To Pay the Piper

Finance & Development, December 2015, Vol. 52, No. 4

Luis A.V. Catão and Rui C. Mano

Countries face a far higher interest rate premium for defaulting on their sovereign debts than previous wisdom suggested

Think of a government that defaults on its debt to foreign investors and, a few years later, negotiates a reduction of the original debt and is about to resume borrowing from capital markets. It faces a number of questions. Should it expect to be penalized for the default and pay an interest rate on new borrowing that is higher than justified by the fundamental state of its economy? If so, how large will such a “default premium” be? And how long will it take for that country to reestablish its creditworthiness and eliminate this default premium?

These are important questions for several reasons. The size and persistence of any default premium determines the debt service burden the country will carry into the future. The premium may also affect any adjustment programs a defaulting country might undertake with multilateral institutions like the IMF to enable it to stay afloat after losing market access. If the default premium is high and persistent, it may take time for the country to reduce reliance on multilateral loans. And if the default premium lasts a long time, it suggests that investors do not easily forget the debt they forgave.

However, whether defaulting sovereigns actually pay a nontrivial interest rate premium has been long debated. With the greater availability of historical data starting in the 1980s a few researchers tried to answer the question empirically. Much of that research suggests that countries either pay a relatively trivial premium for defaulting on their debts or one that is short-lived. For instance, papers by Eichengreen and Portes (1986), Lindert and Morton (1989), and Ozler (1993), among others, found only tiny differences in the interest rate paid by countries that defaulted in the 1930s and those that did not—no more than 25 to 30 basis points (one basis point is 1/100th of 1 percent). In contrast, studies that relied entirely on emerging market data from the 1990s and 2000s (such as Borensztein and Panizza, 2009) found large interest rate premiums of up to 400 basis points on average when countries started to borrow again in private markets, but also found that the premiums virtually disappeared within two years. Only in a few cases in which losses imposed on creditors (so-called haircuts) were exceptionally large did premiums persist (Cruces and Trebesch, 2013).

Still, most governments seem to go out of their way to avoid defaults, which seems incongruous if the penalty is relatively trivial for failing to repay borrowing on the original terms. Clearly, there are other potential risks to defaulting besides interest rate premiums—such as international sanctions, disruptions to trade financing, and loss of reputation—but many studies contend that these other penalties seldom bite hard. Our findings indicate that the general desire to avoid default can be attributed to larger and longer interest rate premiums than previously thought (see Catão and Mano, 2015). So government behavior should not be considered puzzling.

New evidence

Interest rates can be higher than expected based on a country’s fundamentals for many reasons—such as political instability in a borrowing country or bouts of risk aversion in financial markets. But when the premium is solely the result of default history, there are three major factors that should be taken into account to measure correctly the magnitude of such a premium: how to produce a score of a country’s credit history; how to obtain representative data; and how to pick all relevant economic fundamentals—such as the ratio of debt to GDP and economic growth—that could explain a country’s interest rate.

Other researchers have chosen varied measures of credit history, studied disparate time periods, and used different sets of economic fundamentals in their analyses. Estimates of default premiums can be extremely sensitive to these choices. For instance, default premiums may vary across time because of temporary external factors—for example, during 2002–07, when commodity prices were high and risk aversion was low. Likewise, focusing on the less globalized and less liquid world of the 1960s and 1970s—as some earlier studies did—may lead to unrealistically low default premiums. That means that any estimate of the average default premium in a short time period may be biased. Indeed, it is tempting to assume that default premiums simply vanished when sovereign spreads were compressed, even for countries with repeated defaults. But narrow sovereign spreads can be explained by temporary factors (including low risk aversion) and should not be taken as a proxy for the underlying default premium. A proper measure of the default premium requires netting out from the spread the effects of the current country’s fundamentals and of global capital markets; it is very important to control for those factors in any analysis. Finally, a researcher can underestimate the correct size of the default premium by using measures of how investors remember the past that are ad hoc narrow, and do not allow the data to speak more broadly by itself.

We looked at each of these three key ingredients and applied a common methodology across samples. We found more significant default premiums than other researchers because:

- We used a more general measure of credit history that shapes investors’ perception of creditworthiness. We measured the default premium as the sum of three credit history indicators: the total amount of time a country was in default, the years since its last default, and whether the year after debt renegotiation corresponds to the first, second, third, fourth, or fifth year after default. This allows for the possibility that investors’ memories decay quickly in the first years after default and more gradually thereafter.

- We constructed a much broader data set that spans advanced and emerging market countries for two active periods of international bond markets: 1870–1938 and 1970–2011. Our data set expands the historical coverage of existing series on sovereign spreads through research with primary and secondary sources. The new data set comprises 68 countries and has about 3,000 annual observations excluding default years, far more than previous studies.

- We included factors other than credit history that might have affected default premiums. These factors include many macroeconomic fundamentals such as public debt-to-GDP ratio, the share of debt in foreign currency, and GDP growth (amplifying, for example, the historical data in Reinhart and Rogoff, 2009), as well as conditions in global financial markets, such as the volatility of stock prices and benchmark interest rates, that affect investors’ risk appetite and hence leniency toward less creditworthy borrowers. Finally, we included the size of past defaults.

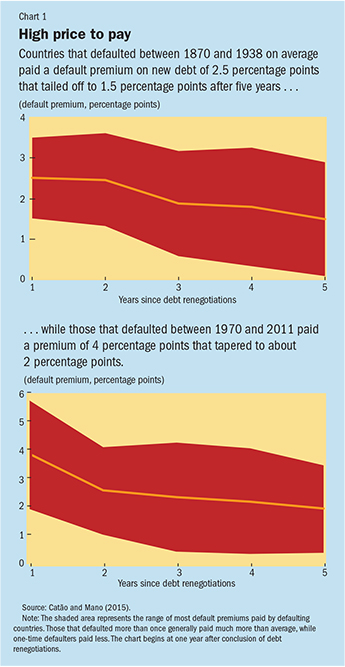

Chart 1 shows default premiums when countries return to private borrowing for 1870–1938 and 1970–2011. For the pre–World War II period, the average initial premium was 250 basis points, much higher than earlier estimates, and it lasted much longer—after five years it still averaged 150 basis points. For the later period the premiums were higher—400 basis points at first and 200 basis points even after five years. The persistence of the premiums is the result of both the years in default and the number of years since default.

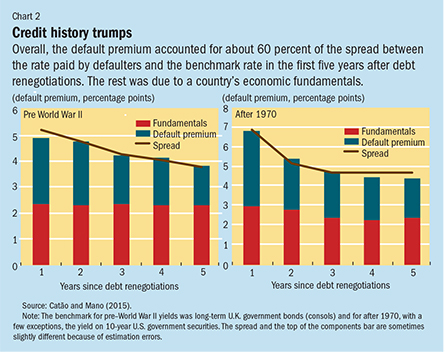

Overall, the default premium accounted for up to 60 percent of the spread between the rate paid by defaulters and the benchmark rate (see Chart 2). That is, much of the overall interest rate paid by a sovereign when it returns to private capital markets is not due to the state of its economy but to its substandard credit history. So the default premium can be of striking importance in gauging the interest charges countries may pay once they fully return to private capital markets.

Serial defaults

Chart 1 indicates that there was a large range of default premiums both above and below the average. That is chiefly due to differences between one-time and serial defaulters. Serial defaulters typically pay a higher-than-average default premium because they stay out of the market accumulating arrears for longer stretches—an effect captured by our credit history indicator measuring time in default. Investors tend to take these “out-of-market” spells—especially if recent—as suggestive of lower creditworthiness, even if standard fundamentals such as debt-to-GDP ratio and economic growth are good. Moreover, the more uncertain lenders are about the accuracy of statistics reported by a defaulting country, the more the lenders tend to focus on government actions such as failure to repay and renegotiation delays, which generally results in a higher expected default premium.

Our credit history indicators do not distinguish between large and small defaults. It might seem logical that because investors suffer bigger losses in some defaults than in others, they would punish larger defaults with larger default premiums.

But establishing the effects of past haircuts on default premiums is difficult. First, all defaults are major events, usually involving a sizable haircut. Second, investors in competitive markets base the price of bonds and loans on future default risk. Past haircuts would matter if lenders consistently decided to recoup their losses by charging an extra premium. But in competitive markets—like the typical sovereign bond market—any attempt to recoup losses is likely to be undercut by new lenders. Moreover, nearly 90 percent of the broad differences in haircuts is explained by variables already included in our model of the default premium—like debt-to-GDP ratio and length of default.

A clear rationale

The bottom line is that the typical interest rate premium for past defaults has been underestimated. This is partly because earlier studies did not take into account sufficient indicators of credit history, and—crucially—their data sets were not comprehensive enough. Looking at a larger number of episodes and longer historical periods than previous researchers did, we found that the sovereign default premium was usually sizable in the first few years after debt renegotiation and that it declined only gradually—certainly more slowly than previous researchers had found.

As a practical spinoff, consider a country with a moderate ratio of debt to GDP of, say, 50 percent, with all of its debt in private hands. At the post-1970 default premium average of 400 basis points, its excess annual payments in interest would amount to 2 percent of GDP after debt renegotiation, tapering to 1 percent of GDP several years later. Even for moderate debt ratios, the interest cost is not trivial—given that interest payments on external debt often range between 1 percent and 3 percent of a country’s GDP. This cost would be higher for more-indebted countries that stayed out of private financial markets for many years. The short of it is that avoiding defaults can be very valuable, even leaving aside other costly risks such as loss of reputation, international sanctions, and disruptions in trade and financial intermediation.

Clearly, the absolute size of a default premium for a country depends on its specific conditions and estimates of how national and global economic factors might evolve. But our analysis demonstrates that a default premium that is close to historical averages would likely be costly enough to justify attempts to avoid default—including the use of austerity measures to get the economy back on track. This is all the more true for governments that are highly indebted and have a history of default and long spells away from private capital markets. ■

Luis A.V. Catão is a Senior Economist in the IMF’s Research Department and Rui C. Mano is an Economist in the IMF’s Asia and Pacific Department.

References

Borensztein, Eduardo, and Ugo Panizza, 2009, “The Costs of Sovereign Default,” IMF Staff Papers 56(4), pp. 683–741 (Washington).

Catão, Luis A.V., and Rui C. Mano, 2015, “Default Premium,” IMF Working Paper 15/167 (Washington: International Monetary Fund).

Cruces, Juan, and Christoph Trebesch, 2013, “Sovereign Defaults: The Price of Haircuts,” American Economic Journal: Macroeconomics, Vol. 5, No. 3, pp. 85–117.

Eichengreen, Barry, and Richard Portes, 1986, “Debt and Default in the 1930s: Causes and Consequences,” European Economic Review, Vol. 30, No. 3, pp. 599–640.

Lindert, Peter H., and Peter J. Morton, 1989, “How Sovereign Debt Has Worked,” in Developing Country Debt and Economic Performance, Vol. 1, ed. by Jeffrey Sachs (Cambridge, Massachusetts: National Bureau of Economic Research).

Ozler, Sule, 1993, “Have Commercial Banks Ignored History?” American Economic Review, Vol. 83, No. 3, pp. 608–20.

Reinhart, Carmen, and Kenneth Rogoff, 2009, This Time Is Different: Eight Centuries of Financial Folly (Princeton, New Jersey: Princeton University Press).

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org