Trade Turbulence

Finance & Development, March 2016, Vol. 53, No. 1

Cristina Constantinescu, Aaditya Mattoo, and Michele Ruta

China’s transition to a new growth path is contributing to trade volatility today and will shape trade opportunities tomorrow

Global trade has been a puzzle lately. In the 2000s, and especially after the Great Recession, trade growth has been persistently sluggish relative to GDP. And 2015 appears to have added a new dimension: volatility. Available data indicate that global trade contracted sharply in the first half of the year before beginning to grow again, albeit slowly.

In a previous article (“Slow Trade,” in the December 2014 F&D), we examined the cyclical and structural factors behind the global trade slowdown: weak demand, maturing value chains, and slower trade liberalization than in the 1990s. These forces are all still at work and contributed to the weak growth of world trade in 2015.

The trade fluctuations in 2015 may reflect turbulence as China adjusts to a new, slower growth path that is less dependent on investment and industrial production. China’s transition has strikingly different implications for countries depending on their main exports. Some of these effects are temporary; others are more structural. Manufacturers (especially in east Asia) suffered significant declines in export quantities but are now recovering; commodity producers were hurt primarily by lower export prices, which persist; and services exporters have benefited in a way that could presage future opportunities.

A most peculiar year

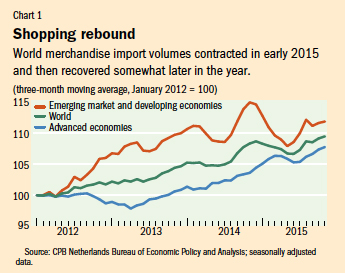

After a period of low but fairly consistent trade growth, preliminary data for 2015 show a sudden contraction in trade volume of about 3 percent quarter over quarter in the first half of the year (see Chart 1). In the third quarter of 2015, growth appears to be positive again but weaker than in the second half of 2014. The contraction and partial rebound were concentrated in emerging market economies.

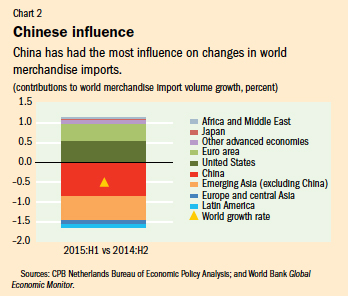

Emerging Asia, which accounts for more than a quarter of world trade, seems to have been the epicenter of the 2015 trade downturn and incipient rebound. According to preliminary figures, in the first half of 2015 emerging Asia’s imports dropped by 10 percent, accounting for nearly 90 percent of the contraction in world import volumes. China alone saw a contraction in import volumes of 15 percent and was responsible for more than half of the contraction in world imports (see Chart 2). The reversal of these trends in the region in the third quarter is contributing to the rebound that we observe in world trade, although trade growth in 2015 was still weaker than in 2014. Developments in other regions also matter. In particular, lower imports from crisis-stricken commodity exporters such as Brazil and Russia—in part reflecting lower demand in China, as discussed below—have contributed to falling global imports.

Napoleon’s prophecy

Napoleon is reputed to have said, “When China wakes, the world will shake.” Indeed, short-term macroeconomic fluctuations as China’s economy shifts from investment and manufacturing to consumption and services are affecting the pattern of production and trade in east Asia and beyond. These changes are manifested in manufacturing, commodities, and services trade.

On the production side, the slowdown in GDP has been concentrated in the industrial sector, which depends more on imported inputs than do other sectors of the economy; imported inputs make up 11.5 percent of total inputs in the industrial sector and only about 6 percent in other sectors. On the demand side, the slowdown is more significant in investment, which has greater, though declining, import intensity than other components of total demand. The import intensity of China’s investment is more than 50 percent higher than that of its consumption. Investment-related imports account for almost 60 percent of China’s total imports, and for 11 percent of the world’s investment-related imports (second only to the United States).

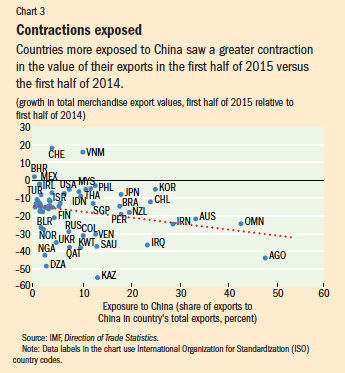

The contraction in China’s imports was distributed across all the regions of the world. Countries more exposed to China, as measured by that country’s share in their total exports, tended to see a greater contraction in the value of their exports in the first half of 2015 than in the corresponding period in 2014 (see Chart 3). Bilateral trade data for the third quarter are not yet available. A 1 percent higher exposure to China meant a 0.3 percent greater contraction in the growth of value of a country’s exports. The reduction in value of exports was attributable to lower prices and lower quantities, varying across regions depending on the composition of their exports. The slower growth in imports from large commodity exporters, such as those in the Middle East and sub-Saharan Africa, reflects the recent drop in prices; the sizable contraction in imports from emerging Asia, especially in the first quarter of 2015, resulted largely from lower quantities.

Magnifying chains

The impact on manufacturing was most visible in east Asia, which experienced a regional trade collapse. China is an important ultimate destination for the value-added exports of other Asian countries. Data available for five countries in east and south Asia indicate that about 50 percent of gross exports of these countries to China constitute value added that is ultimately absorbed in China, and therefore fully dependent on Chinese demand. Another 20 percent of regional exports are reexported by China and consumed in third countries, and therefore not dependent on China’s demand. The remainder constitutes foreign value added in a particular country’s gross exports to China, which originates elsewhere in the region and beyond.

The impact of macroeconomic changes in China may have been magnified by changes in the composition of economic activity. Production shifted away from sectors that are associated with global value chains—that is, from industrial production to services and, within industrial production, from capital goods (equipment and machinery) to consumption goods. Given the extensive network of supply chains in east Asia, this magnification effect likely affected intraregional trade flows more than interregional trade.

In the longer term, the recovery of global trade will, on one hand, be limited by diminished growth in demand in China; on the other hand, it will be boosted by the relocation of production away from China toward other lower-cost economies. Rebalancing from investment to consumption is likely to create opportunities for exporters of final goods and may also eventually boost upstream intermediate and capital goods sectors that are now adversely affected.

Nominal troubles and real opportunities

Commodity exporters saw no decline in export volumes. Exporters in Africa, the Middle East, eastern Europe and central Asia, and Latin America did experience lower trade values, but that was largely because of falling commodity prices—that is, a nominal rather than a real contraction. This evidence suggests primarily a price response to expectations of diminished demand for commodities and enhanced supply in sectors like oil and gas. Nevertheless, deterioration in the terms of trade for commodity producers has hurt real incomes for that group and contributed to recessions in countries such as Brazil and Russia, leading to a further contraction in commodity exporters’ import volumes.

Africa and the Middle East are emblematic of these nominal troubles. Having experienced the deepest plunge in export values since mid-2014, Africa and the Middle East contributed significantly to the recent decline in world trade values. Mostly a nominal phenomenon driven by changing prices, the downturn in oil and commodity exports also reflects sluggish volume growth in recent years. China and other emerging Asian economies together account for more than half of the decline in export values of Africa and the Middle East.

The rebalancing of the economy from investment to consumption is also shifting China’s demand from goods to services. Some of this demand is being served by cross-border imports and consumption abroad—whose growth is already visible. Available data indeed show the different dynamics of goods and services imports in recent years, with slowing imports of goods and rising imports of services, especially travel (see Chart 4). The latter may reflect consumption abroad of services ranging from tourism to education and health. But it is also possible that these data capture other short-term factors such as disguised or illegal capital outflows.

Services imports are growing, but trade in goods still dominates. The net effect is influenced largely by the decline in imports of goods, because services were a relatively small share of total imports of China in 2014. But the share of services has grown—from about 15 percent at the beginning of 2011 to close to 22 percent in the first half of 2015.

Mind the transition

Looking ahead, the rebalancing of the Chinese economy will unquestionably influence trends in world trade. But how the transition is managed will affect how much global trade fluctuates in the coming years.

Diminished growth in China, as well as the national shift in emphasis from investment to consumption, is affecting manufacturing and commodity exporters. The changing composition of demand is likely to favor exporters of consumption goods and eventually of upstream intermediate and capital goods used in their production. In the longer term, rising wages in China may also encourage industrial production and exports in lower-cost economies, and in turn enhance demand for commodities. Finally, the rebalancing is also shifting China’s demand from goods to services, and these imports may grow even faster if services markets continue to open up. ■

Cristina Constantinescu is an Economist and Michele Ruta is a Lead Economist, both in the Trade & Competitiveness Global Practice of the World Bank, and Aaditya Mattoo is Research Manager, Trade and International Integration, at the World Bank.

This article is based on a World Bank report by the authors, “Global Trade Watch: Spillovers from China’s Rebalancing.”

Write to us

F&D welcomes comments and brief letters, a selection of which are posted under Letters to the Editor. Letters may be edited. Please send your letters to fanddletters@imf.org