Transparency Matters

Finance & Development, December 2013, Vol. 50, No. 4

Luis Brandão-Marques, Gaston Gelos, and Natalia Melgar

The more forthcoming countries are, the more they can resist the ups and downs of global financial conditions

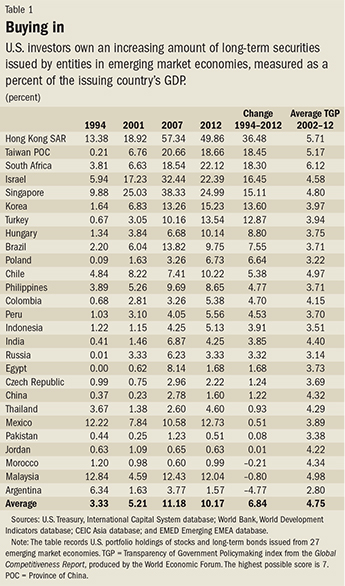

Over the past 20 years, emerging market economies have become increasingly integrated into world financial markets. For example, U.S. portfolio holdings of long-term securities (equities and long-term bonds) issued by entities from 27 key emerging market economies roughly tripled as a share of each country’s GDP between 1994 and 2012 (see Table 1).

This increase in financial integration has brought emerging market economies tremendous benefits. It has reduced their cost of capital (which has expanded investment opportunities), improved risk sharing and portfolio diversification, sped up the transfer of technology, and contributed to the spread of best practices in investor protection and governance.

But deepening financial integration has come at a price for many of these economies: it has increased their vulnerability to the ups and downs of international financial markets. However, that increased vulnerability varies significantly—it is higher for some countries, lower for others. To devise policies to reduce the volatility that can accompany increased global integration, governments must understand how country characteristics shape the way global financial markets affect emerging market economies.

To that end, we examined the role that country transparency plays in the amplification of financial shocks emanating from global financial centers. We found that the more transparent economies—those that provide more data and in a more timely fashion and have better corporate disclosure standards, more predictable policies, and better governance—react less sharply to both improvements and deteriorations in global market conditions than do the more opaque emerging market economies that score worse on various dimensions of transparency.

Country transparency and capital flows

Many individual country factors influence the speed and intensity with which financial shocks propagate across economies. Financial linkages, such as common exposures by banks and mutual funds, play an important role in the transmission of common shocks and in financial contagion. It is also known that financial integration, the result of lower barriers to cross-border financial flows, generally facilitates the international propagation of financial shocks (Bekaert and others, 2011).

Less clear, however, is the role played by country-level transparency—that is, the availability of information that allows investors to properly assess risks and returns associated with investing in a country. It is often asserted that more transparency can be beneficial both in attracting investment and in helping to avoid excessive volatility of capital flows. The argument is that more transparency enhances the orderly and efficient functioning of financial markets. Transparency reduces the occurrence of such phenomena as herding (where investors make certain decisions merely because they observe others making them), waves of investment flows driven by sentiment, and investor overreaction to news. The global financial crisis has drawn renewed attention to the role opacity plays in exacerbating financial shocks.

However, in principle, more transparency can actually result in higher volatility and, as a result, be destabilizing. For example, transparency might generate excessive provision of public information (through disclosures from governments or market participants), which could crowd out potentially more precise private information—reducing information efficiency and increasing volatility—especially when such information is confusing (“noisy,” in financial parlance) or unrelated to fundamental conditions. For example, the timely publication of preliminary (and imprecise) official data may lead market participants to overreact to such news, causing too much price volatility in financial markets (Morris and Shin, 2002). More transparency also contributes to financial integration (by reducing information costs and asymmetries) and can augment the simultaneous movement of prices across markets (Carrieri, Chaieb, and Errunza, 2013).

Although there is some evidence that supports the beneficial effects of country-level transparency (Gelos and Wei, 2005), the overall evidence is ambiguous. Moreover, existing empirical studies have focused largely on the transmission of financial shocks during crisis episodes.

We explored whether opacity at the country level amplifies the local impact of global market conditions over the business cycle by examining the behavior of bond and equity prices. The basic hypothesis is that when global financial conditions are benign, international investors become more prone to invest in markets whose underlying distribution of risks they understand less well (“ambiguous” markets) and then flee when global conditions deteriorate. Investors could behave this way for several reasons. They might become more comfortable with ambiguity when their other investments have performed well. Another possibility is that during difficult times fund managers face more scrutiny and more pressure to justify the asset composition of their portfolios and respond by reducing their exposure to assets whose risks are less well understood. Consequently, they are more prone to hold less transparent assets during good times than during bad times. Alternatively, ambiguity may make it harder for investors to separate fundamental shocks from pure noise shocks, inducing them to associate benign signals in the financial centers with good fundamentals in the ambiguous markets.

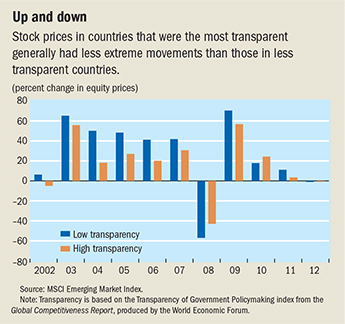

Whatever the reason (and the possibilities are not mutually exclusive), more opaque markets experience larger booms when financial market conditions are favorable, whereas the opposite is true during bad times (see chart).

Gauging transparency

Measuring country transparency poses significant difficulties. First, we need measures that capture some notion of the inability to pin down precisely how likely different events are. We are therefore interested in indices of opacity that gauge the availability of all relevant information the investor can use to assess the risks associated with investing in a given country. Second, we need indices that cover many countries and go back a long time. Therefore, we focused on indices measuring corruption, governance, corporate disclosure practices, accounting standards, and the transparency of government policies and statistics.

To quantify the impact of global financial shocks on asset prices from emerging markets, we used, as a proxy for liquidity conditions and risk aversion in financial centers, the VIX, which measures investor expectations of stock market volatility over the next 30 days. In doing so, we controlled for several different measures of country opacity (ranging from the degree of corporate disclosure and transparency of government policies to broader measures of opacity, such as perceptions of corruption). Using data for both stock and bond markets over the period 1997–2011, we consistently found that emerging markets that score worse on various dimensions of opacity measures react more strongly to global market conditions than economies that are more transparent.

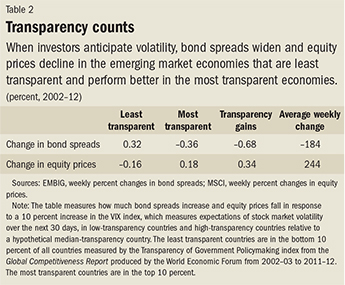

It is significant that this result holds even when we controlled for a broad range of measures of risk, credit quality, and liquidity (Brandão-Marques, Gelos, and Melgar, 2013). In fact, according to our estimates, in response to a 10 percent increase in the VIX (considered a mildly negative shock), the countries with the most transparent government policies would experience an increase in sovereign bond spreads (the difference between the rate a country pays to borrow and the rate on U.S. Treasury securities) roughly 0.4 percentage point lower than that of the median country. By contrast, the least transparent country would have an increase in those spreads of 0.3 percentage point more than the median country. The “transparency gains” for more transparent countries amount to roughly twice the average weekly change in spreads measured by the J.P. Morgan Emerging Markets Bond Index Global (an index that follows total returns of debt instruments issued to foreign buyers by emerging market economies). For equities, the gain is more significant and reaches almost two and a half times the average weekly increase in the MSCI Emerging Market Index, which measures the performance of about 1,600 stocks globally (see Table 2). This is roughly three times more than the increase in exposure that a country would get from doubling its international portfolio flows. Qualitatively, this result holds not only for government policies, but also for the other measures of transparency mentioned above.

Policy challenge

Our research implies that emerging markets are not helpless when it comes to responding to the ups and downs of global markets. Countries that wish to benefit from financial globalization can reduce its unpleasant side effects by becoming more transparent—that is, by providing more data and in a more timely fashion, improving corporate disclosure standards, increasing the predictability of policies, and, more generally, improving governance. In other words, increasing transparency may be an effective instrument for countries to consider before resorting to other measures aimed at reducing the adverse consequences of capital flows. ■

Luis Brandão-Marques is a Senior Economist in the IMF’s Monetary and Capital Markets Department, Gaston Gelos is a Division Chief in the IMF’s Monetary and Capital Markets Department, and Natalia Melgar is an Economist in the IMF’s Resident Representative Office in Uruguay.

References

Bekaert, Geert, Campbell R. Harvey, Christian T. Lundblad, and Stephan Siegel, 2011, “What Segments Equity Markets?” Review of Financial Studies, Vol. 24, No. 12, pp. 3841–90.

Brandão-Marques, Luís, Gaston Gelos, and Natalia Melgar, 2013, “Country Transparency and the Global Transmission of Financial Shocks,” IMF Working Paper 13/156 (Washington: International Monetary Fund).

Carrieri, Francesca, Ines Chaieb, and Vihang Errunza, 2013, “Do Implicit Barriers Matter for Globalization?” Review of Financial Studies, Vol. 26, No. 7, pp. 1694–739.

Gelos, Gaston R., and Shang-Jin Wei, 2005, “Transparency and International Portfolio Holdings,” Journal of Finance, Vol. 60, No. 6, pp. 2987–3020.

Morris, Stephen, and Hyun Song Shin, 2002, “Social Value of Public Information,” American Economic Review, Vol. 92, No. 5, pp. 1521–34.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org