Europe’s Road to Integration

Finance & Development, March 2014, Vol. 51, No. 1

History points to integration to overcome a tough crisis

Alarming headlines about Europe have been inescapable in recent years even if the latest outlook is somewhat better. Markets and the media have questioned Europe’s ability to deal with a severe financial shock and an economic downturn, even raising concern about the viability of the euro.

As bad as the crisis has been—and it has been extremely damaging, not least for the many people out of work—that should not obscure Europe’s achievement of a closely integrated region with some of the world’s highest standards of living. That this has been accomplished after two devastating world wars and the division of the continent between east and west for much of the 20th century is all the more remarkable.

Europe has experienced some crucial pushes toward integration in the past 25 years—the fall of the Berlin Wall in 1989, the wave of central European countries that joined the European Union in 2004, and the launch of the euro in 1999. The current crisis presents an opportune time to consider Europe’s path to integration so far and what lies ahead.

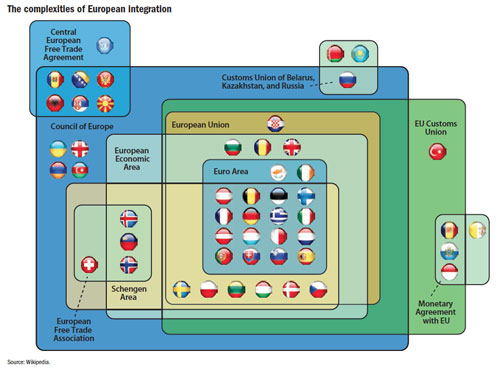

While Europe is much larger and more populous than the European Union alone, the Union has been at the heart of European integration, binding countries once in conflict and offering benefits well beyond its borders—as a key trading and investment partner across Europe and as a powerful catalyst for fundamental economic and governance reforms by many entrants and aspirants.

The past few years have been rocky, and there will surely be further bumps ahead. The crisis exposed weaknesses in the regional architecture and national policies, while eroding political support for closer ties. But integration has yielded substantial benefits for Europe so far, and continues to point the way forward.

Complex origins

More than six decades ago, six countries in western Europe (Belgium, France, West Germany, Italy, Luxembourg, and the Netherlands) decided to take economic cooperation a step further. The vision of the EU founding fathers, epitomized by the Schuman Declaration in 1950, was to tie their economies—including the reemerging West German economy—so closely together that war would become impossible.

Europe will not be made all at once, or according to a single plan. It will be built through concrete achievements which first create a de facto solidarity.

—Robert Schuman

The history of the European Union has been one of big and small steps toward ever-closer integration. Early on, leaders decided to integrate their key industries of the war and postwar years: coal and steel production. Tariffs were reduced, subsidies slashed, and national cartels dismantled. But unlike other forms of emerging postwar economic cooperation, the integration of Europe was defined by the creation of supranational institutions. Over the years these institutions have evolved into the executive, legislative, and judicial branches of the European project. The durability and continuous strengthening of these institutions is a demonstration of the power and the success of the project. A key milestone was the first direct European vote in 1979 when the European Parliament became the legislative power.

Geographically, the European Union also went through various stages of enlargement. In 1973, Denmark, Ireland, and the United Kingdom joined what was then the European Community. The 1970s saw deep social and political transformations in Greece, Portugal, and Spain, where military regimes and dictatorships were overthrown. Inspired by the prosperity and stability of the European Community, these countries joined the European project a mere decade later, strengthening their emerging democracies. The countries benefited enormously from free trade and common policies, in particular structural funds that were set up to foster convergence by funding infrastructure and productive investments in poorer regions.

Transition from communism

The most significant episode in Europe’s postwar political and economic integration was the collapse of the centrally planned economic systems at the end of the 1980s. The fall of the Berlin Wall stands as the defining moment of a long and multifaceted process of liberalization. More than 20 countries emerged from communism to take their places in democratic Europe, presenting both the greatest opportunities and the greatest challenges in European integration since the war.

In all cases the initial challenge for the transition was stabilization. The collapse of traditional trade and investment links and dislocation of domestic demand contributed to large output collapses in the early years of transition, ranging from about 10 percent in Poland and Hungary to some 40 percent in countries such as Latvia and Lithuania. As prices were liberalized, they tended to skyrocket, partly as relative prices were set by supply and demand rather than central planning, but with especially steep increases where state revenues dried up and governments had few sources of finance other than turning to central banks to print money. Currencies across the region devalued rapidly and banking crises were widespread. In some cases, where there was adequate political and institutional support for fiscal and monetary discipline, stabilization was achieved within a couple of years; others faced longer or multiple attempts to establish low inflation and sustainable public finances.

Following stabilization, the focus turned to institution building to improve the functioning of the economies, drawing on best practices from western Europe and the rest of the world. Countries faced huge challenges in privatization, public sector reform, and establishment of an environment conducive to reform. The creation of credible monetary and exchange rate frameworks—whether involving floating or different types of fixed-rate arrangements—in almost all countries was key to the success of transition. Integration has been particularly evident in the financial sector, with western European banks dominating in most of the transition countries. This has brought critical benefits in terms of know-how and financing. At the same time, the unfettered flow of capital into the region during the heady years of the early to mid-2000s stoked bubbles that burst in the ensuing global financial crisis.

Integration has contributed to strong convergence of incomes. Average GDP per capita across emerging Europe relative to advanced economies in Europe rose by about 50 percent between 1995 and 2013, despite the recent crisis. Sizable trade and investment links with western Europe were key to the growth and convergence progress that brought emerging Europe’s income levels to just under half of those in their advanced economy neighbors.

The European Union has been an increasingly important focus for the transition. In the 1990s, external assistance came mainly from other countries and international institutions such as the IMF, the World Bank, and the new European Bank for Reconstruction and Development. But as accession—the process by which countries join the European Union—gained steam, the European Union has played a critical role in developing institutions, guiding economic policy, and financing infrastructure. This process culminated in EU accession for 11 countries (4 of them already euro area members), and candidate status for an additional 3. This achievement was inconceivable 25 years ago and has brought tremendous benefits both to the transition countries and to the existing EU members (see Box 1), through increased trade, capital, and labor flows.

Box 1. Integration of East and West: Supply chains

The emergence of a German–central European supply chain is a good example of successful economic integration following the collapse of the Berlin Wall.

Since the 1990s the Czech Republic, Hungary, Poland, and the Slovak Republic have emerged as major manufacturing satellites—particularly in the automobile industry—of a production system with Germany at its hub. The evolution of this export-oriented system was spurred by large labor cost differentials, geographic proximity, and historical and cultural affinities and supported by large flows of foreign direct investment from Germany.

The supply chain benefits Germany by allowing it to produce and export goods in which it may not be competitive were it restricted to manufacturing within its national borders (see “Adding Value” in the December 2013 F&D). In economic jargon, its production possibility frontier has expanded. Meanwhile the emerging economies in the supply chain have received significant technology transfers, enabling particularly rapid income convergence. Economic theory predicts that, all else equal, poorer countries should grow faster than richer countries, but the central European countries belonging to the supply chain have been able to expand output at an even faster clip than can be accounted for by income differentials. Moreover, rapid export growth in these countries has been tilted in favor of knowledge-intensive sectors. So the supply chain is driving greater demand for skilled labor and creating opportunities for countries to move up the value chain over time.

Maastricht and the euro

Meanwhile, Europe’s core countries continued to grow closer. Early on, exchange rate variability between member states was reduced through the European Exchange Rate Mechanism (ERM), which allowed currencies to fluctuate around parities within predefined bands. In 1990, exchange controls within the European Economic Community were abolished, allowing for the free flow of capital. Although there were crises under the ERM—for example, the United Kingdom was forced out in 1992 when the value of the pound sterling fell below ERM limits—realignments became less frequent over time as monetary policies and inflation rates converged.

The idea of a common currency slowly gained traction, but it was not until the Maastricht Treaty of 1992 that the Economic and Monetary Union, and with it a common currency and monetary policy, truly began to take shape. While creation of a single currency was rooted in Europe’s integration and facilitating economic transactions within the union, it also helped place the unified Germany that emerged at the end of the Cold War solidly within a common European institutional framework.

The Maastricht Treaty established convergence criteria designed to ensure that countries joining the new common currency would be sufficiently similar to be well served by a single monetary policy. It also gave market forces a significant role in disciplining member states, by establishing the “no bailout” clause. To dispel skepticism and preserve fiscal discipline after the common currency was introduced, member countries signed the Stability and Growth Pact in 1997, which was designed to tie policies to fiscal balance and debt targets.

In sum, the euro’s architecture was built on the premise that market forces, combined with minimal coordination of policies, would suffice to align economies, discipline fiscal policies, and allow countries to withstand idiosyncratic shocks.

Global crisis becomes European debt crisis

The global financial crisis after the collapse of Lehman Brothers in September 2008 triggered the euro area’s sovereign debt crisis. The crisis exposed severe imbalances in the euro area and weaknesses in the European architecture.

Following the introduction of the euro in 1999, many countries—among them Greece, Ireland, Italy, Portugal, and Spain—experienced a dramatic decline in borrowing costs, for both the private and public sectors. In many cases, cheap credit—often fed by capital from banks in the euro area’s core—fueled a credit boom that led to high growth rates, which in turn attracted more capital and investment. But it also increased the indebtedness of households and firms, and investment was concentrated in the nontradables sector (for example, real estate), while high wages eroded external competitiveness. Current account balances deteriorated sharply, and countries accumulated large foreign debt. Misled by the belief that the increase in income was permanent, governments expanded.

Converging interest rates masked an absence of underlying structural convergence. Cross-border financial flows—stimulated by the absence of cross-border transaction costs and financial regulation—facilitated increasing disparities in competitiveness. But when the credit cycle turned, a sudden stop in private capital flows left a number of euro area countries on the brink, their banks laden with bad debt from overinvestment and with large exposures to weakening sovereign debt. Not only had markets not recognized emerging risks, the Stability and Growth Pact had been weakened—a number of members, including some core countries, exceeded its limits, undermining its credibility, and failed to instill sufficient fiscal discipline.

The highly integrated European financial system lacked circuit breakers and common supervision at the onset of the euro area crisis, and was thus highly susceptible to contagion. Country-specific economic and financial shocks spread quickly throughout the region, threatening the viability of the currency union.

Crisis response

National governments began implementing challenging macroeconomic adjustment programs, with the overarching goals of reducing fiscal deficits and improving the competitiveness of their economies—unwinding the imbalances that had grown in previous years and laying the basis for more sustainable long-term growth. European policymakers realized that the European Union had yet to develop the institutional and financial capacity to support crisis economies, prompting cooperation with the IMF (see Box 2). The European Union had to reconsider its “no bailout” principle, and it extended support to sovereigns priced out of the market.

Box 2. The IMF and Europe

This remarkable journey of European integration has had the IMF as a partner all along.

Surprising as it may sound now, many of the earlier IMF program engagements were with the currently “advanced” European economies. The list of early IMF arrangements features countries such as Belgium, France, Italy, the Netherlands, Portugal, Spain, and the United Kingdom. Italy and the United Kingdom were the last G7 economies to have IMF-supported programs, as late as 1977.

IMF involvement in the region escalated with the historic transformation in eastern Europe. The fall of the Berlin Wall opened the floodgates. The challenges of economic stabilization—combating output collapses and in some cases hyperinflation as well as establishing new institutions—underpinned IMF programs in many transition economies, with momentous structural reforms helping countries move from communist to market-based frameworks.

The next wave of programs came at the onset of the global financial crisis. The lull of the late 2000s was interrupted by devastating effects on emerging Europe from disruptions in advanced economies. Ukraine, Hungary, and Iceland were the first, each putting IMF-supported programs in place in November 2008. Others followed suit, and with the crisis spreading to euro area countries as well, Greece, Ireland, and Portugal requested programs in 2010 and early 2011.

This latest round typifies the changes in IMF engagement with countries. For instance, Poland, with its very sound economic fundamentals, benefited from a new insurance-like credit line. But most other countries, commensurate with their higher needs, also benefited from greatly increased loan amounts, as well as efforts to focus conditionality on key macroeconomic priorities.

A more forceful response would have been preferable to the numerous false starts and solutions that often seemed just enough to keep the currency area intact, yet insufficient for a decisive break. But much has still been achieved. A permanent financial support facility for euro area member states—the European Stability Mechanism—was set up. At the height of the crisis, the European Central Bank stepped up to defend the euro area’s integrity with large liquidity support for banks (longer-term refinancing operations) and by establishing a framework for so-called Outright Monetary Transactions.

Most critically, the crisis made clear the need for a pan-European approach to the banking system—the banking union—with efforts now under way (see “Tectonic Shifts” in this issue of F&D). The ultimate objective is to help reduce financial fragmentation and sever the negative feedback loops between banks and sovereigns. The European Union has also taken important steps to strengthen fiscal and economic governance, to detect—and ultimately avoid—a renewed emergence of excessive fiscal and external imbalances.

At critical moments, Europeans have answered with more integration and more solidarity.

The global financial crisis and its reverberations in the euro area also presented formidable challenges for emerging Europe. Financial markets froze and issuing sovereign international bonds became next to impossible. Capital flows retreated, even those channeled through subsidiaries of western banks. As western parent banks faced capital and liquidity shortages, fragilities of an interconnected system came to the fore and subsidiaries in these countries entered a period of deleveraging that has yet to end.

With plummeting exports and domestic demand, output in most countries declined sharply, generating a deeper recession in emerging Europe than in other emerging market regions. Only a few countries escaped—either because their precrisis boom was more contained, leaving room for countercyclical policies, or because their trade and financial interconnectedness was limited.

Countries adopted a range of policies to respond to the crisis, which shocked their economies beyond the most pessimistic expectations. The initial goal was to stabilize the financial sector: countries relaxed reserve requirements, increased deposit coverage, and, in some cases, intervened directly in individual distressed financial institutions.

With large stocks of private debt, mostly denominated in foreign currency, there were few monetary and exchange rate options. Nor was fiscal expansion an option for most in the region as recession took its toll on government finances. Not surprisingly, a number of countries turned to financial assistance from the IMF. IMF lending, often front-loaded and supporting economic programs designed in conjunction with country authorities and European institutions, has provided support to help smooth the needed policy adjustment in 13 countries in the region since the onset of the crisis.

The journey continues

The nascent economic recovery in the euro area risks creating complacency—a wrong-headed belief that the crisis is over and integration efforts can be relaxed.

Far-reaching decisions have been made, but the economic integration of the euro area remains incomplete. Financial markets are fragmented (low European Central Bank interest rates are not spreading throughout the euro area, and firms in countries under pressure often face high borrowing rates), competitiveness gaps remain large, structural rigidities hinder labor and product market integration, and fiscal and other policy coordination have a long way to go.

The task is not just to overcome the crisis and repair the damage, however daunting that may be with output and investment still below precrisis levels and unemployment still unacceptably high in most euro area countries. The even greater challenge is to build a more robust euro area that is able to withstand future shocks and where country-specific shocks cannot easily become systemic.

Solving the crisis calls for a reassessment of the economic and financial architecture underpinning the euro area. The common approach to the area’s banks—as embodied in the vision of a strong banking union—rightly suggests the need for more integration, stronger institutions at the center, and more emphasis on understanding spillovers.

The crisis and its response also mark a departure from some principles in the Maastricht Treaty, including the “no bailout” clause, and have led to a new understanding of national sovereignty in the context of common policies. Designing a union that builds on these new realities will be challenging. Among the most difficult decisions will be finding a political consensus that strikes the right balance between national sovereignty and the role of a strengthened center and policies that serve the greater good. A political framework will be needed to support the necessary economic integration.

Strengthening the monetary union is critical to reviving cross-border capital flows and restoring the effectiveness of monetary policy across the euro area. The banking union is a key part of this process, and the establishment of a Single Supervisory Mechanism is an important step toward a common approach to a healthy banking system. The ongoing Balance Sheet Assessment, which will provide a clear picture of where most banks stand, can help reduce uncertainty about the riskiness of banks. The recent agreement on a Single Resolution Mechanism and a Single Resolution Fund are additional steps toward a fuller union better equipped to deal with banks in trouble, though their complex structure and a cumbersome decision-making process could hamper effectiveness. In the future, an effective common financial backstop will be necessary to address links between sovereigns and banks seen during this crisis (indebted governments struggled to cover banking sector costs, which, coupled with banks holding government debt, undermined confidence in both sovereigns and banks).

Deeper fiscal integration in the euro area can correct weaknesses in the system’s architecture, make the area more resilient to future crises, and provide long-term credibility to crisis-response measures already adopted. Better oversight of national policies and enforcement of rules is under way and will help reinstate fiscal and market discipline. Stronger governance is also a prerequisite for greater sharing of fiscal risks ahead of time; progress is still needed on this front, and is important to reduce the need for costly support after a crisis strikes. Minimal fiscal risk sharing—by increasing cross-country fiscal insurance mechanisms—is also a precondition to reinstate market discipline, adding credibility to no-bailout arrangements.

Long-standing labor and product market rigidities continue to hamper relative price adjustment and competitiveness, especially in the countries that have been under pressure recently. There has been some progress—notably labor market reforms in Spain and Portugal—but much more must be done. A renewed push to improve productivity by implementing the EU Services Directive—which would facilitate cross-border provision of services similar to the current free movement of goods—will help. Providing support for credit to small and medium-sized enterprises and a new round of free trade agreements would also spur growth. Such efforts would lead to a more balanced and sustainable growth path, helping to reduce euro area imbalances.

In emerging Europe, most of the precrisis growth resulted from fast and furious capital inflows that fueled credit expansion, largely benefiting the nontradables sector. The region now faces a very different reality as western parent banks continue to reduce their exposure and the unwinding of ultraloose monetary policy in advanced economies threatens prospects for capital inflows. The region also faces a smaller labor supply with the decline in the working-age population set to accelerate in coming years.

With a modest outlook for capital inflows and labor force participation, the region’s growth opportunities depend on improving productivity through structural reforms. For some, this requires sustained pursuit of labor market reforms: greater flexibility in wage determination, reducing disparities between standard and temporary contracts, and complementary reforms in social benefits. For others, improving the business environment and completing privatization are important to attract foreign investment in the tradables sector and improve links with supply chains in Europe. And yet for others—which already have a competitive export sector and well-established links with regional supply chains—the challenge is to move up the value ladder by improving the skills of their workers.

While the recent crisis in Europe differs from previous challenges in its nature and calls for far-reaching actions, a look back reminds us of the momentous hurdles Europe has surmounted in the past, as well as the approach it has taken in those trying times: greater integration. If political will can once again be summoned, further integration coupled with steps to boost growth can create a more durable foundation for prosperity in the region.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org