Investment Renaissance

Finance & Development, December 2015, Vol. 52, No. 4

Wenjie Chen, David Dollar, and Heiwai Tang

China is important to the increasing foreign investment in Africa, but its role is far from dominant

Africa’s economic growth has accelerated over the past 15 years and the continent has been receiving significantly more foreign direct investment than in the past. Each development almost certainly plays a role in causing the other.

African economies on average have improved their institutions and policies—changes that not only make for productive and enhanced growth, but also attract more domestic and foreign investment. At the same time there is evidence that foreign direct investment, which involves an ownership stake in an enterprise, has spillover benefits on the recipient economy providing technology, management, and connection to global value chains that should speed economic growth in Africa.

The acceleration of African growth is important because increased growth in the past decade has led to the best progress on poverty reduction on the continent since before 1990. Between 1990 and 2002 the poverty rate in sub-Saharan Africa was flat at 57 percent of the population (living below the World Bank’s $1.25 a day poverty line). But between 2002 and 2011 poverty dropped 10 percentage points. Continued sustained growth is needed to bring poverty down further, and a steady flow of foreign direct investment can help meet that objective.

Recently much attention has been paid to one part of this investment renaissance: Chinese direct investment in Africa. China has become Africa’s main trading partner and Chinese demand has increased Africa’s export volume and earnings. Many observers assume that China has also become the dominant investor in Africa. Indeed, there have been some high-profile, large natural resource investments, including some in countries that have a poor track record of governance—such as Sinopec’s oil and gas acquisition in Angola, the Sicomines iron mine in the Democratic Republic of the Congo, and Chinalco’s mining investment in Guinea. But in fact, although China is an important investor in Africa, and is likely to remain so, it is far from dominant—whether in the resource or other sectors. Moreover, exactly what the recent slowdown in Chinese growth portends for Africa is unclear.

Our research looks beyond the big state-enterprise deals, like the splashy ones mentioned above, to understand the reality of Chinese investment, especially private investment, in Africa. Chinese investment has the potential to become very significant in Africa, partly because the demographics of China and Africa are going in different directions.

Labor force growth

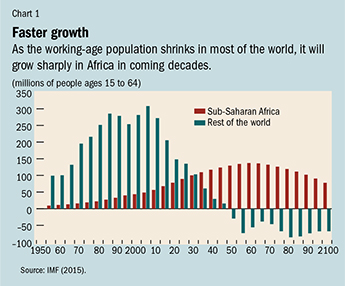

China has been through a period of rapid labor force growth in which it needed to generate 20 million jobs a year. However, that phase is over. The Chinese working-age (15–64) population has started to decline, as it has in most advanced economies. In sub-Saharan Africa, on the other hand, by 2035 the number of people reaching working age will exceed that of the rest of the world combined (IMF, 2015; see Chart 1). Africa and south Asia will be the main sources of labor force growth in the global economy, as workforces elsewhere shrink. That means there is great potential for mutual benefit from foreign investment that flows from the aging economies such as China to younger and more dynamic ones in Africa.

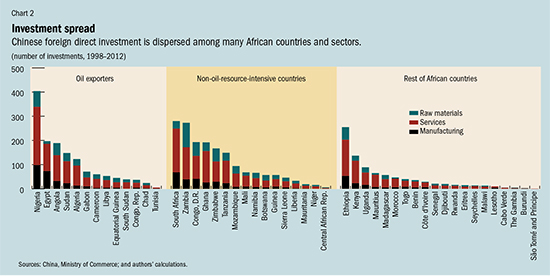

In investigating China’s foreign direct investment (called overseas direct investment by the Chinese), we used firm-level data compiled by China’s Ministry of Commerce. Chinese enterprises that make direct investments abroad are supposed to register with the Ministry of Commerce. The resulting database provides the investing company’s location in China and its line of business. It also includes the country to which the investment is flowing and a description in Chinese of the investment project. However, it does not include the amount of investment. During 1998–2012 about 2,000 Chinese firms invested in 49 African countries. There are about 4,000 investments in the database because firms often have more than one project. The typical investing firm is private and much smaller than the big state-owned enterprises involved in the megadeals that have captured so much attention. Based on the descriptions of the overseas investment, we categorized the projects into 25 industries covering all sectors of the economy—primary, or raw materials operations; secondary, or materials processing; and tertiary, or services. The allocation of the projects across countries and across sectors provides a snapshot of Chinese private investment in Africa.

Some things immediately jump out from the data on the number of investments. The investments are not concentrated in natural resources. The service sector received the most number of investments—such as sales affiliates or operations that provide assistance to construction and transportation. There were also significant investments in manufacturing. Most foreign direct investment is in the service sector both globally and in Africa, so in this sense Chinese investment is typical. Chinese investment is well dispersed in Africa: in resource-rich countries like Nigeria and South Africa, but also in non-resource-rich countries like Ethiopia, Kenya, and Uganda (see Chart 2). Even in resource-rich countries, natural resource projects make up a small portion of individual investments.

We also asked whether factor endowments—such as land, labor, and capital—and other country characteristics influence the number and types of investment projects from Chinese investors. If Chinese investment is similar to profit-oriented investment from other countries, then the number and nature of projects should be related to the factor endowments as well as to other characteristics of the recipient countries. We found that although Chinese foreign direct investment in Africa is less prevalent in sectors that require high-skilled labor, it does tend to gravitate toward those countries with a better-trained workforce, suggesting that Chinese investors aim to exploit the edge these countries have over other countries in the region whose workforces lack the same level of training. We also found that Chinese foreign direct investment is more concentrated in capital-intensive sectors in the more capital-scarce countries, suggesting its importance as a source of external financing for the continent.

Our initial assessment of Chinese investment in Africa looked at the number of investment projects without reference to the size of the investment—which may explain why our findings about the nature of China’s investments did not support the common belief that China is an outsized investor in Africa. But when we looked at investments by size, we also found that China does not dominate foreign direct investment in Africa. Using the Ministry of Commerce’s aggregate data on the stock of Chinese foreign direct investment (that is, the value of the investment in place) in different African countries, we found that at the end of 2011 it was only 3 percent of total foreign direct investment on the continent. Most of the investment came from Western sources. Although that figure may seem small to many people, it is confirmed by other sources. According to the United Nations Conference on Trade and Development (2015) new Chinese foreign direct investment in Africa during 2013–14 was 4.4 percent of the total investment flow—only slightly more than the Chinese share of investment in place. EU countries, led by France and the United Kingdom, are overwhelmingly the largest investors in Africa. The United States is also significant, and even South Africa invests more on the continent than China does.

Moreover, when it comes to the value of investments, China allocates its direct investment in Africa much as other countries do. Chinese and non-Chinese investors are both attracted to larger markets and both are attracted to natural-resource-rich countries. So although most Chinese investments are in services and manufacturing, those tend to be smaller than the typically large-value investments in energy and minerals. Western investment favors these expensive natural resource projects too.

One important difference between expensive investments by China and by Western firms involves governance: Western investment is concentrated in African countries with better property rights and rule of law. Chinese foreign direct investment is indifferent to the property rights/rule of law environment, and its expensive investments tend to favor politically stable countries. This difference makes sense because a significant portion of Chinese investment is tied up in state-to-state resource deals.

China’s slowdown

Analysts have asked whether the recent slowdown in China’s economy, the stock market turbulence in the second quarter of 2015, and the renminbi depreciation in August 2015 may augur a slowdown in Chinese foreign investments.

The underlying issue in China’s economy is that it has relied on exports and investment for too long and is making a difficult transition to a different growth model. Because China is the largest exporter in the world, it is not realistic for its exports to grow much faster than world trade. The recent growth in China’s export volume has been in the low single digits, similar to the growth rate of world trade. There is nothing wrong with China’s competitiveness; it is just facing a slow-growing world market. Depreciation likely would not change the picture much because other developing economies may follow suit.

China’s stimulus package following the global financial crisis of 2008–09 was heavily oriented toward boosting investment and took its investment rate to 50 percent of GDP. That maintained growth for a while, but it has resulted in excess capacity throughout the economy. There are many empty apartments, the capacity utilization rate in heavy industry is low, and there is much underused infrastructure, such as highways in smaller cities and convention centers in cities where there is no demand for them. Because of the excess capacity it is natural for investment to slow and affect the overall growth of the economy. The slowdown in China has had an immediate effect on Africa because it has contributed to declining prices for primary products and declining volumes of exports for African economies.

But the weaker news for the old industrial Chinese economy during the first half of 2015 was matched by some positive news from the new economy. In contrast to industry, the services sectors grew rapidly. Most of the service output is consumed by households, and household income has been rising steadily for the past three decades. Still, the slowdown in investment is bound to have some spillover effect on employment, income, and consumption.

Even though the economic slowdown in China has hurt African exports and export prices, it carries some potential positive news. The deceleration in domestic investment in China means that for the moment China has even more capital to send abroad. Although its consumption rate should gradually rise, for the foreseeable future China is likely to have an excess of savings over investment, which means that it will continue to provide capital to the rest of the world. This can happen in a fairly orderly fashion. The authorities have laid out an ambitious set of reforms that should facilitate the shift from investment-led growth to a model based more on productivity growth and consumption growth. The plans include a number of steps to foster the new model. For example, to allow more labor flexibility, authorities plan to relax rules that tie a household’s government benefits to the region in which the household is registered. They also intend to introduce financial reform to price capital better and allocate it to the most efficient use, and to open up the service sector, which is still largely closed to foreign trade and investment.

A smooth transition should enable China to continue to grow in the 6 to 7 percent range for the next decade. It will not provide increases in demand for energy and minerals on the scale of the past, but it should be a stable source of direct investment for other countries. Africa will have to compete for its share through infrastructure investment, improvements in the investment climate, and strengthening of human capital because, as we found, countries with more human capital attract the more skill-intensive investment from China.

There is, however, a possibility of a more negative outcome. For the first time, Chinese outward investment is exceeding inward investment by a large amount; the slowdown in the domestic economy is part of the reason, as domestic Chinese firms are looking elsewhere for profits. In fact, the net capital outflow from China in 2015 is extraordinary. The IMF’s 2015 Article IV staff report projects a current account surplus of $337 billion. Through September the central bank’s reserves declined by $329 billion. The two numbers together provide a rough estimate of $666 billion in net capital outflows.

If China does not make a smooth transition to a new growth model, it will remain a major source of capital in the short run but it will not grow as well over the medium to long term and thus will not be as important a source of capital. China’s successful rebalancing will be a better outcome for both China and for the rest of the developing world. ■

Wenjie Chen is an Economist in the IMF’s African Department. David Dollar is Senior Fellow in the China Center at the Brookings Institution. Heiwai Tang is Assistant Professor of International Economics at Johns Hopkins University’s School of Advanced International Studies.

This article is based on the August 2015 Brookings Institution Working Paper “Why is China investing in Africa? Evidence from the firm level,” by Wenjie Chen, David Dollar, and Heiwai Tang.

References

International Monetary Fund (IMF), 2015, Regional Economic Outlook: Africa (Washington, April).

United Nations Conference on Trade and Development, 2015, World Investment Report.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org