A Change in Focus

Finance & Development, September 2012, Vol. 49, No. 3

Malhar Nabar and Olaf Unteroberdoerster

PDF version

![]() The Chinese… Ask the IMF

The Chinese… Ask the IMF

China’s external surplus is dwindling, with repercussions for its Asian trading partners

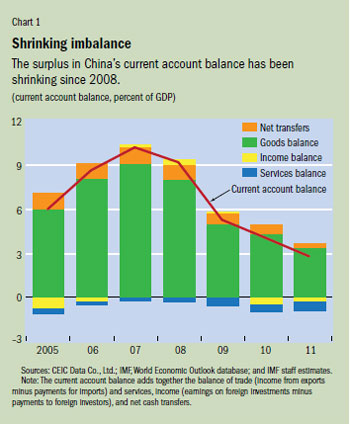

For the past five years, the global economic news has often featured declining numbers: asset prices, down; employment, down; industrial production, down. Add to this list China’s external surplus. The world’s second-largest economy has seen a key measure of its surplus with trading partners—the current

account balance, which nets payments to foreigners

For the past five years, the global economic news has often featured declining numbers: asset prices, down; employment, down; industrial production, down. Add to this list China’s external surplus. The world’s second-largest economy has seen a key measure of its surplus with trading partners—the current

account balance, which nets payments to foreigners  and income from abroad—drop from $412 billion, or 9.1 percent of GDP, in 2008 to $202 billion, 2.8 percent of GDP, in 2011 (see Chart 1).

and income from abroad—drop from $412 billion, or 9.1 percent of GDP, in 2008 to $202 billion, 2.8 percent of GDP, in 2011 (see Chart 1).

Falling numbers generally reflect troubled economic times. But could the decline in China’s external surplus instead be welcome news and a sign that its economy is rebalancing—away from exports toward stable, domestically driven growth? If that is the case, then the rest of the Asian economies will have to adjust because they have become so closely linked to China.

Declining surplus

The sharp compression in China’s external surplus undoubtedly reflects weak demand in its largest export destinations. Most people think of clothes, footwear, and toys from China feeding the U.S. consumer frenzy during the boom years prior to 2007. But Chinese exporters had made much broader inroads into the U.S. market beyond Wal-Mart and Target. Exports of machinery and equipment to the United States contributed 10 to 15 percent of China’s overall export growth in the early 2000s. That contribution has declined to about 5 percent during the postcrisis period because U.S. private investment, particularly in the housing market, has been subdued. At the same time, China’s imports of minerals and commodities have risen significantly since the crisis, in part due to increases in spending the government undertook to shore up domestic activity.

But beyond these cyclical forces, there are deeper elements at work.

First, China’s dramatic policy response to the global financial crisis—centered on infrastructure such as highways, high-speed rail, and improvements to ease travel between the inland provinces and the coast—contributed to a steep increase in the level of investment. As a percentage of GDP, investment spending in China rose from 41 percent before the crisis to 48 percent by 2009. Once the stimulus program started to wane and infrastructure spending began to slow, strong private sector manufacturing activity and construction of social housing ensured that investment remained close to 50 percent of GDP in 2011.

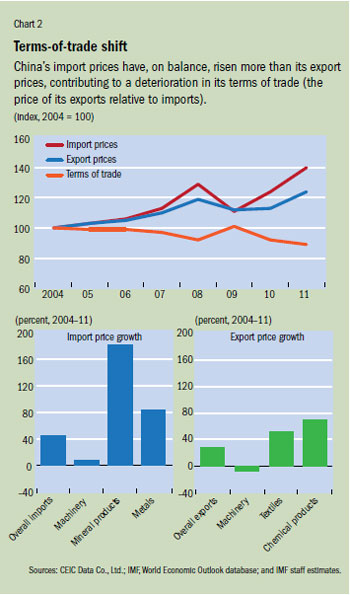

Second, China’s terms of trade (the average price of its exports relative to imports) have worsened in recent years, starting well before the global financial crisis (see Chart 2). As China has developed, its imports have shifted toward minerals, whose prices have been rising, while its exports have moved toward machinery, where competition has kept prices in check. Other export-oriented economies, notably Japan and Korea, experienced similar declines in their terms of trade as they developed. In China’s case, the sheer size of its trade flows implies that its external surplus has been highly sensitive to shifts in the prices of its exports and imports. And since 2009, the sustained strength in demand for imported commodities and minerals associated with China’s investment boom has reinforced this underlying dynamic of worsening terms of trade.

Third, reflecting in part the underlying shifts in the domestic economy, the real appreciation of China’s currency, the renminbi, has also contributed to a decline in its trade surplus.

A sustained rebalancing?

Do China’s shifting trade patterns represent a sustained rebalancing of its economy away from export dependence? Although policy efforts have achieved much in reorienting the economy toward domestic demand, so far the decline in China’s external surplus has been largely achieved through higher investment. The evidence does not yet indicate that household consumption is rising steadily as a share of GDP (see “Sino-Spending,” in this issue of F&D). It is possible that the growth in capacity from the recent elevated investment could eventually be used for domestic production—in higher final sales to Chinese households. But it could also lead to future increases in exports if Chinese firms instead continue to look outward. Alternatively, if the investment turns out to have been misallocated and demand is not forthcoming (domestic or external), it could show up as excess capacity and result in more bad loans in the banking system. At this point, it is too early to determine how the new capacity will be used. However, it is fair to say that there is growing concern that domestic imbalances are on the rise even as the external ones retreat.

China’s policymakers are cognizant of these risks. The overall policy direction in China, as laid out in 2010 in the 12th Five-Year Plan, focuses on accelerating the transformation of the economy toward one driven by household consumption. Policymakers are motivated equally by the side effects of China’s existing growth model—high capital and energy intensity, relatively low job creation, and a shrinking income share for labor—and by the sluggish nature of the global recovery. Achieving such a transformation will require changes that include

•Higher household disposable income: The floor on urban wages was raised across the country last year. To protect low-skilled and entry-level workers with minimal bargaining power, future increases in the minimum wage will have to keep pace with the increases in the compensation of more experienced and skilled workers. In addition, lowering the social contribution payroll tax (the combined employer and worker rate can exceed 40 percent of wages in some cases) would lift the share of remuneration captured by households and induce them to consume more. At the same time, a stronger renminbi would make imports cheaper and raise household purchasing power over imported consumer goods.

•A stronger social safety net, which would reduce household precautionary saving and increase consumption: Access to health care must continue to improve—through the recently expanded government health insurance programs, better training of personnel, and adequate incentives for skilled medical staff to relocate to rural areas. The complexity of regulations covering pension programs could be further simplified to encourage greater participation in pension plans. Also, more comprehensive education subsidies would ease the impulse to save, particularly among young households.

•Increases in input costs and improved corporate governance: Government subsidies and directives on the cost of production inputs (such as land, energy, and capital) have steadily tilted the economy further toward capital-intensive production. Incentives for excessive investment would be reduced if input costs were raised closer to levels in comparable economies and if the cost of capital were aligned with its high return. The effect of these measures would be greater if they were combined with corporate governance reforms requiring large state-owned enterprises to make more substantial dividend payments rather than hoard profits.

•Financial sector reform: The existing system of bank-based financial intermediation—in which the authorities guide interest rates and the allocation of credit—tends to favor large corporations at the expense of households and smaller firms. A greater reliance on market forces to determine interest rates and improved access to a wider range of saving and financing options would improve the efficiency of investment, lift household capital income, and boost consumption.

If these structural reforms were put in place, household income and consumption would rise faster, investment would decline as a share of the national economy, and China would successfully move to a consumption-driven growth model with structurally lower external surpluses. Such an outcome would be the most beneficial for China and its trading partners, many of which, particularly within Asia, are already significantly affected by the changes in China’s trade patterns.

China’s Asian trading partners

To examine the effect of the shifts in China’s trade on Asian trading partners it is useful to distinguish among China’s roles as a source of regional demand, an export-processing hub, and a competitor.

Asian economies have clearly benefited from China’s strong domestic demand since the recent global recession, in particular for commodities and capital goods. While the rapid growth of Asian exports to China has been fueled by its role as the center of an Asian supply chain that culminates in exports to advanced economies, economic activity within China has become more important as a source of demand in recent years. IMF estimates suggest that, when Japan is excluded, about 60 to 70 percent of the recovery in Asia’s exports to China above precrisis trends can be attributed to China’s domestic demand.

Overall, China’s demand for investment goods has risen more sharply than its demand for consumer goods. As a result, based on value added, the typical Asian trading partner exports roughly 30 percent more capital goods to China than consumer goods, a reversal from the ratio of capital to consumer goods exports 10 years ago. For Asia’s leading capital goods exporters—Japan and Korea—China accounts for 20 to 25 percent of such exports, a fourfold increase from a decade earlier.

Exports to China from commodity producers such as Australia and Indonesia have also risen sharply. China accounts for about two-thirds of the world’s iron ore imports, half of its soybean imports, and about one-third of metals imports. As a result, Chinese demand has an impact beyond Asia. In Africa, for example, Chinese firms have become major investors in the mining and infrastructure sectors. In Latin America, the economic cycle depends in no small measure on economic activity in China. According to recent IMF estimates (2012), should production in China abruptly slow (a hard landing, as economists say), commodity prices would fall by about 20 to 30 percent and severely affect economic activity, fiscal revenue, and debt levels in Latin America. That would be an impact similar in magnitude to what the region experienced after the collapse of the U.S. investment banking firm Lehman Brothers in 2008.

However, regional trading partners would have to adapt to rebalancing in China that shifts from investment-led to consumption-led growth. To begin with, despite rapid growth, China’s role as an importer of consumer goods is still small. The world’s second-largest economy accounts for only 2 percent of the world’s consumer goods imports. In addition, Chinese consumers have increasingly turned toward domestically produced goods—China’s share in global consumer goods imports has fallen behind its share in global consumption. This may reflect a number of factors, including the inability of foreign producers to overcome implicit barriers—for example, by setting up large retail and distribution networks—increased competitiveness from domestic producers, or a shift by foreign firms to produce locally to adjust to Chinese consumer preferences and to be closer to the customer. Whatever the reasons for the relative decline in Chinese imports of consumer goods, a shift in the share of global consumer demand toward China would not automatically imply a proportional increase in global consumer goods imports. Nevertheless, suppliers in Asia and elsewhere could still benefit, if only indirectly, from a shift toward consumption-led growth in China by integrating themselves into the supply chain of Chinese firms that cater to the domestic market.

At the hub

Asian trading partners have also benefited from growing export links with China, which is the center of the Asian supply chain hub. China today accounts for more than 50 percent of all imports of intermediate goods (those used as part of the production process) within the region—twice its share in the mid-1990s. For Asia excluding China, the share of intermediate goods exports to China in total exports has doubled over the past decade. That is in contrast to the share of direct consumer goods exports to the United States and the euro area, which has steadily declined (see Chart 3). As a result of being part of the supply chain, Asian economies’ exports to China have increasingly been driven by the success of China’s exports in world markets. This means, however, that if the rapid growth of Chinese exports slows, Asian trading partners will also face significant headwinds. We estimate that a 1 percentage point drop in Chinese export growth would lower the growth of exports of other Asian economies to China by about ⅓ percentage point. Moreover, for most Asian economies—which export mainly manufactured goods, not commodities—Chinese exports rather than Chinese domestic demand appear to be the dominant factor in determining their exports to China. The link with China’s export performance appears to be relatively stronger for capital goods exporters such as Japan and Korea and for some smaller highly open economies in Southeast Asia.

On the other hand, because Asian economies are linked through supply chains, China’s role as a competitor has been less important. In fact, measuring the increase in China’s share of gross exports to leading markets overstates its importance. China’s dominance shrinks when its share is measured on a value-added basis—which nets out direct and indirect inputs from other Asian economies. In the case of the United States for example, China’s direct share of gross imports of final goods from Asia was 62 percent in 2010, whereas, on a value-added basis, its share was less than 50 percent. The implication for more advanced economies in Asia is that any potential increase in competition with China as its exports shift increasingly toward high-tech goods will also depend on China’s ability to capture a larger share of the value chain. While the imported content in Chinese exports gradually increased through the mid-2000s, it began to fall in recent years—a trend that could be reinforced by China’s rapid buildup in physical and human capital, which could allow it to capture large parts of the technology-intensive value chain. In addition, rising fuel and transportation costs could lead to a partial reversal of so-called vertical trade integration by reducing the number of locations in a production chain. However, more outsourcing and relocation of industries could result from rising wages in China, which may help low-income economies in the region, given their abundance of cheap labor.

Headwinds

For now, the recent sharp decline in China’s external surplus appears to be the product of a secular worsening of China’s terms of trade, robust import growth fueled by very high investment demand, and cyclically weak external demand. At the same time that China’s external imbalances are shrinking, there is concern that new domestic imbalances may be emerging. As a result, Asian trading partners that have benefited from China’s investment-led growth may face growing headwinds to their exports in the event that the domestic imbalances eventually disrupt growth in China. Given the importance of vertical supply chain links with China, they would also be hurt if China’s exports were to slow. By contrast, the net benefits for Asian trading partners from rebalancing in China would be larger and more lasting, if they are able to increase their direct and indirect access to Chinese consumers. ■

Malhar Nabar is an Economist and Olaf Unteroberdoerster is a Deputy Division Chief, both in the IMF’s Asia and Pacific Department.

This article is based on a recent IMF Working Paper (12/100), “An End to China’s Imbalances?” and Chapter 4 of the IMF’s April 2012 Regional Economic Outlook: Asia and Pacific, “Is China Rebalancing? Implications for Asia.”

Reference

International Monetary Fund (IMF), 2012, Regional Economic Outlook: Western Hemisphere (Washington, April).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org