Migration Meets Slow Growth

Finance & Development, September 2012, Vol. 49, No. 3

PDF version

![]() Papademetriou on the changing face of migration

Papademetriou on the changing face of migration

The global movement of workers will change as the economic crisis continues in advanced economies

The United States’ long-standing argument with Mexico over illegal migration is on the wane. Net migration from Mexico is near zero and apprehensions of illegal immigrants (many non-Mexican) at the U.S. southern border are at levels last seen in 1970 (U.S. Border Patrol, n.d.).

Massive U.S. investments in border controls, aggressive interior enforcement measures, a Mexican economy that has been growing much faster than the U.S. economy since 2010, and ever-deeper cooperation with the United States on the issue explain a good part of the decline in illegal migration. But even more important is that a sustained decline in Mexican fertility means that fewer new Mexican workers are entering the labor force each year at the same time that job opportunities in the United States are much lower as a result of the ongoing economic distress.

The aftermath of the Great Recession has not only affected immigration between the United States and Mexico. Immigrants from lower- and middle-income countries have been particularly vulnerable to the destruction of jobs in most advanced economies. Migration—which has been both driving force and byproduct of globalization and the ever-increasing interconnectedness it fuels—now comes face to face with the global crisis.

The crisis may have ended a period in which the benefits of openness, including large-scale immigration, were embraced with relatively few questions across advanced economies. In the years ahead, immigration is likely to become more selective, and lower-skilled migrants are likely to be less welcome—at least as prospective permanent residents, let alone as fellow citizens.

Job destruction

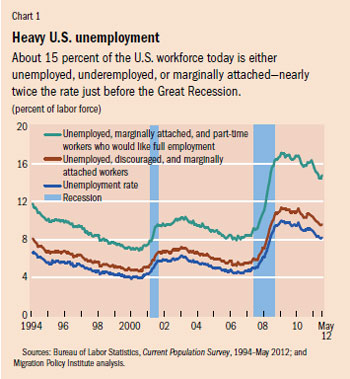

In the United States, for example, labor market distress has reached levels not seen since the Great Depression. About 23 million people, roughly 15 percent of the labor force, are unemployed or underemployed—including workers in involuntary part-time situations and those who become marginally attached or discouraged (see Chart 1). The share of men who hold a job is at the lowest level since 1948, when the U.S. Labor Department began collecting these data, while for all workers it is the lowest since 1981. At mid-2012, nearly 42 percent of the unemployed had been jobless for 27 weeks or longer, increasing the prospect that their skills will atrophy and raising the risk that even as large numbers remain unemployed, jobs will go begging because of the growing gap between the skills available and the skills employers require (see “The Tragedy of Unemployment,” in the December 2010 issue of F&D). Hardest hit are middle-aged workers (45 to 64 years old), who both remain unemployed longer than any other age group and find it harder to get jobs with wages similar to the ones they lost. Moreover, investments in productivity-enhancing and labor-saving technologies during recessions reduce the post-recession demand for workers (Katz, 2010). Notwithstanding a smaller workforce, the United States has a higher GDP than five years ago.

These troubling figures are not limited to the United States. Five years after the first signs of distress in the U.S. mortgage market that led to the global financial crisis and three years after a halting recovery began in most advanced economies, the jobs crisis in Europe as a whole is even worse. In April 2012, 24.7 million persons in the 27 countries of the European Union (EU) were unemployed, 8 percent more than a year earlier (Eurostat, 2012). The situation becomes even more dire when one considers all measures of economic distress; 42.6 million EU workers were unemployed or underemployed in 2011.

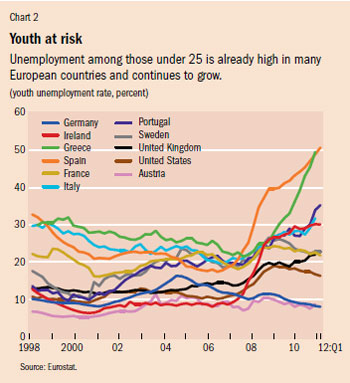

Moreover, youth unemployment is extremely high and continues to grow in some EU countries (see Chart 2). The potential consequences of this phenomenon are disquieting. They include long-term “economic scarring,” the risk of a “lost generation” of workers, and the potential for social disorder—the appeal of extreme ideologies is strongest among those with dismal prospects.

While millions of workers have been hurt by the crisis, the pain is uneven. Men, young workers—particularly young immigrants—and members of minority groups have fared the worst. In the United States, Hispanics, blacks, middle-aged workers, and teenagers have been hit harder than other groups. In Europe, immigrant groups that absorbed a disproportionate economic and labor market hit include those from Andean and North African countries in Spain; Bangladeshis, Pakistanis, and Portuguese in the United Kingdom; and most immigrants in Greece.

These groups are consistently vulnerable for a variety of reasons.

•Skills. Immigrants typically have lower skill levels or skills that are more difficult to recognize or translate into the local economy, factors that are compounded by poor language ability.

•Experience. Young workers, immigrants, and disadvantaged minorities often have less work experience and face more or less formal “last hired/first fired” policies.

•Contingent employment. These groups are often in jobs that are more temporary in nature and expand and contract to reflect demand cycles.

•Training. Employers typically have made fewer investments in training these workers, which makes them more expendable.

•Employment sector. The sectors in which many of them worked were hit hardest by the crisis. In the United States and Spain, for example, the bursting of the housing bubble led to the collapse of the construction sector, which was a source of employment for large numbers of immigrants, many of them illegal residents.

Migration suffers

In the past three decades, migration from low- and middle-income countries to higher-income countries grew across all skill and education levels. The United Nations estimated in 2008 that the number of immigrants—authorized or unauthorized—to the more developed regions of the world would nearly double, from 5.4 percent in 1980 to 10.5 percent by 2010 (United Nations, 2009).

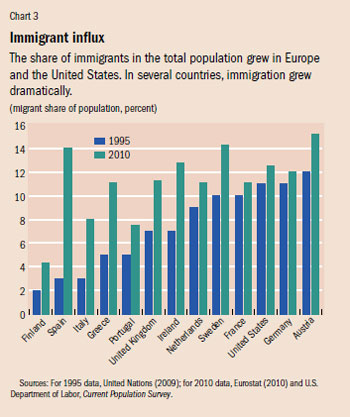

In several instances, often in countries whose main experience with migration had been as senders, not recipients, of immigrants, immigration grew at rates that were unprecedented in peaceful times. In Spain, for instance, the number of immigrants grew from a few percentage points to 14 percent of the population in less than 15 years. Remarkably rapid growth also occurred in Finland, Ireland, the United Kingdom, Greece, and Italy (see Chart 3). In all instances, rapid rates of growth gave these countries inadequate time to adjust their legal and institutional frameworks to incorporate newcomers effectively and prepare their publics for the changes that fast-paced increases in migration entail. This sowed the seeds for the recent reaction to immigration, such as the rise of nationalist parties with strong, if often selective (typically anti-Muslim), anti-immigration platforms. The economic crisis has simply intensified the negative reaction to immigrants.

Porous borders and a general belief that immigration had positive economic effects allowed vast numbers of migrants to relocate, legally and illegally. Indeed, expanding economies absorbed the additional labor with ease. Consumers enjoyed the reduced costs of goods and services produced by lower-paid immigrants, and many economic policymakers praised the restraining effect of immigration on wage inflation—a phenomenon that domestic workers who are directly affected understandably loathe.

The Great Recession changed that.

To be sure, international migration has continued to grow. But most of that growth has been in middle-income, and particularly in emerging, economies—such as Brazil, Russia, India, and China, but also South Africa, Mexico, Turkey, Indonesia, and several other Southeast Asian countries. Total immigration to high-income countries has, however, grown very slowly relative to the growth rates of the past three decades, even though English-speaking countries have continued to admit significant numbers of new immigrants (United Nations, 2012).

A new normal?

The postcrisis environment will be one of uncertainty. And it spawns a host of questions, many essentially unanswerable right now. Will high unemployment and slow, uneven employment growth gradually recede, with growth and “traditional” immigration patterns returning to roughly precrisis levels? Or will economic growth and immigration levels in high-income countries settle at more moderate levels? Have advanced economies arrived at an inflection point in their always complex immigration histories whereby one can expect a sustained period of lower labor market demand and much more selective migration? How will continuing labor market distress affect behavior among groups often on the margins of the labor force, whose decisions nonetheless determine the overall supply of workers: less-educated workers; discouraged workers; the urban poor; disadvantaged and otherwise marginalized workers (many of whom are minorities); women now out of the labor force who want to return to it; retirees returning to work or older workers postponing retirement; and those who had shunned certain jobs as too difficult or too socially undesirable? Collectively, the choices these groups make will help determine the number of immigrants that receiving countries will “need” in the coming years—and the economic, labor market, and social welfare decisions of governments, employers, and individuals will help shape these determinations.

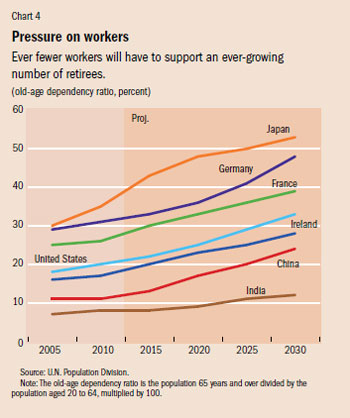

Nonetheless, some of the underlying drivers of migration will not change. Baby boomers may retire later than originally projected, but aging will continue to generate demand for immigrant workers both to work and to pay the taxes to support social benefits and care for the aged. The new worker pipelines in countries with long-term low fertility rates will grow smaller, which, together with aging populations, will put increasing pressure on the producing part of the labor force. Old-age dependency ratios—the number of those who are over 65 years old divided by the number of those who are between 20 and 64 years old—will grow ever larger (see Chart 4). Education and training systems in wealthy countries will continue to struggle to meet labor market demand because no country can anticipate the future demand for skills well enough, nor develop competitive specialized domestic industries by relying exclusively on homegrown talent. The challenge for policymakers will be offering credible policy responses during a period of extraordinary uncertainty and persistently high unemployment, while being active in the hunt for global talent and maintaining the openness and tolerance that undergirds competitiveness in the long run.

In the meantime, certain forms of migration have continued to grow and will likely grow faster in the years ahead. Most respond to the opportunity differentials between countries, which is the major driver of immigration. Among them are the following.

Emigration from high-income countries due to economic distress. Some of it will be to former colonies where opportunities have become more plentiful. The flows to watch are those from countries such as Ireland and the Mediterranean member states of the European Union that moved from centuries-old traditions of emigration to becoming massive immigration players in little more than a decade. They now seem to be returning to their historical pattern.

Two-way migration flows among high-income countries and from high-income countries to fast-growing middle-income ones. Migration between high-income countries has been occurring for generations and accounts for about a quarter of all migration (United Nations, 2012). The free movement provisions of the European Union and the de facto openness of most wealthy countries to migration from countries of similar levels of development mean that such movements will continue to grow. North-South migration, which now stands at about 13 million persons, will likely grow robustly, focusing on the fast-growing middle-income countries and turning them into the next migration hubs, especially since they already host substantial numbers of immigrants from neighboring lower-income countries. In fact, their active effort to attract talented immigrants from the North is well under way, focusing on enticing their expatriates to return by offering such incentives as tax and foreign exchange concessions and research opportunities. The actions of global firms attracted by similar incentives, by the availability of talent without some of the immigration constraints of high-income countries, and by the proximity to new and increasingly abundant middle classes eager to buy their products complete the circle.

Attracting skilled immigrants will become more of a policy target. Skills and talent are highly prized in an increasingly competitive world, and the search for them is intensifying. However, high-quality skills—such as degrees in the sciences, technology, engineering, and mathematics (STEM) from leading universities—will not always be as available as they seem to be today—which will have a profound effect on the fields of study immigrants choose and on educational institutions across the globe. Recruiting STEM graduates out of school is becoming the “lowest-hanging fruit” of immigration policy in many countries. Competition for these graduates can become heated very quickly.

The recent growth in international students will continue. More than 3 million students are studying outside their home countries today—nearly twice the number in 2000, and the number could more than double again by 2020 (UNESCO, 2011). The attraction is there for host countries—educating fee-paying foreign students is lucrative—and for students—the value of foreign education is increasing as competition for talent grows.

Finally, other forms of migration will also continue to rise—including investor and retirement migration, “adventure” migration, and migration by children of immigrants seeking to explore opportunities in their parents’ countries from the safety of citizenship in their parents’ adopted countries.

What may be equally important is that the character of migration is also likely to change. For most of the past 150 years, migration hewed to a well-established pattern in which family unification and citizenship were near-standard end products. But the greatest likelihood is that the new migration will be more temporary and contract based (more in the nature of “mobility” than traditional migration) and will typically not come with citizenship.

Inescapable realities

A closer look at the intersection between the ongoing fiscal and jobs crises and immigration in most of the highly developed world points to several important areas that need attention from policymakers.

First, authorities must reexamine some of the assumptions about the nearly unremitting demand for immigrant labor, and particularly the notion that large-scale immigration is essential to economic growth and prosperity. The reality is more nuanced. The future will most likely see much more selective migration and much more active management of the immigration system. Immigration politics, not just good governance, will see to it. Approving employer applications for new immigrants with few or otherwise easily obtainable skills may gradually become a thing of the past. Policymakers will also come to think harder about how and where to invest in the job skills of economically scarred and marginalized workers and those whom globalization has left behind. Once more, politics and responsible leadership will make that necessary. Moreover, the economic restructuring that the crisis has forced on nearly all advanced economies and the resulting investments in increased productivity make arguments for large-scale immigration harder to sustain. Finally, pressure will increase on receiving governments to enforce laws against illegal immigration and unauthorized employment that they may have been reluctant to enforce in the past.

Second, as the crisis continues, increasing numbers of the long-term unemployed will see their skills degrade further. Policymakers thus face the specter of growing structural unemployment—with which much of Europe has contended for a generation but the United States has mostly avoided. This suggests that governments and employers will have to redouble their efforts to invest in their legal workers regardless of their origin or prior qualifications and that workers will have to invest in themselves. When economic growth returns, employers and the broader economy will need a better-skilled and better-educated workforce. Those that have one will do well; those that do not will fall further behind—as will the economic sectors that employ workers without investing in them.

Third, the cuts to immigrant integration funds occurring in most advanced economies could spell further, and longer-term, social and economic troubles that will make the recovery more challenging than it need be. For instance, Spain zeroed out its integration budget earlier this year, and integration assistance and public services to immigrants and other marginalized groups are being cut in most countries. This means that immigrant groups that fared relatively well before the economic crisis are also likely to prosper during the recovery. But those already struggling will be less able to recover and will face huge obstacles to economic well-being that will likely continue into the next generation. The underlying drivers of successful immigrant integration—such as language ability, education, relevant skills and qualifications, credential recognition, local work experience, and professional contacts—are unlikely to have changed. But as employers choose from a large pool of unemployed workers, the importance of these attributes for immigrants will grow and the consequences of lacking them will be more devastating. ■

Demetrios G. Papademetriou is President of the Migration Policy Institute.

References

Eurostat, 2010, “Population by Sex, Age Group and Country of Birth.”

———, 2012, “Unemployment Statistics” (April).

Katz, Lawrence F., 2010, “Long-Term Unemployment in the Great Recession,” Testimony for the Joint Economic Committee, U.S. Congress. April 29, Washington.

United Nations, Department of Economic and Social Affairs, Population Division, 2009, “Trends in International Migrant Stock: The 2008 Revision” (United Nations database, POP/DB/MIG/Stock/Rev.2008).

———, 2012, “Migrants by Origin and Destination: The Role of South-South Migration,” Population Facts 2012/3.

United Nations Educational, Scientific and Cultural Organization (UNESCO) Institute for Statistics, 2011, Global Education Digest 2011 (Montreal).

U.S. Border Patrol, n.d., “Nationwide Illegal Alien Apprehensions Fiscal Years 1925–2011.”

U.S. Department of Labor, Bureau of Labor Statistics, January 1994–May 2012, Current Population Survey (Washington).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org