprehensive debt restructuring seeking a significant debt reduction.

•Guarantee: To support the government’s debt restructuring, the Caribbean Development Bank agreed to provide a partial guarantee for the new exchange instruments, which should significantly improve the success of the debt exchange.

•Debt-for-equity swap: To address the country’s extraordinary debt levels, the government is also using a debt-for-equity/land swap.

•Stabilization fund: To maintain the health of the financial system during the debt restructuring, the government established a special banking sector reserve fund at the Eastern Caribbean Central Bank to provide temporary liquidity to domestic financial institutions, if needed.

•IMF loan. To accompany the government’s economic reform program, the IMF approved a three-year Stand-By Arrangement in the amount of $80.7 million.

Although the ECCB is responsible for banking supervision in the eastern Caribbean, financial institution licensing and supervision of nonbank financial entities remain in the hands of national governments, which can lead to regulatory arbitrage and overbanking. Capacity constraints and a significant risk of spillovers between banks and nonbanks and across countries call for a competent regional regulator or supervisor to oversee the nonbanking sector. Closer collaboration between bank and nonbank supervisors and consolidation of the financial sector are needed as well.

Setting the example

The ECCU has taken a number of steps in recent years to strengthen integration as a way to deliver stronger economic growth and a more stable financial sector. But continued very high debt, financial sector challenges, and insufficient progress in coordinating regional policies have left the region vulnerable and could undermine confidence in the future.

Yet with strong leadership, the time is ripe for bold reforms to strengthen the currency union, especially when it comes to fiscal policy and the financial sector. ■

This article draws on the forthcoming book Macroeconomics and Financial Systems in the Eastern Caribbean Economic and Currency Union (OECS/ECCU)—A Handbook, ed. by Aliona Cebotari, Alfred Schipke, and Nita Thacker (Washington: International Monetary Fund).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org