Statistical Appendix

January 2015

January 2015

Related Links

Email notification sign-up

Regional Economic Outlook Update: Middle East and Central Asia

Learning to Live With Cheaper Oil Amid Weaker Demand

January 2015

A large and possibly persistent decline in oil prices, and slower-than-projected growth in the euro area, China, Japan, and Russia, have substantially altered the economic context for countries in the Middle East and Central Asia. The appropriate policy response will depend on whether a country is an oil exporter or importer. A common theme, however, is that these developments present both an opportunity and an impetus to reform energy subsidies and step up structural reform efforts to support jobs and growth.

Lower oil prices have weakened the external and fiscal balances of oil exporters, including members of the Gulf Cooperation Council (GCC). Large buffers and available financing should allow most oil exporters to avoid sharp cuts in government spending, limiting the impact on near-term growth and financial stability. Oil exporters should prudently treat the oil price decline as largely permanent and adjust their medium-term fiscal consolidation plans so as to prevent major erosion of their buffers and to ensure intergenerational equity.

Gains from lower oil prices provide much-needed breathing space for oil importers but will be offset by a concurrent decline in external demand, particularly from Russia, but also from the euro area and China. Russia’s sharp slowdown and currency depreciation have weakened the outlook for the Caucasus and Central Asia (CCA) because of strong linkages through trade, remittances, and foreign direct investment, suggesting the need for greater exchange rate flexibility and near-term fiscal easing where financing allows, along with stepped-up reform efforts.

Table 1. Real GDP Growth, 2014 and 2015 | ||||||

|

|

|

|

|

| |

| World | U.S. | Euro Area | Emerging Markets | China | Russia | |

| 2014 | 3.3 | 2.4 | 0.9 | 4.4 | 7.4 | 0.6 |

| 2015 | 3.5 | 3.6 | 1.2 | 4.3 | 6.8 | -3.0 |

| 2015 Revision from Oct. 2014 WEO |

-0.3 | 0.5 | -0.2 | -0.6 | -0.3 | -3.5 |

| MENAP Oil Exporters |

GCC | Non-GCC Oil Exporters |

MENAP Oil Importers |

CCA Oil Exporters |

CCA Oil Importers | |

| 2014 | 2.7 | 3.7 | 1.5 | 3.0 | 5.2 | 4.7 |

| 2015 | 3.0 | 3.4 | 2.4 | 3.9 | 4.9 | 4.4 |

| 2015 Revision from Oct. 2014 WEO |

-0.9 | -1.0 | -0.7 | 0.0 | -0.8 | -0.4 |

|

Note: | ||||||

Recent Global and Regional Shocks

Lower Oil Prices

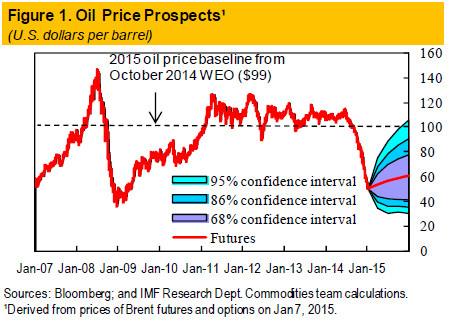

Oil prices have declined by about 55 percent since September 2014, and in late November the Organization of the Petroleum Exporting Countries (OPEC) decided not to cut production. Since then, markets expect oil prices to be around $57 per barrel

on average in 2015 (a decline of about 43 percent from the October 2014 REO baseline) before rising gradually to $72 per barrel by 2019 (about 23 percent lower than projected in the October 2014 REO) (Figure 1). Oil prices are expected to partially recover over the medium term because of the likely decline in investment and future capacity growth in the oil sector in response to lower oil prices.

Prices for other commodities have also declined, though not by as much as oil prices. Metals prices, for example, are now expected to be 13 percent lower in 2015–19 than was projected in the October 2014 REO. Baseline forecasts for average gas prices remain broadly unchanged; however, some gas exporters (Qatar) are facing lower gas prices because their contracts are indexed to oil prices.1

The drop in oil prices is estimated to have been driven by both supply and demand factors: higherthan-expected supply, particularly from the United States, was not offset by production cuts by OPEC members, just as global oil demand (especially from China, Japan, and the euro area) was weakening (see the recent IMF blog post titled Seven Questions About The Recent Oil Price Slump.

Uncertainty surrounding the future path of oil prices is high, pointing to the possibility of short-term volatility. Downside risks stem from the possibility of weaker-than-expected demand growth in key advanced or emerging economies. Upside risks relate to the possibility of supply disruptions – for example, in Iraq – or to a decision by OPEC to cut production. Over the medium term, the outlook for is likely to depend on how oil investment and production respond to lower prices. It will also depend on whether OPEC resumes its role as the swing producer or whether prices will be more strongly influenced by the marginal cost of shale oil production.

Lower oil prices have different implications for oil exporters and importers. A decline in prices results in losses in export and fiscal revenues in oil-exporting countries, with possible knock-on effects on government spending and non-oil economic growth. Oil-importing countries gain from lower oil prices through reduced oil import bills and lower energy subsidy bills. Higher disposable incomes and lower production costs could contribute to the growth of domestic demand.

Weaker Demand

Despite a large decline in oil prices, the IMF forecast of global growth for 2015 has been revised down by 0.3 pp to 3.5 percent (Table 1). The positive impact of lower oil prices on global growth is expected to be more than offset by the negative effects of various cyclical and policy factors. (For more details, see the January 2015 World Economic Outlook Update

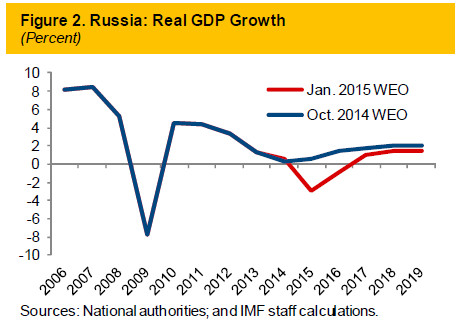

Growth forecasts for the euro area, Japan, and some emerging economies, particularly China and Russia, have been revised down. Russia’s economy is now expected to shrink by 3 percent in 2015, with growth revisions amounting to 3½ pp (Figure 2), because of lower oil prices and increased geopolitical tensions. Forecasts for the euro area have been revised downward by 0.2 pp to 1.2 percent, and for China by 0.3 pp to 6.8 percent. These revisions are owing to both cyclical factors and slower potential growth.

The CCA countries will be affected by Russia’s deepening recession through multiple channels, especially trade, remittances, foreign direct investment (FDI), and risk premiums. A temporary fall of 1 pp in Russia’s GDP growth in a given year is estimated to lower growth in the CCA oil exporters by 0.15 pp and in the CCA oil importers by 0.4 pp in that year. (See Box 3.1 in the October 2014 REO). China’s slowerthan-expected growth will also have negative effects on growth in the CCA. Among the MENAP oil importers, Maghreb 2 countries will face weaker export prospects because of slower-than-expected growth in the euro area, while Mashreq 3 countries could be affected by lower remittances, FDI, and tourism from the GCC.

Declines in prices of other commodities, which some

oil-importing countries in the region export (for example, copper in Armenia, gold in the Kyrgyz Republic, and iron in Mauritania), will offset gains stemming from lower oil import bills (Figure 3).

Higher Interest Rates, Stronger Dollar, and Weaker Ruble

Global interest rate and exchange rate developments,

which are largely driven by the expected

normalization of U.S. monetary policy, also have a

bearing on the regional outlook, albeit to a lesser

extent than declines in commodity prices and

external demand. The expected increase in U.S.

interest rates is likely to tighten financial conditions

in the MENAP and CCA regions, particularly in the

GCC because of their exchange rate pegs, and to

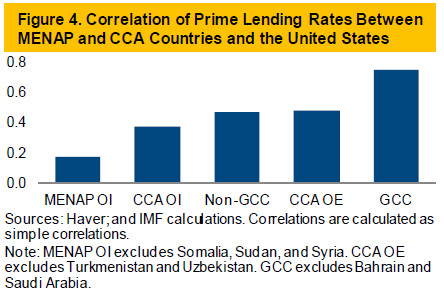

dampen the growth of private credit (Figure 4).

These interest rate spillovers are likely to occur with

a delay because of slow pass-through.

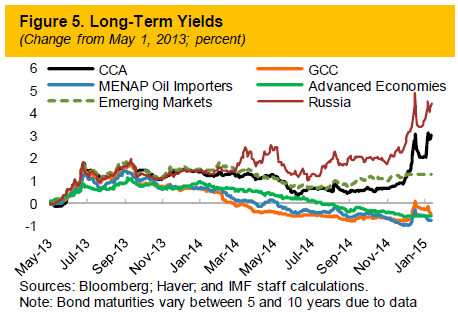

So far, long-term yields in the MENAP oil importers

and the GCC have not been affected much by

concerns about tightening U.S. monetary policy.

Large fiscal and external buffers in the GCC, and declines in MENAP oil importers’ country risk

premiums, resulting from recent progress in reforms,

caused their long-term yields to decline since the

start of the “taper talk” in May 2013, in contrast to

developments in emerging market yields (Figure 5).

CCA long-term yields have recently risen faster than

emerging market trends, in part because of the

region’s exposure to Russia.

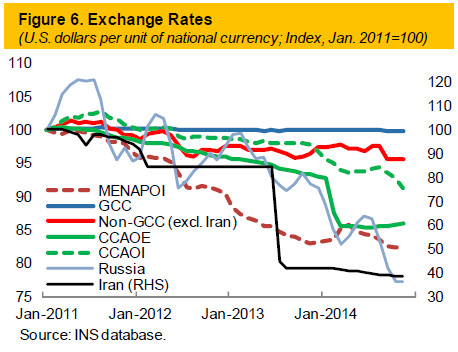

Despite a predominance of dollar pegs in the GCC

and other managed exchange rate regimes in the

MENAP and CCA regions, a number of local

currencies have depreciated against the U.S. dollar

since oil prices started to fall in June 2014 (Figure 6).

In the MENAP region, currencies in Iran, Morocco, and Tunisia depreciated by 6–13 percent against the dollar since last June, with a corresponding reduction in the magnitude of the oil price shock measured in local currency. Currencies of the CCA oil importers (Armenia, Georgia, the Kyrgyz Republic, and Tajikistan) have also come under pressure, in the face of rapid depreciation of the Russian ruble. Among the CCA oil exporters, the Turkmenistani manat was devalued by 23 percent earlier this month, and the Kazakh tenge was devalued by 18 percent last February.

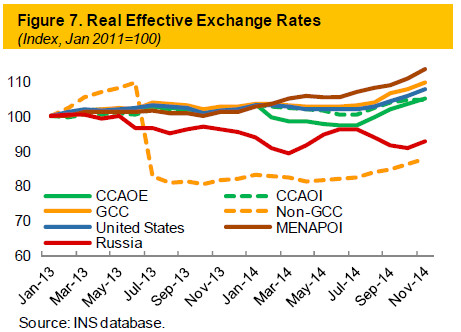

Despite nominal exchange rate depreciations, currencies of MENAP and CCA countries have appreciated in real effective terms since last June (reflecting the weaker euro and sharp depreciation of the Russian ruble), risking to limit prospects for increased exports from these regions (Figure 7).

The sharp depreciation of the ruble has also

depressed the value of remittances from Russia,

which account for a significant share of some CCA

economies (particularly Armenia, the Kyrgyz

Republic, and Tajikistan). In addition, the amounts

of remittances are declining because of the recession

in Russia and, possibly, a declining number of CCA

migrant workers.

Banks Exposed But Resilient

The impact of lower oil prices on oil exporters’

banking systems is likely to be muted in the near

term, but downside risks are likely to increase over

time. Second-round effects of lower oil prices on

economic activity could weaken asset quality,

liquidity, and profitability, but the speed of

adjustment is likely to vary across countries.

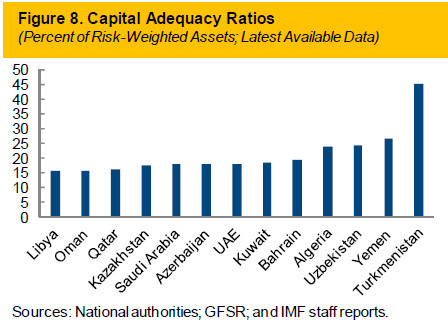

GCC banking systems will be affected by the decline

in oil prices, given the strong correlation between

non-oil growth and government spending, but they

should remain resilient owing to their high capital buffers, low nonperforming loans (NPLs), and

generally high liquidity (Figures 8–9).

Outside the GCC, a source of risk in Algeria’s

banking system is the public banks’ extensive and

direct exposures to large state-owned enterprises in

various industries, which are subject to fiscal strains

as a result of lower oil prices. Yemen is at high risk

because its banks are highly exposed to government

debt against the backdrop of a weak fiscal position

and limited financing options. Selected oil-importing

countries (such as Egypt, Jordan, and Lebanon) for

which remittances are a major source of liquidity

could experience tighter liquidity conditions if

remittances decline.

Banks in the CCA have high capital adequacy ratios and the countries have large financial buffers but banking systems are more vulnerable to shocks because of credit risk and structural vulnerabilities. Some countries (such as Azerbaijan, Kazakhstan, and Tajikistan) are starting from positions of weakness: high NPLs and high dollarization, particularly unhedged borrowing in foreign currency, expose banks to market-induced credit risks, and preclude them from accessing the central banks as lender of last resort. Large spillovers from Russia’s slowdown, lower remittances, and financial distress also heighten credit and liquidity risks.

Overall, high state involvement in the financial sector across the region, and the strong link between the oil and non-oil economies, on the one hand, and fiscal performance, on the other hand, suggest that financial supervisors need to closely monitor financial sector vulnerability to oil price shocks. Likewise, CCA bank supervisors need to be vigilant regarding exposures of their financial sectors to spillovers from Russia’s slowdown and financial market distress.

Conflicts and Security Disruptions

Conflicts, terrorism, and related security disruptions continue to be a prevailing concern in the region. Although airstrikes have slowed the advance of the so-called Islamic State (ISIS), conflicts in Iraq and Syria persist, creating significant economic and political spillovers for neighboring countries (especially Jordan and Lebanon). The security situations in Afghanistan, Libya, Pakistan, and Yemen also remain challenging. Conflicts cast a shadow over the economic outlook for the MENAP region, not only because they disrupt economic activity; they also reduce political space for the much-needed reforms and delay the return of confidence to the MENAP region.

Oil Exporters

Oil exporters in the MENAP and CCA regions are faced with substantial losses in government revenues and exports as a result of the large decline in oil prices. Many countries have significant buffers in the form of foreign assets that will allow them to avoid steep spending cuts and limit the drag on growth. For countries in the CCA, the impact of lower oil prices is compounded by the deepening recession in Russia, to which they are closely linked through trade, remittances, and foreign direct investment (FDI), and by slowing growth in China, another important trading partner. But the consequences for economic growth in these countries will likely be mitigated by countercyclical expenditure policy.

Across both regions, with buffers eroding at varying speeds, most countries will need to re-assess medium-term spending plans and, if lower oil prices persist for a prolonged period, will need to adjust gradually to the new realities in the global oil market. Some countries that do not have significant buffers or borrowing capacity will need to adjust more quickly, with adverse consequences for economic growth. In all oil-exporting countries, deepening economic reforms aimed at diversifying economies away from oil, and encouraging growth and job creation, would help mitigate any adverse effects of fiscal consolidation on growth.

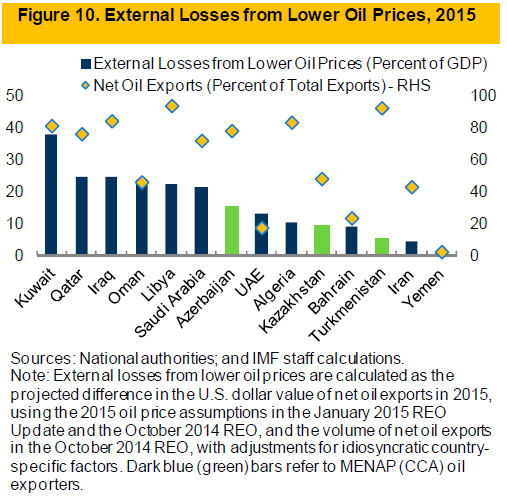

Large Losses for Oil-Dependent Economies

The large decline in oil prices will lead to significant

revenue losses for oil exporters in the MENAP and

CCA regions because most of these economies are

highly dependent on oil. Oil exports account, on

average, for two-thirds of total exports in the

MENAP and CCA oil exporters (Figure 10).

Oil export losses in 2015 are expected to reach about $300 billion or 21 pp of GDP in the GCC, about $90 billion or 10 pp of GDP in the non-GCC, and about $35 billion or 8 pp of GDP in the CCA oil exporters. The countries that will be most affected are Kuwait, Qatar, Iraq, Oman, Libya, and Saudi Arabia.

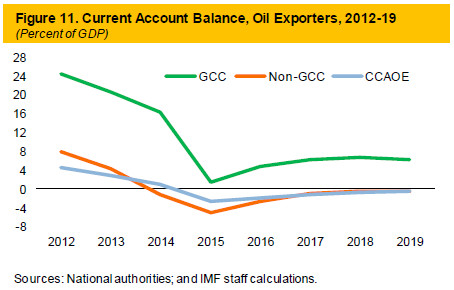

As a result, current account surpluses are projected to

decline this year to 1.6 percent of GDP in the GCC,

while non-GCC oil exporters and CCA oil exporters

will likely post deficits of around 5 percent and 2.7

percent of GDP, respectively (Figure 11).

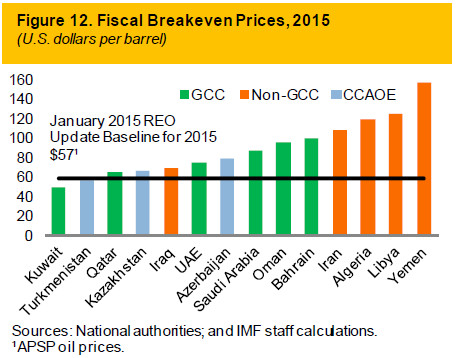

Fiscal revenues will also decline because oil export

revenues are captured almost entirely by

governments in the MENAP and CCA countries. Most oil exporters need oil prices to be considerably

above the $57 projected for 2015 to cover

government spending, which has increased in recent

years in response to rising social pressures and

infrastructure development goals (Figure 12).

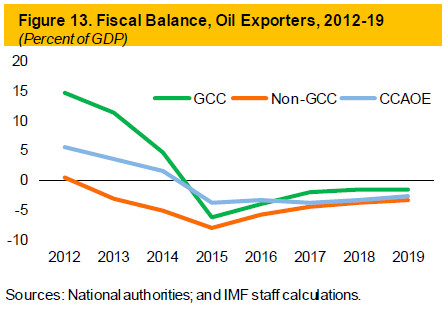

As a result, the oil price decline is expected to

significantly erode fiscal positions across the region

(Figure 13). Except for Kuwait, Turkmenistan, and

Uzbekistan, all countries in the region are expected

to run fiscal deficits in 2015 (Table 2). The GCC

fiscal surplus (4.6 percent of GDP in 2014) is now

projected to turn into a deficit of 6.3 percent of GDP

in 2015; a downward swing of about 11 pp of GDP.

On current policies, and assuming a partial recovery of oil prices in line with futures markets, fiscal balances could gradually improve over the medium term while remaining in deficit in most countries.

Table 2. Fiscal Balances, Oil Exporters | ||

| 2014 | 2015 | |

| GCC | ||

| Bahrain | -5.4 | -12.1 |

| Kuwait | 21.9 | 11.1 |

| Oman | -1.4 | -16.4 |

| Qatar | 9.2 | -1.5 |

| Saudi Arabia | 1.1 | -10.1 |

| United Arab Emirates | 6.0 | -3.7 |

| Non-GCC | ||

| Algeria | -7.4 | -15.1 |

| Iran, Islamic Republic of | -1.4 | -3.4 |

| Iraq | -4.9 | -6.1 |

| Libya | -43.3 | -37.1 |

| Yemen, Republic of | -5.4 | -5.2 |

| CCA | ||

| Azerbaijan | -2.3 | -14.5 |

| Kazakhstan | 3.2 | -2.3 |

| Turkmenistan | 1.4 | 0.0 |

| Uzbekistan | 0.5 | 0.2 |

>3% of GDP >3% of GDP |

0-3% of GDP 0-3% of GDP |

<0% of GDP <0% of GDP |

| Sources: National authorities; and IMF staff estimates. | ||

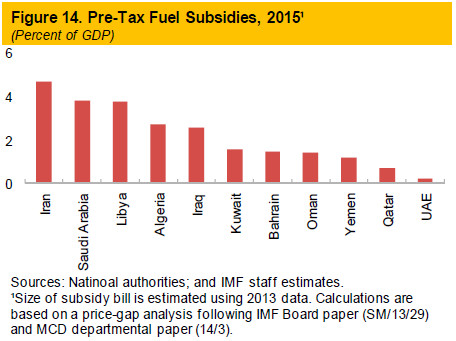

Even after the reduction in oil prices, energy prices

charged to consumers remain well below

international prices in most oil exporters. These

‘energy subsidies’ are not reflected in the budget but

persist as important foregone revenue and as a reason

for the exceptionally fast growth of energy

consumption in these countries (Figure 14).

The new fiscal realities facing most oil exporters make it all the more urgent to begin tackling the underpricing of energy products in oil-exporting countries in both the MENAP and CCA regions.

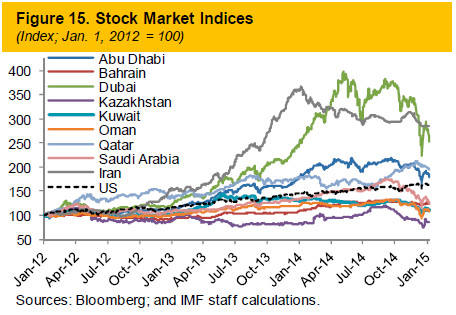

Weaker Stock Markets

Stock markets in a number of countries, including

Iran, Kazakhstan, Kuwait, Saudi Arabia, and the

United Arab Emirates, declined sharply in late 2014

because of rising concerns about how their

economies will be affected by lower oil prices, and

particularly as to whether governments, which have

been key drivers of corporate earnings, would cut

spending in response to lower oil prices (Figure 15).

The decline in equity prices may weigh on

consumption, but the effects should be manageable.

Energy-related firms and banks with large exposures

to the oil sector are facing more difficult refinancing

conditions because lower oil prices are expected to

lower their earnings and creditworthiness. Capital

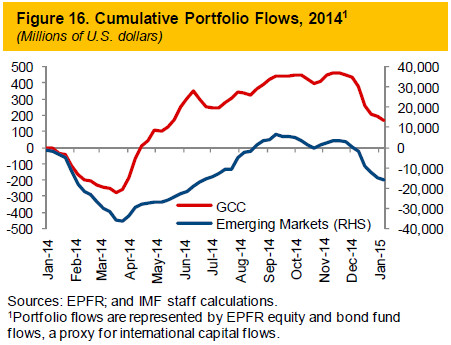

flows to the GCC have also slowed, though they

remain broadly in line with trends for other emerging

markets (Figure 16).

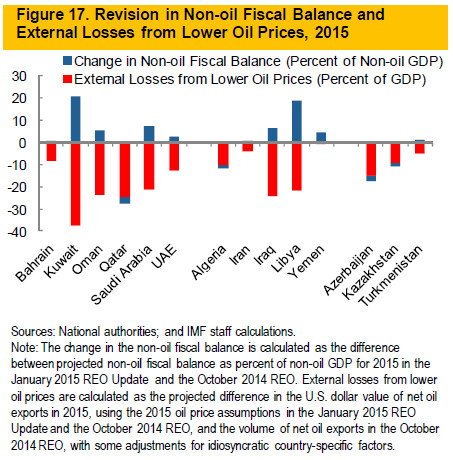

Avoiding Sharp Cuts in Spending

Most oil-exporting countries in the MENAP and

CCA regions have significant fiscal buffers, which

allow them to avoid sudden cuts in spending in

response to declining oil revenues (Table 3).

GCC countries, which are expected to be most

severely affected by the decline in oil prices in terms

of revenue losses, and which generally peg their

currencies to the dollar, have large financial assets and borrowing capacity to help cushion the impact

on near-term growth. Nevertheless, most GCC

countries (except Qatar) are now expected to slow

spending growth in 2015 compared to what was

projected in the October 2014 REO, resulting in a

decline in their non-oil fiscal deficits (Figure 17).

These declines are much smaller than the loss of fiscal revenues, suggesting that countries are using their fiscal buffers.

Table 3. Size of Financial Buffers and Resource Horizons | ||||

| Availability of financial buffers in the short run 1 | Resource horizon (2012) 2 | Gross central government debt (percent of GDP, 2013) 3 | Saving enough for intergenerational equity? 4 | |

| GCC | ||||

| Bahrain | limited | 14 | 43.9 | No |

| Kuwait | Substantial | 122.7 | 3.2 | No |

| Oman | limited | 32.8 | 7.3 | No |

| Qatar | Substantial | 159.6 | 34.3 | No |

| Saudi Arabia | Substantial | 80.1 | 2.7 | No |

| United Arab Emirates | Substantial | 117.9 | 11.7 | No |

| Non-GCC | ||||

| Algeria | Substantial | 55.3 | 9.3 | No |

| Iran, Islamic Republic of | limited | 209.5 | 11.3 | N/A |

| Iraq | limited | 131.9 | 31.3 | No |

| Libya | Substantial | 126.8 | N/A | No |

| Yemen, Republic of | limited | 63.1 | 48.2 | No |

| CCA | ||||

| Azerbaijan | Substantial | 27.8 | 13.8 | No |

| Kazakhstan | Substantial | 65.6 | 12.9 | No |

| Turkmenistan | Substantial | 271.9 | 20.5 | Yes |

| Uzbekistan | Substantial | N/A | 8.5 | N/A |

| 4 years and above | >40 | <40 | Yes | |

| 3 years and below | 20<x<40 | >40 | No | |

| <20 | ||||

|

1 Source: Calculations based on years until public net foreign assets turn negative,

assuming no fiscal adjustment. 2 Source: Ratio of proven reserves to total oil and natural gas production (2012 figures from Annex 3 in Fall 2013 REO). 3 Source: Fall 2014 REO. 4 Source: Figure 1.8 (Fall 2014 REO) and Figure A3.3 (Fall 2013 REO). |

||||

In the GCC, most of the slowdown in spending is expected to affect capital spending. By contrast, current spending, particularly on public wage bills, is unlikely to change significantly, though some countries are reforming their energy subsidies. Reducing subsidies and other current spending would be preferable to reducing capital spending because the former would likely exert a smaller drag on economic growth while addressing fiscal rigidities. Identifying additional sources of non-oil revenue would support efforts to contain spending.

Some CCA oil exporters, faced with the twin shocks of lower oil prices and the deepening recession in Russia, are expected to increase government spending. Azerbaijan and Kazakhstan are expected to use their fiscal buffers and borrowing to provide a fiscal stimulus, leading to some deterioration in their non-oil fiscal balances. By contrast, Turkmenistan and Uzbekistan intend to maintain their earlier spending plans because prices for their gas exports have not been affected by the decline in oil prices. Although fiscal stimulus in response to adverse developments may be appropriate in some cases, countries would be well advised to maintain a cautious approach to fiscal policy, because a prolonged period of lower oil prices would ultimately require significant adjustment in most countries.

Countries with low or inaccessible buffers face more immediate adjustment needs, and some have taken appropriate initial steps in this direction. For example, Yemen, although lower oil prices will have a smaller revenue impact on its economy compared to other oil exporters, is planning to increase non-oil revenue collection, contain the government wage bill, and continue fuel subsidy reform. A large financing gap in Iraq’s 2015 draft budget will force a reduction in current and capital spending. In Libya, fiscal adjustment is occurring through capital spending because of political instability. In Algeria, lower current transfers and additional tax revenues should drive the fiscal adjustment in response to lower oil prices.

Limited Impact on Growth and Inflation over the Near Term

With most MENAP and CCA countries expected to use buffers in response to lower oil revenues in the next two years, the near-term impact of lower oil prices on non-oil growth is likely to be contained. As a result, regional spillovers from major oil-exporting countries, particularly from the GCC to the Mashreq and sub-Saharan Africa, through remittances, non-oil imports, and/or outward investment are generally expected to be limited in the near term. In a few financially constrained MENAP oil exporters (Iran, Iraq, Yemen), growth will likely slow in the next two years. In the CCA oil exporters, growth has been revised downward in the near term because of the larger-than-expected slowdown in Russia.

Overall, we expect growth in the GCC of around 3.4 percent in 2015, a downward revision of 1 percentage point relative to the October 2014 REO.4 In the non-GCC oil exporters, growth is revised down by 0.7 pp in 2015 to 2.4 percent. In the CCA oil exporters, growth is expected at about 4.9 percent this year, 0.8 pp below the October 2014 REO forecast.

The impact of declining oil prices on inflation in MENAP and CCA oil exporters is likely to be subdued because most countries use administered prices for fuel products. Countries with a more flexible exchange rate (for example, Iran) would need to be vigilant and tighten monetary policy if lower oil revenue leads to a sharp depreciation of the exchange rate and higher inflation. CCA countries that are facing simultaneous external shocks can allow more exchange rate flexibility. These countries should maintain adequate foreign exchange buffers so that they can address potential financial stability concerns, and should adjust monetary policy both to address emerging signs of inflation pressures and to limit exchange rate pressures.

Oil production and evolving conflicts in the region constitute important downside risks to the outlook. Regional OPEC oil producers are not expected to cut oil production under baseline projections, but apparent oversupply in the global oil market suggests that the risks for oil production are skewed to the downside. In addition, countries in conflict or difficult security situations (Iraq, Libya, Yemen) or facing a difficult external environment (Iran) could also suffer from declining oil production and/or face downside risks from conflict-induced disruptions in non-oil economic activity. A deeper recession in Russia and a further depreciation of the ruble could have an additional negative impact on non-oil exports from CCA oil exporters.

Need to Adjust and Diversify over the Medium Term

As the decline in oil prices could prove to be persistent, most oil exporters in the region may well need to adjust their fiscal positions to the new realities of the global oil market to ensure that they maintain fiscal sustainability.

The adjustment would need to be anchored by credible medium-term fiscal consolidation plans and would require limiting current spending, including wage and subsidy bills. Although some countries have already initiated subsidy reforms (Azerbaijan, Bahrain, Kuwait, Qatar, Saudi Arabia, Turkmenistan, the United Arab Emirates) or started discussing them (Oman), energy subsidies still remain large in the region. Falling oil prices could make such reforms both more urgent and, possibly, politically easier to implement.

Careful prioritization and appraisal of sizable investment projects would also be important to ensure medium-term growth dividends. Priority projects, including large foreign-financed projects in some CCA countries, should move forward. Countries also need to explore possibilities for diversifying revenue sources, which could include income and value-added taxes.

Accompanying measures that would help limit the adverse impact of fiscal consolidation on the growth of the non-oil economy include deeper reforms to diversify economies away from oil, particularly by improving the business environment, creating incentives for private entrepreneurship in the tradable goods sectors, and increasing private employment of nationals. CCA countries, in particular, should accelerate structural reforms to liberalize their economies, especially reforms to ease business regulation and strengthen competition. Institutional arrangements and transparency for dealing with oil price—driven changes in fiscal revenues also need to be strengthened.

Oil Importers

Oil importers in the MENAP and CCA regions are benefiting from lower oil prices. Energy import bills are reduced and, where lower oil prices are passed on to end-users, production costs decline and disposable income rises.

Yet in most oil-importing countries gains from lower oil prices are offset by other adverse factors, such as slower-than-expected domestic demand growth and a weaker-than-expected outlook for growth in the key trading partner countries: the euro area and GCC, for MENAP oil importers, and Russia and China, for CCA oil importers. In addition, some countries export non-oil commodities, the prices for which have been declining. As a result, the impact on growth and on fiscal and current account deficits is mixed, with expected improvements in some countries but a worsening in others, especially in the CCA countries, which have been strongly affected by a deepening recession in Russia.

Lower oil prices create favorable conditions for continuing subsidy reforms and for stepping up structural reform efforts to support medium-term growth and job creation. However, oil importers should not overestimate the positive impact of the decline in oil prices on their economies: demand growth is weak in trading partner countries and there is considerable uncertainty about the persistence of lower oil prices and the availability of external financing.

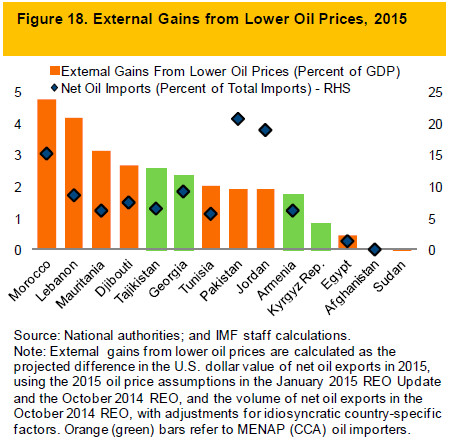

Sizeable Gains in Only a Few Cases

The sharp drop in oil prices has reduced energy

import bills in MENAP oil importers. External gains

from lower oil prices in 2015 are estimated, on

average, at about 1½ pp of GDP in the MENAP and

2 pp of GDP in the CCA (Figure 18).

Countries estimated to gain most from lower oil prices in 2015 are Morocco (about 4¾ pp of GDP), Lebanon (about 4¼ pp of GDP), Mauritania (about 3 pp of GDP), Djibouti and Tajikistan (about 2½ pp of GDP), Georgia (about 2¼ pp of GDP), Jordan, Tunisia and Pakistan (about 2 pp of GDP), and Armenia (about 1¾ pp of GDP).

The windfall gains are generally smaller than oil exporters’ losses because MENAP and CCA oil importers depend much less on oil than oil-exporting countries do (Figure 18). Also, declines in global oil prices are generally transmitted with significant lags to the CCA countries because their oil import prices are typically fixed for periods of several years.

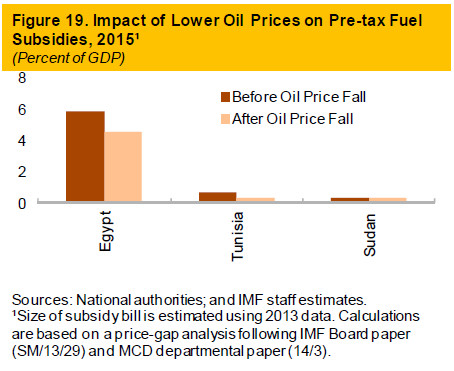

Unless governments choose to lower the pump prices

of petroleum products, lower international oil prices

will also result in fiscal gains through reduced fuel

subsidy bills. These savings are estimated at about

½ pp of GDP for the MENAP oil importers in 2015

(Figure 19). Gains are particularly large in Egypt,

where subsidy bills remain high despite recently

initiated reforms; whether those gains will accrue to

the budget will depend on country-specific arrangements between state oil companies and the

government. CCA oil importers do not subsidize fuel

through government budgets. Their energy subsidies

are not expected to decline because they tend to

depend on gas prices, which are projected to remain

stable in the near term.

Fiscal Policy Responding to Multiple Shocks

Among MENAP countries benefitting most from

lower oil import bills, fiscal balances are expected to

improve (compared to projections in the October

2014 REO) in Lebanon (by 1¾ pp of GDP) and

Egypt (by ½ pp of GDP) (Figure 20).

In other MENAP oil importers, fiscal balances are now projected to be weaker this year than was projected in the October 2014 REO (for example, Djibouti and Tunisia), in part owing to weaker-thanexpected domestic demand growth and scaling-up of public investment. In the Kyrgyz Republic, Russia’s slowdown and large investment projects have led to a 7¼ pp of GDP downward revision in the fiscal balance.

Partially Saving Windfall Gains

Overall, MENAP oil importers are expected to save most of their oil-related windfall gains. Their current account positions are expected to improve by 1 pp of GDP (compared to projections in the October 2014 REO). This improvement is broadly in line with the oil-related windfall gains estimated at about 1½ pp of GDP. MENAP countries do face the risk of a possible decline in remittances, official financing, FDI, and tourism from the GCC countries, albeit over the medium term.

By contrast, current account positions in the CCA oil importers are expected to deteriorate by about 1 pp of GDP from projections made in the October 2014 REO, which compares to about 2 pp of GDP of windfall gains from lower oil prices. The main reason is a significant weakening in external demand from Russia and, to a lesser extent, China. Additional current account pressures arise for countries that export minerals and other commodities (Figure 3) and that recently experienced domestic real currency appreciation (Figure 7).

Limited Impact on Growth and Inflation

The impact of lower oil prices on growth is likely to be limited in the MENAP and CCA oil importers.

First, low pass-through from global oil prices to domestic fuel prices limits the impact on disposable incomes and input costs of firms in MENAP oil importers. The pass-through coefficients in these countries are about 0.4 on average and are much lower for some countries that continue to subsidize domestic fuel prices (Egypt, Tunisia). Pass-through in the CCA oil importers is greater, because of more flexible price-setting mechanisms.

Second, some MENAP and CCA oil importers are facing simultaneous external demand shocks from weaker-than-expected growth in the euro area and Russia, as well as slower-than-expected progress in domestic reforms and delays in return of confidence.

In the CCA oil importers, negative spillovers from Russia overshadow the relief from lower oil prices, leading to a downward revision of growth by ½ pp in 2015 compared to the October 2014 REO, to 4½ percent (Table 1). Downward revisions in Maghreb countries (especially Morocco and Tunisia), which are most affected by spillovers from the euro area, are about 0 to ¾ pp. Mashreq countries (for example, Egypt) are less affected because growth in the GCC countries, to which they are most exposed, is expected to be only modestly weaker. (Growth in Egypt in 2015 has been revised upward by 0.3 pp, in part owing to a strong rebound in Q3 2014.) Overall, MENAP oil importers are expected to grow at 3.9 percent in 2015, unchanged from the October 2014 REO.

In most CCA and MENAP oil importers, lower oil prices are unlikely to have a large direct effect on domestic inflation because of the small share of fuels in the CPI baskets and, in some cases, these effects are offset by subsidy reforms. In some countries (Egypt, Tunisia) domestic fuel prices are subsidized and are not expected to move in line with global prices. In some countries (most CCA oil importers), exchange rate movements are a more important factor influencing inflation.

Over the Medium Term

If lower oil prices prove to be persistent, oil importers will face the question of whether to continue spending or save the windfall gains. It is important not to over-estimate the positive impact of the oil price shock on the oil-importing economies in the region, given weak demand in many of MENAP and CCA’s key trading partners over the medium term. Also, countries should avoid entering into irreversible spending commitments, given the uncertainty about the persistence of the shock and the availability of external financing.

Countries where fiscal sustainability is a concern would be well advised to save the fiscal windfall gains so as to strengthen buffers against adverse cyclical shocks, to free resources for growthenhancing spending, and reduce public debt (especially Egypt, Jordan, Lebanon, and Pakistan). Lower oil prices also create favorable conditions for continuing subsidy reforms accompanied by better targeted social safety nets – especially in countries where subsidies are still high (Egypt, Tunisia) – and for introducing tax reforms (Lebanon). Where weaknesses in demand growth or potential growth are also a concern, countries may consider continuing to use a mixed strategy, allocating a portion of windfall gains toward growth-enhancing investments in infrastructure, health, and education. Windfall changes in fiscal revenues should be managed transparently. All countries need to maintain a focus on fiscal consolidation in the medium term.

External windfall gains should help bolster weak reserve positions across most of the MENAP region and help them create buffers for responding to adverse shocks in the future. In countries where inflation is rising (for example, Tajikistan), monetary policy needs to be tightened further to help limit exchange rate pressures. By contrast, in some cases, increased reserves and low inflation could provide an opportunity to increase exchange rate flexibility (Egypt, Morocco, Pakistan) or reduce policy rates to boost domestic demand. This is particularly important in countries where growth has slowed because of conflicts or other shocks.

Lower oil prices also create an opportunity to step up structural reform efforts, especially in the areas of business environment, governance, education, and trade integration. Visible progress will help boost productivity, create more jobs, and improve living standards and inclusiveness.

MENAP Region: Selected Economic Indicators, 2000–16 | ||||||

| Average | Projections |

|||||

| 2000–11 | 2012 | 2013 | 2014 | 2015 | 2016 | |

| MENAP 1 | ||||||

| Real GDP (annual growth) | 5.3 | 4.6 | 2.2 | 2.8 | 3.3 | 3.9 |

| Current Account Balance | 9.4 | 12.5 | 10.0 | 6.5 | -1.7 | 0.3 |

| Overall Fiscal Balance | 3.3 | 2.8 | 0.1 | -2.4 | -7.0 | -5.0 |

| Inflation, p.a. (annual growth) | 7.2 | 10.1 | 10.0 | 7.0 | 6.5 | 6.4 |

| MENAP oil exporters | ||||||

| Real GDP (annual growth) | 5.6 | 5.4 | 1.9 | 2.7 | 3.0 | 3.7 |

| Current Account Balance | 13.6 | 18.2 | 14.7 | 10.0 | -0.9 | 2.0 |

| Overall Fiscal Balance | 7.5 | 7.8 | 4.6 | 0.1 | -7.1 | -4.8 |

| Inflation, p.a. (annual growth) | 7.3 | 10.5 | 10.4 | 5.9 | 6.1 | 6.2 |

| Of Which: Gulf Cooperation Council | ||||||

| Real GDP (annual growth) | 5.8 | 5.4 | 3.6 | 3.7 | 3.4 | 3.3 |

| Current Account Balance | 16.5 | 24.5 | 20.6 | 16.3 | 1.6 | 4.7 |

| Overall Fiscal Balance | 12.2 | 14.6 | 11.3 | 4.6 | -6.3 | -4.0 |

| Inflation, p.a. (annual growth) | 2.9 | 2.4 | 2.8 | 2.6 | 2.2 | 2.6 |

| MENAP oil importers | ||||||

| Real GDP (annual growth) | 4.7 | 2.9 | 3.0 | 3.0 | 3.9 | 4.5 |

| Current Account Balance | -1.7 | -5.9 | -4.8 | -3.7 | -3.5 | -3.9 |

| Overall Fiscal Balance | -5.1 | -8.4 | -9.5 | -8.0 | -6.9 | -5.5 |

| Inflation, p.a. (annual growth) | 6.9 | 9.4 | 9.2 | 9.5 | 7.4 | 6.7 |

| MENA 1 | ||||||

| Real GDP (annual growth) | 5.4 | 4.6 | 2.1 | 2.6 | 3.2 | 3.8 |

| Current Account Balance | 10.3 | 13.6 | 10.8 | 7.1 | -1.8 | 0.4 |

| Overall Fiscal Balance | 4.2 | 4.1 | 1.1 | -2.2 | -7.4 | -5.2 |

| Inflation, p.a. (annual growth) | 7.1 | 10.1 | 10.4 | 6.8 | 6.6 | 6.5 |

| MENA oil importers | ||||||

| Real GDP (annual growth) | 4.8 | 2.0 | 2.6 | 2.5 | 3.8 | 4.4 |

| Current Account Balance | -2.2 | -7.9 | -6.7 | -5.0 | -4.8 | -5.1 |

| Overall Fiscal Balance | -5.7 | -8.7 | -10.5 | -9.9 | -8.3 | -6.4 |

| Inflation, p.a. (annual growth) | 6.4 | 8.7 | 10.2 | 10.1 | 8.2 | 7.6 |

| Arab countries in transition (excl. Libya) | ||||||

| Real GDP (annual growth) | 4.6 | 2.5 | 2.7 | 2.3 | 3.8 | 4.4 |

| Current Account Balance | -0.7 | -6.1 | -4.6 | -3.1 | -3.6 | -3.9 |

| Overall Fiscal Balance | -5.9 | -9.1 | -11.3 | -10.7 | -8.7 | -6.7 |

| Inflation, p.a. (annual growth) | 6.7 | 6.1 | 7.8 | 7.6 | 7.5 | 7.6 |

Sources: National authorities; and IMF staff calculations and projections. 12011–16 data exclude Syrian Arab Republic. Notes: Data refer to the fiscal year for the follow ing countries: Afghanistan (March 21/March 20) until 2011, and December 21/December 20 thereafter, Iran (March 21/March 20), Qatar (April/March), and Egypt and Pakistan MENAP Oil exporters: Algeria, Bahrain, Iran, Iraq, Kuw ait, Libya, Oman, Qatar, Saudi Arabia, the United Arab Emirates. MENAP Oil importers: Afghanistan, Djibouti, Egypt, Jordan, Lebanon, Mauritania, Morocco, Pakistan, Sudan, Syria, and MENA: MENAP excluding Afghanistan and Pakistan. Arab countries in transition (excl. Libya): Egypt, Jordan, Morocco, Tunisia, and Yemen. |

||||||

CCA Region: Selected Economic Indicators, 2000–16 | ||||||

| Average | Projections |

|||||

| 2000–11 | 2012 | 2013 | 2014 | 2015 | 2016 | |

| CCA | ||||||

| Real GDP (annual growth) | 8.9 | 5.6 | 6.6 | 5.2 | 4.9 | 5.4 |

| Current Account Balance | 1.3 | 3.1 | 1.8 | -0.1 | -3.3 | -2.4 |

| Overall Fiscal Balance | 2.6 | 4.7 | 2.8 | 1.0 | -3.9 | -3.3 |

| Inflation, p.a. (annual growth) | 9.7 | 5.3 | 6.0 | 6.0 | 6.4 | 6.8 |

| CCA oil and gas exporters | ||||||

| Real GDP (annual growth) | 9.3 | 5.6 | 6.8 | 5.2 | 4.9 | 5.5 |

| Current Account Balance | 2.7 | 4.6 | 2.8 | 0.9 | -2.7 | -1.8 |

| Overall Fiscal Balance | 3.4 | 5.5 | 3.4 | 1.4 | -3.9 | -3.3 |

| Inflation, p.a. (annual growth) | 9.9 | 5.7 | 6.3 | 6.2 | 6.2 | 6.9 |

| CCA oil and gas importers | ||||||

| Real GDP (annual growth) | 6.5 | 5.4 | 5.6 | 4.7 | 4.4 | 4.7 |

| Current Account Balance | -8.4 | -10.5 | -7.6 | -9.6 | -8.9 | -8.0 |

| Overall Fiscal Balance | -3.2 | -2.2 | -2.5 | -2.7 | -4.0 | -3.1 |

| Inflation, p.a. (annual growth) | 8.2 | 2.1 | 3.6 | 4.7 | 7.9 | 5.7 |

Sources: National authorities; and IMF staff calculations and projections. CCA oil and gas exporters: Azerbaijan, Kazakhstan, Turkmenistan, and Uzbekistan. CCA oil and gas importers: Armenia, Georgia, the Kyrgyz Republic, and Tajikistan. |

||||||

1 By contrast, in most CCA oil and gas importers, gas prices are fixed in U.S. dollars on multi-year contracts.

2 Maghreb countries: Algeria, Libya, Mauritania, Morocco, and Tunisia.

3 Mashreq countries: Egypt, Jordan, Lebanon, and Syria.

4The Saudi Arabian authorities have released revised real GDP data that update the base year from 1999 to 2010. This rebasing has resulted in a higher share of oil GDP (now 43 percent compared to 21 percent previously) and a lower share of non-oil GDP (57 percent compared to 79 percent previously) in overall GDP. Under the new series, real GDP growth is now estimated at 10 percent, 5.4 percent, and 2.7 percent in 2011, 2012, and 2013, respectively, compared to 8.6 percent, 5.8 percent, and 4 percent previously. For 2014, the preliminary official estimate is that the economy grew by 3.6 percent. This compares to staff’s projection in the October 2014 REO of 4.6 percent growth. If the old (1999 base year) oil and non-oil shares in GDP had been retained, staff estimates the 2014 growth rate would have been around 4.4 percent.