El Niño Good Boy or Bad?

Finance & Development, March 2016, Vol. 53, No. 1

Paul Cashin, Kamiar Mohaddes, and Mehdi Raissi

El Niño has important effects on the world’s economies—and not all of them are bad

The current El Niño (Spanish for “The Boy”)—a band of above-average ocean surface temperatures that develops every 3 to 7 years off the Pacific coast of South America and lasts about two years—is causing major climatological changes around the world. Climate experts are continuously monitoring the developments of the 2015–16 El Niño, which is one of the most severe events in the past 50 years and, notably, the largest since the 1997–98 episode that shocked global food, water, health, energy, and disaster-response systems.

But what are the macroeconomic effects of an average El Niño event? Economists are increasingly interested in the relationship between climate—temperature, precipitation, storms, and other aspects of the weather—and economic performance, including agricultural production, labor productivity, commodity prices, health, conflict, and economic growth. A thorough understanding of this relationship can help governments design appropriate institutions and macroeconomic policies.

Taking the temperature

In a recent IMF study, we examined variations in weather-related events—with a special focus on El Niño—over time and across different regions to identify their impact on growth, inflation, energy prices, and nonfuel commodity prices, motivated by growing concern about their effects on commodity prices and national macroeconomies. These extreme weather conditions can constrain the supply of rain-driven agricultural commodities, lead to higher food prices and inflation, and may trigger social unrest in commodity-dependent countries that rely primarily on imported food.

Our research—taking into account the economic interlinkages and spillovers between countries—analyzed the macroeconomic transmission of El Niño shocks between 1979 and 2013, both on national economies and internationally, focusing on its effects on real GDP, inflation, and commodity prices.

The results indicate that El Niño has a large but highly varied economic impact across different regions. Australia, Chile, India, Indonesia, Japan, New Zealand, and South Africa face a short-lived fall in economic activity in response to a typical El Niño shock. However, in other parts of the world, an El Niño event actually improves growth, in some countries directly—for instance, in the United States—and in other countries—such as in Europe—indirectly through positive spillovers from major trading partners. Many countries in our sample experienced short-term inflation pressures following an El Niño shock (its magnitude increasing with the share of food in the consumer price index, CPI, basket), while energy and nonfuel commodity prices also rose around the world.

Defining El Niño

In an El Niño year, air pressure drops along the coast of South America and over large areas of the central Pacific. The typical low pressure system in the western Pacific becomes a weak high pressure system, moderating the trade winds and allowing the equatorial countercurrent (which flows west to east) to accumulate warm ocean water along the coastline of Peru. This phenomenon causes the thermocline—a transition layer between warmer mixed water at the ocean’s surface and cooler deep water below—to drop in the eastern part of Pacific Ocean, cutting off the upwelling of cold nutrient-rich ocean water along the coast of Peru.

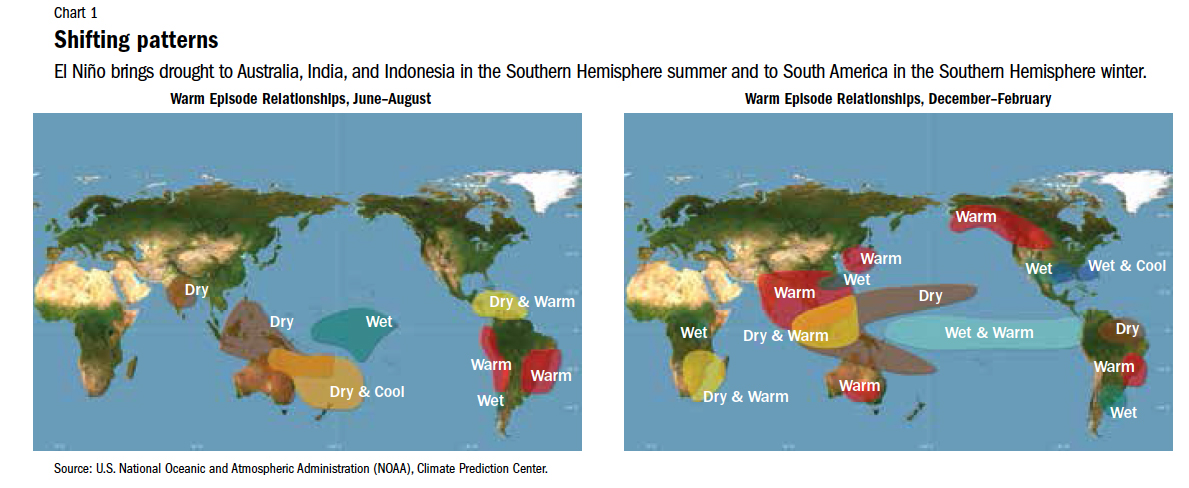

An El Niño typically brings drought to the western Pacific (including Australia), rains to the equatorial coast of South America, and storms and hurricanes to the central Pacific (see Chart 1, which shows the climatological effects across two different seasons). These changes in weather patterns have significant effects on agriculture, fishing, and construction industries, as well as on national and global commodity prices.

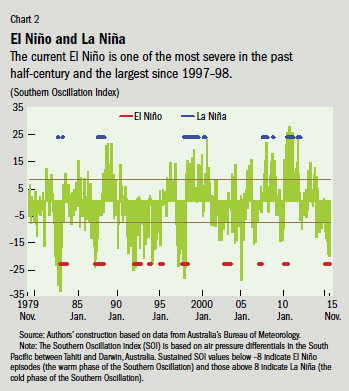

One way to measure El Niño intensity is by using what weather experts call the Southern Oscillation index (SOI), which is based on air pressure differentials in the South Pacific between Tahiti and Darwin, Australia. Sustained SOI values below –8 indicate El Niño episodes (the warm phase of the Southern Oscillation). Likewise, sustained SOI values above 8 indicate the cold phase of the Southern Oscillation, dubbed La Niña. The 1982–83 and 1997–98 El Niño episodes were quite severe and had large adverse macroeconomic effects in many regions of the world, whereas other El Niño events in our sample period were relatively moderate: 1986–88, 1991–92, 1993, 1994–95, 2002–03, 2006–07, and 2009–10 (see Chart 2). The 2015–16 El Niño event has been one of the most severe of the past 50 years and the largest since that in 1997–98.

Climate and the global macroeconomy

We analyzed the international macroeconomic transmission of El Niño shocks, taking into account drivers of economic activity, interlinkages and spillovers between different regions, and the effects of unobserved or observed common factors such as energy and nonfuel commodity prices (see Chudik and Pesaran, 2016; and Cashin, Mohaddes, and Raissi, 2015, for details).

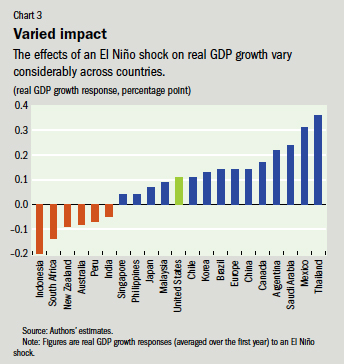

The results show that while Australia, India, Indonesia, New Zealand, Peru, and South Africa face a short-lived fall in economic activity in response to an El Niño shock, other countries, such as Argentina, Canada, Mexico, and the United States may actually benefit (either directly or indirectly through positive spillovers from major trading partners—see Chart 3).

Good boy or bad?

On the negative side, in Australia El Niño causes hot and dry summers in the southeast, increases the frequency and severity of bush fires, reduces wheat export volumes, and drives up global wheat prices, leading to a drop in the country’s real GDP growth. New Zealand also experiences drought in places that are normally dry, and floods elsewhere, thereby lowering agricultural output and real GDP. El Niño conditions usually coincide with a weak monsoon and rising temperatures in India, which hurts its agricultural sector and increases domestic food prices and inflation. El Niño–induced drought in Indonesia is also harmful to that country’s economy and agricultural sector, pushing up world prices for coffee, cocoa, and palm oil. Furthermore, mining equipment in Indonesia relies heavily on hydropower; with deficient rain and low river currents, the world’s top exporter of nickel—used to strengthen steel—is able to produce less of the metal.

El Niño typically brings stormy winters to Chile and raises metal prices by disrupting the supply chain: heavy rain will reduce access to Chile’s mountainous mining region, where large copper deposits lie. Therefore, we would expect an increase in metal prices and lower output growth, which we estimate to be about –0.2 percentage point on impact—with an average effect over the first year that is positive but not statistically significant. South Africa experiences hot and dry summers during an El Niño episode, with adverse effects on its agriculture and real GDP growth. More frequent typhoon strikes and cooler weather during summers are expected for Japan, which could depress consumer spending and growth. Our analysis suggests an initial drop of about 0.1 percentage point in Japanese output growth. However, the construction sector experiences a boost following typhoons, which can partly explain the increase in growth after an initial decline.

On the other hand, in the United States, El Niño typically brings wet weather to California (benefiting lime, almond, and avocado crops, among others), warmer winters in the Northeast, increased rainfall in the South, diminished tornado activity in the Midwest, and a decrease in the number of hurricanes that hit the east coast, all of which leads overall to higher real GDP growth. Plentiful rains can help boost soybean production in Argentina, which exports 95 percent of the soybeans it produces. Canada enjoys warmer weather in an El Niño year, and in turn a greater return from its fisheries. In addition, the increase in oil prices means larger oil revenues for Canada, which is the world’s fifth-largest oil producer (averaging 3,856 million barrels a day in 2012). For Mexico we observe fewer hurricanes on the east coast and more hurricanes on the west coast, which generally brings stability to the oil sector and boosts exports. Although El Niño is associated with dry weather in northern China and wet weather in southern China, we do not observe any direct positive or negative effects on China’s output growth. Moreover, a number of economies—in Europe, for example—that are not directly affected by El Niño do benefit from the shock, mainly due to positive indirect spillovers from commercial trade and financial market links.

Although there are both winning and losing countries from an El Niño event, in the aggregate the detrimental effects on losing countries more or less balance out the positive effects on winning countries.

Commodity prices and inflation

The El Niño weather phenomenon can also significantly affect global commodity prices. The higher temperatures and droughts following an El Niño event, particularly in Asia and the Pacific, not only increases the prices of nonfuel commodities (by about 5½ percent over a year), but also boosts demand for coal and crude oil as lower output is generated from hydroelectric power plants, thereby driving up their prices.

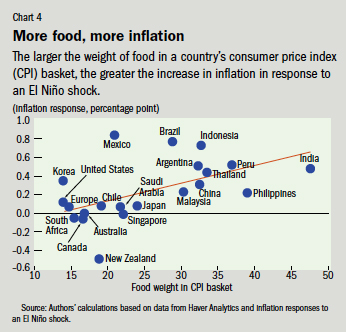

Generally—but not always—El Niño events tend to be inflationary, with the impact on our sample of countries ranging between 0.1 and 1 percentage point. This reflects mainly higher fuel and nonfuel commodity prices, but is also a result of government policies such as holding buffer stocks of grain, persistent inflation expectations, and strong domestic demand in countries whose growth picks up following an El Niño episode. The largest increases in inflation in Asia are observed in India, Indonesia, and Thailand, probably due to the high weight of food in the CPI basket of these countries—47.6 percent, 32.7 percent, and 33.5 percent, respectively. We investigated this hypothesis by looking at the weight of food in the CPI basket of the 21 countries and regions and their inflation responses and found a clear positive relationship between food share and increased inflation (see Chart 4).

Because growth, inflation, and commodity prices are sensitive to El Niño developments, governments should take into consideration the likelihood and effects of El Niño episodes when formulating macroeconomic policy, and implement policies that could help ameliorate the adverse effects of such shocks. For example, in India changing cropping patterns and sowing quicker-maturing crop varieties, rainwater conservation, judicious release of food grain stocks, and changes in import policies and quantities would help bolster agricultural production in low-rainfall El Niño years. On the macroeconomic policy side, governments should continue to closely monitor any upticks in inflation arising from El Niño shocks—and alter their monetary policy stance appropriately—to avert second-round inflation effects. And in the longer term, investment in the agricultural sector, mainly in irrigation, as well as building more efficient food value chains, would serve as valuable insurance against future El Niño episodes. ■

Paul Cashin is an Assistant Director and Mehdi Raissi is an Economist, both in the IMF’s Asia and Pacific Department; Kamiar Mohaddes is Senior Lecturer and Fellow in Economics at Girton College, University of Cambridge.

This article is based on the 2015 IMF Working Paper 15/89, “Fair Weather or Foul? The Macroeconomic Effects of El Niño,” by Paul Cashin, Kamiar Mohaddes, and Mehdi Raissi.

Reference

Chudik, Alexander, and M. Hashem Pesaran, 2016, “Theory and Practice of GVAR Modeling,” Journal of Economic Surveys, Vol. 30, No. 1, pp. 165–97.

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org