عربي, 中文, Español, Français, 日本語, Português, Русский

The COVID-19 crisis is inflicting the most pain on those who are already most vulnerable. This calamity could lead to a significant rise in income inequality. And it could jeopardize development gains, from educational attainment to poverty reduction. New estimates suggest that up to 100 million people worldwide could be pushed into extreme poverty, erasing all gains made in poverty reduction in the past three years.

Policymakers must do everything in their power to promote a more inclusive recovery, one that benefits all segments of society.

That is why policymakers must do everything in their power to promote a more inclusive recovery, one that benefits all segments of society.

Our new research, prepared jointly with the World Bank for the G20, focuses on how to increase people’s access to opportunities, no matter who they are and where they are from. More equitable access to opportunities is associated with stronger and more sustainable growth and higher income gains for the poor. But unlocking the full potential of all individuals is not an easy task.

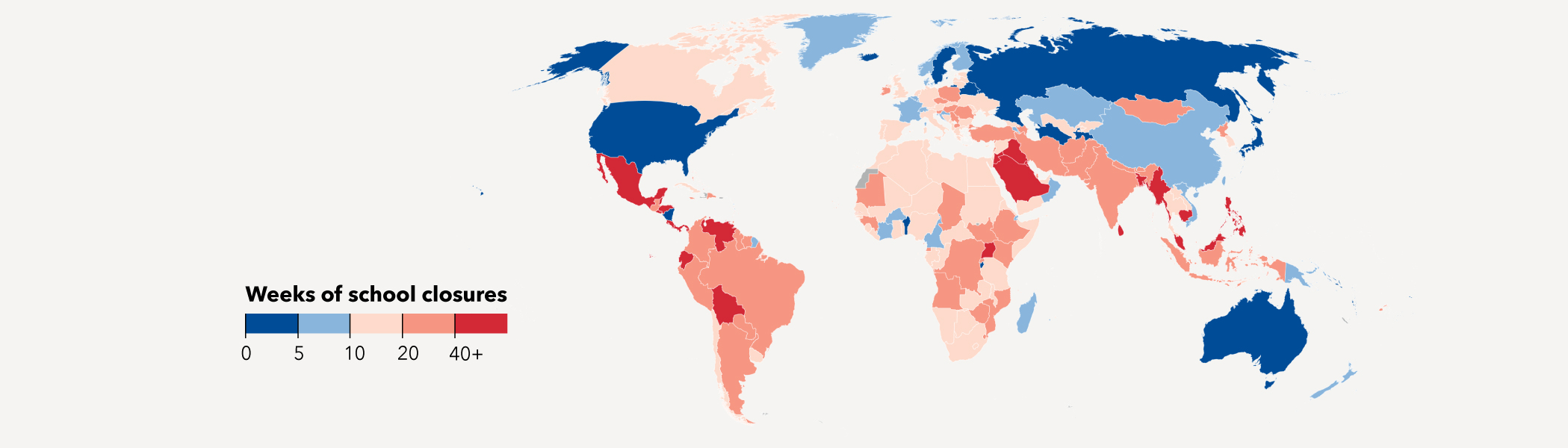

The reality is that low-income households face higher health risks from the virus. They bear the brunt of record-high unemployment and are less likely to benefit from distance learning. Children’s nutrition may also be harmed by the disruption to school-provided meals. According to UN estimates, more than half a billion children worldwide have lost their access to education as a result of coronavirus lockdowns. Many won’t return to the classrooms after the pandemic, with girls more likely than boys to drop out.

These inequalities are truly shocking, but not unexpected. We know from experience and recent IMF analysis that major epidemics often exacerbate pre-existing income inequality.

A policy response like no other

The good news is that governments around the world have deployed extraordinary policy measures to save lives and protect livelihoods. These include extra efforts to protect the poor, with many countries stepping up food aid and targeted cash transfers. Globally, fiscal actions so far amount to about $10 trillion.

But given the severity of the crisis, significant further efforts are essential. This includes taking the measures needed to avoid a scarring of the economy, including from job losses and higher inequality. It is clear that increasing access to opportunities is now more critical than ever if we are to avoid persistent increases in inequality.

With this in mind, I would like to highlight three priorities:

1. Use fiscal stimulus wisely

Substantial fiscal stimulus will have to be deployed during the recovery phase to boost growth and employment. We know from the global financial crisis that countries that experienced larger output losses relative to the pre-crisis trend tended to have higher increases in inequality.

Yet securing a return to growth is not enough. Let’s remember the post-financial crisis reforms and investments that made banking systems more resilient. We will need a similar surge in reforms and investments during the recovery phase to significantly improve the economic prospects of the most vulnerable.

So, we will need a fiscal stimulus that delivers for people. This means scaling up public investment in health care to protect the most vulnerable and minimize the risks from future epidemics. It also means strengthening social safety nets; expanding access to quality education, clean water, and sanitation; and investing in climate-smart infrastructure. Some countries could also expand access to high-quality childcare, which can boost female labor force participation and long-term growth.

These efforts are critical to achieve the Sustainable Development Goals. But how can we significantly scale up spending when so many countries are now facing rising public debt? Public debt in emerging markets has risen to levels not seen in 50 years.

The IMF and the World Bank have championed debt service suspension as a fast-acting measure for countries that lack the financial resources to adequately respond to the crisis. The G20 has responded by agreeing to suspend repayment of official bilateral credit for the poorest countries, from May 1 through the end of 2020.

Over the medium term, there will be room to improve the efficiency of spending and mobilize higher public revenue. There will also be room for tax reform: for example, some advanced and emerging economies could raise their top personal income tax rates without slowing growth. Countries could ensure that the corporate tax system captures an appropriate part of the unusual gains received by the “winners” of the crisis, including perhaps from digital activities. And there should be a concerted effort to combat illicit flows and close tax loopholes, both domestically and internationally.

2. Empower the next generation through education

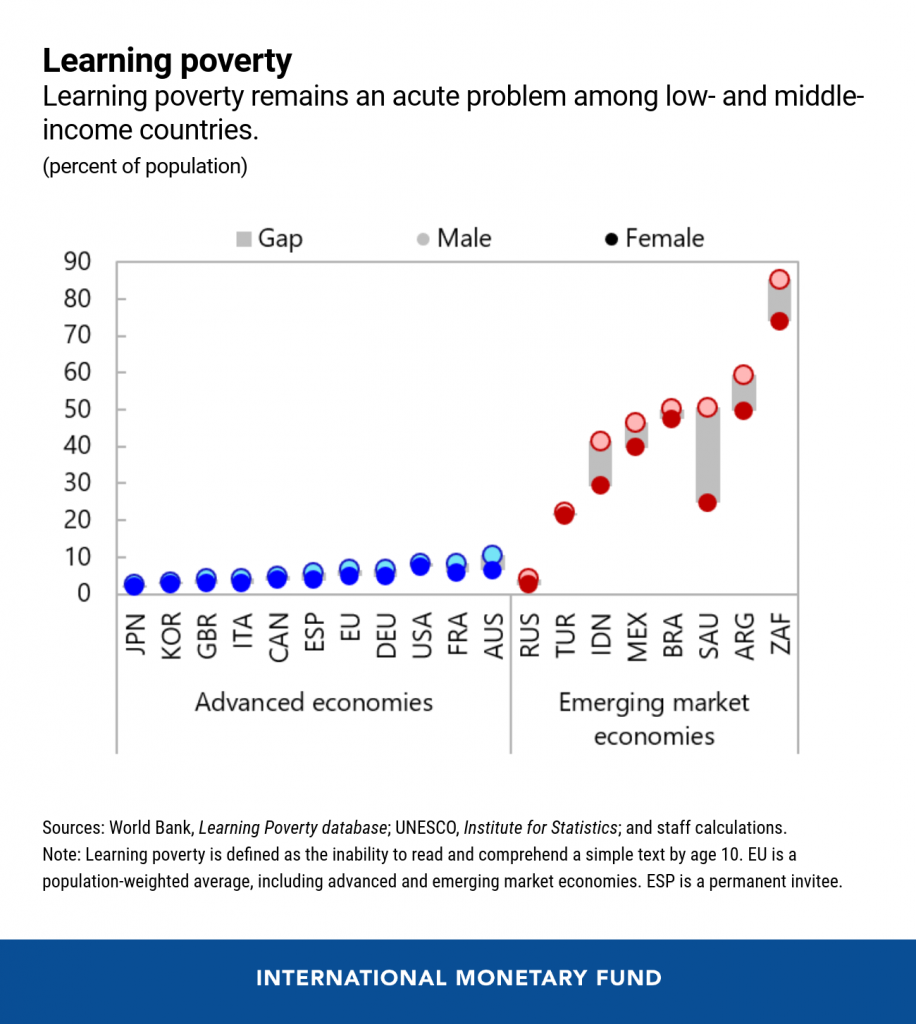

The virus-related disruption to education has left millions of children at risk of “learning poverty,” which means being unable to read and comprehend a simple text by age 10. Driven by poor access to quality schooling, learning poverty is already too high, especially in emerging markets and low-income nations.

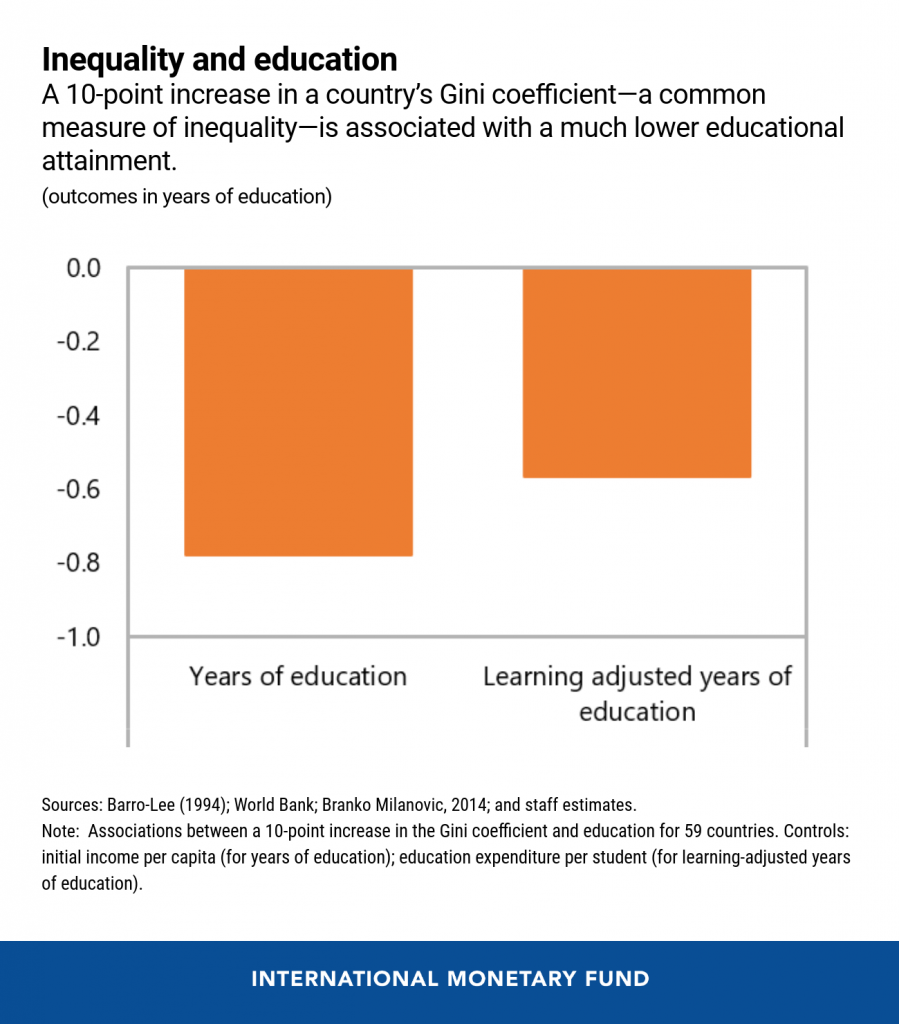

We are also concerned about the long-term effects of the crisis on income and education gaps. In our research, we looked at the link between education and inequality. A 10-point increase in a country’s Gini coefficient (with such increases observed in some economies around the time of the global financial crisis) is associated with significantly lower educational attainment of about half a year. This could reduce lifetime earnings and cause income and opportunity gaps to become persistent across generations.

In other words, safeguarding our future means safeguarding our children. That is why we need more investment in education—not just spending more on schools and distance-learning capacity, but also improving the quality of education and the access to life-long learning and re-skilling.

These efforts can pay large dividends in terms of growth, productivity, and living standards. Simulations, based on a model reflecting an economy like Brazil, show that reducing the educational attainment gap by a quarter, relative to the OECD average, could boost economic output by more than 14 percent.

3. Harness the power of financial technology

COVID-19 has triggered a mass migration from analog to digital. But not everyone has seen the benefits; and the growing digital divide is set to become one of the legacies of the crisis.

What can policymakers do? A key priority must be to broaden the access of low-income households and small businesses to financial products, which will allow households to smooth consumption in the face of shocks and businesses to undertake productive investments. This “inclusion revolution” is now gaining momentum as governments are providing emergency cash transfers in record amounts. For example, in Pakistan and Peru, new support programs cover one-third of the population.

Reaching the most vulnerable can be challenging in developing economies, where nearly 70 percent of employment is informal. But this is where fintech opportunities abound. Think of the fact that about two-thirds of all unbanked adults (1.1 billion people) have a mobile phone, and one-quarter have access to the internet. Moving routine cash payments by governments into accounts could reduce the number of unbanked adults by 100 million globally, and even bigger opportunities exist in the private sector.

Of course, governments also need to manage fintech risks. Reforms are needed to promote competition, enhance consumer protection, and fight money laundering. Finding the right balance will be critical for lower inequality and growth.

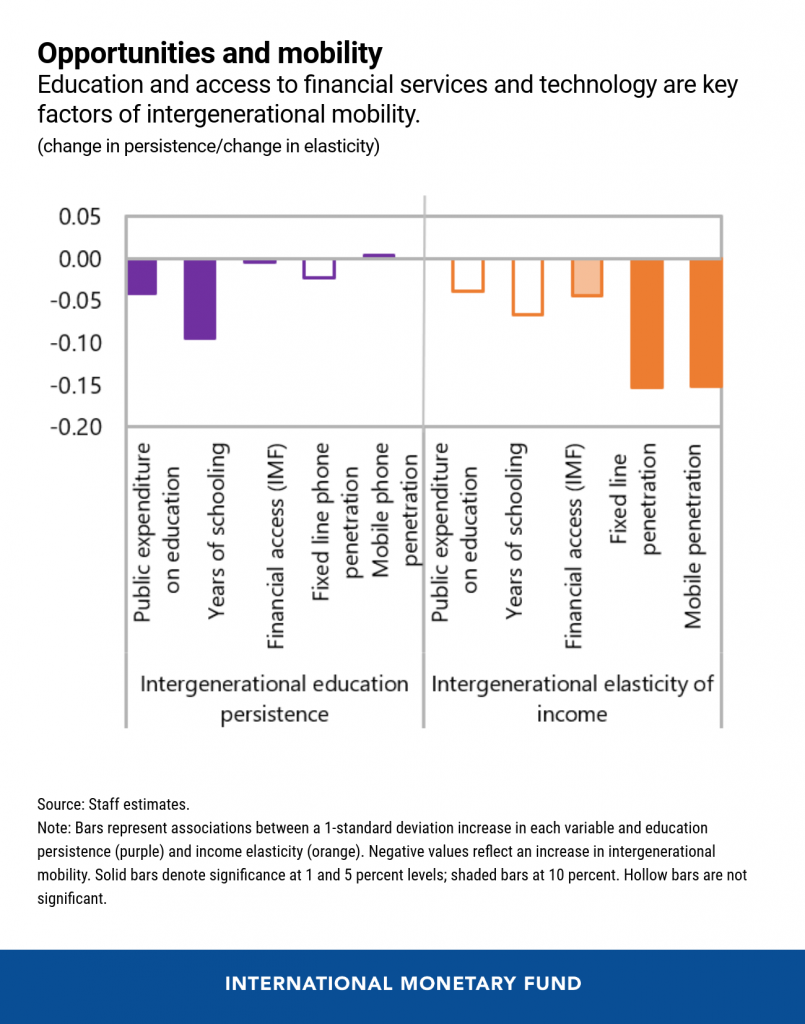

Our research shows that greater access to finance and technology is associated with higher intergenerational income mobility. And we have estimated that there is a 2- to 3-percentage-point GDP growth difference over the long term between financially inclusive countries and their less inclusive peers.

In all these areas, the IMF is working with the World Bank and many other partners to support countries in this time of crisis. We are deeply committed to helping vulnerable groups through our hands-on technical assistance, policy advice, and lending programs. And we have increased our focus on social spending issues, including safety nets, health and education.

As they move forward, all governments will need to gear up for a more inclusive recovery. This means taking the right measures, especially on fiscal stimulus, education, and fintech. And it means sharing ideas, learning from others, and fostering a greater sense of solidarity.

If there is one lesson from this crisis, it’s that our society is only as strong as its weakest member. This should be our compass to a more resilient post-pandemic world.