- Introduction

- Principles

- Practices

- Annex

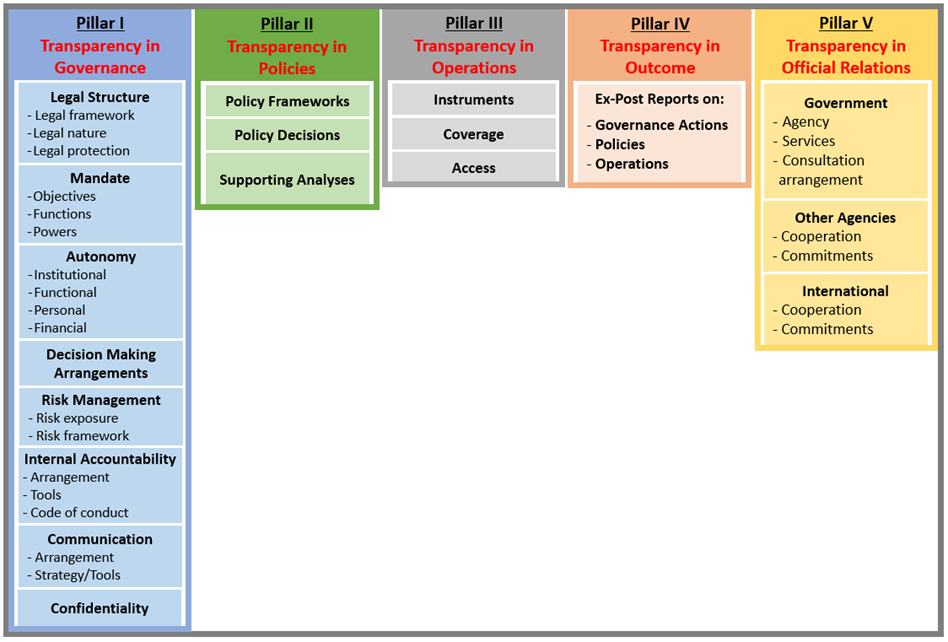

Introduction

Pillar I. Transparency in governance, covering institutional issues.

Pillar II. Transparency in policies, including its framework and decision-making process.

Pillar III. Transparency in operations, highlighting how policy decisions are implemented.

Pillar IV. Transparency in outcome, focusing on how the outcome of central bank policies and other actions are reported to stakeholders to facilitate accountability.

Pillar V. Transparency in official relations, covering central bank interactions with the government and other domestic agencies, and international relations and commitments.

| Figure 1. Central Bank Transparency: Five-Pillar Framework |

|

| Source: IMF Staff |