Back t o Basics Compilation | Finance & Development | PDF version

IV. Economics in Action

Inflation Targeting: Holding the Line

Central banks use interest rates to steer price increases toward a publicly announced goal

In recent years, many central banks, the makers of monetary policy, have adopted a technique called inflation targeting to control the general rise in the price level. In this framework, a central bank estimates and makes public a projected, or “target,” inflation rate and then attempts to steer actual inflation toward that target, using such tools as interest rate changes. Because interest rates and inflation rates tend to move in opposite directions, the likely actions a central bank will take to raise or lower interest rates become more transparent under an inflation targeting policy. Advocates of inflation targeting think this leads to increased economic stability.

Why inflation targeting?

In general, a monetary policy framework provides a nominal anchor to the economy. A nominal anchor is a variable policymakers can use to tie down the price level. One nominal anchor central banks used in the past was a currency peg—which linked the value of the domestic currency to the value of the currency of a low-inflation country. But this approach meant that the country’s monetary policy was essentially that of the country to which it pegged, and it constrained the central bank’s ability to respond to such shocks as changes in the terms of trade (the value of a country’s exports relative to that of its imports) or changes in the real interest rate. As a result, many countries began to adopt flexible exchange rates, which forced them to find a new anchor.

Many central banks then began targeting the growth of money supply to control inflation. This approach works if the central bank can control the money supply reasonably well and if money growth is stably related to inflation over time. Ultimately, monetary targeting had limited success because the demand for money became unstable—often because of innovations in the financial markets. As a result, many countries with flexible exchange rates began to target inflation more directly, based on their understanding of the links or “transmission mechanism” from the central bank’s policy instruments (such as interest rates) to inflation.

How does inflation targeting work?

Inflation targeting is straightforward, at least in theory. The central bank forecasts the future path of inflation and compares it with the target inflation rate (the rate the government believes is appropriate for the economy). The difference between the forecast and the target determines how much monetary policy has to be adjusted. Some countries have chosen inflation targets with symmetrical ranges around a midpoint, while others have identified only a target rate or an upper limit to inflation. Most countries have set their inflation targets in the low single digits. A major advantage of inflation targeting is that it combines elements of both “rules” and “discretion” in monetary policy. This “constrained discretion” framework combines two distinct elements: a precise numerical target for inflation in the medium term and a response to economic shocks in the short term.

Rather than focusing on achieving the target at all times, the approach has emphasized achieving the target over the medium term—typically over a two- to three-year horizon. This allows policy to address other objectives—such as smoothing output—over the short term. Thus, inflation targeting provides a rule-like framework within which the central bank has the discretion to react to shocks. Because of inflation targeting’s medium-term focus, policymakers need not feel compelled to do whatever it takes to meet targets on a period-by-period basis.

What is required?

Inflation targeting requires two things. The first is a central bank able to conduct monetary policy with some degree of independence. No central bank can be entirely independent of government influence, but it must be free in choosing the instruments to achieve the rate of inflation that the government deems appropriate. Fiscal policy considerations cannot dictate monetary policy. The second requirement is the willingness and ability of the monetary authorities not to target other indicators, such as wages, the level of employment, or the exchange rate.

Having satisfied these two basic requirements, a country can, in theory, conduct a monetary policy centered on inflation targeting. In practice, the authorities may also take certain preliminary steps:

•Establish explicit quantitative targets for inflation for a specific number of periods ahead.

•Indicate clearly and unambiguously to the public that hitting the inflation target takes precedence over all other objectives of monetary policy.

•Set up a model or methodology for inflation forecasting that uses a number of indicators containing information about future inflation.

•Devise a forward-looking operating procedure through which monetary policy instruments are adjusted (in line with the assessment of future inflation) to hit the chosen target.

Target practitioners?

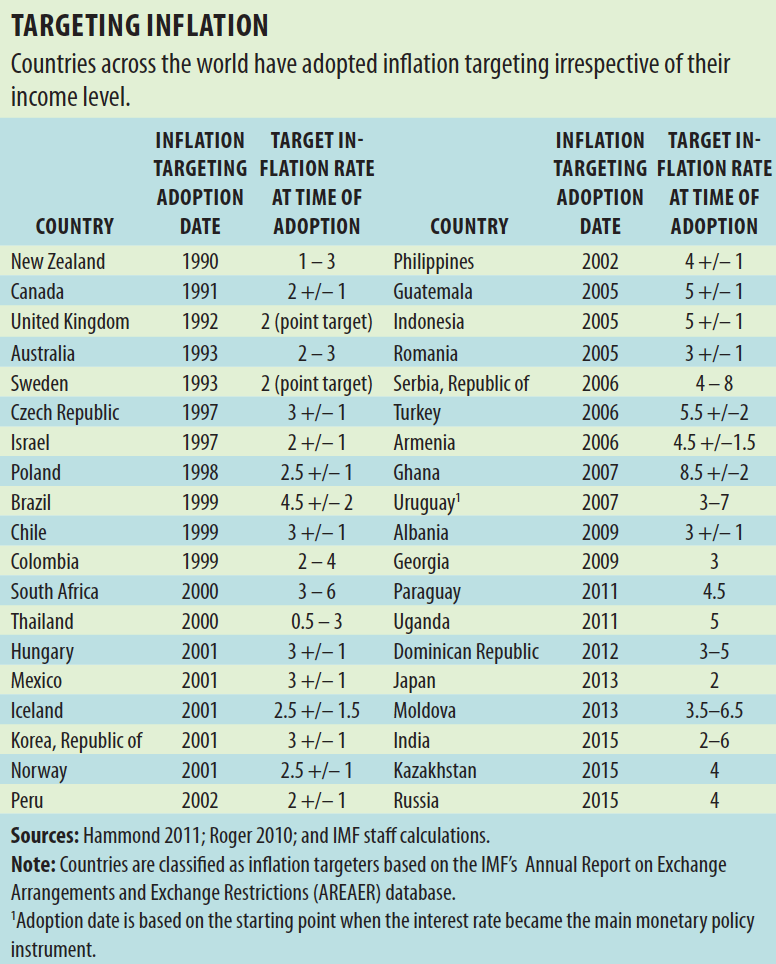

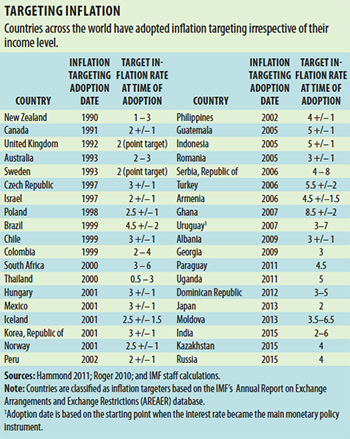

Central banks from advanced, emerging market, and developing economies and from every continent have adopted inflation targeting (see table). Full-fledged inflation targeters are countries that make an explicit commitment to meet a specified inflation rate or range within a specified time frame, regularly announce their targets to the public, and have institutional arrangements to ensure that the central bank is accountable for meeting the target.

{kind=link}

The first country to adopt inflation targeting was New Zealand. The only central banks to have stopped inflation targeting once they started it are Finland, Spain, and the Slovak Republic—in each case after they adopted the euro as their domestic currency. Armenia, the Czech Republic, Hungary, and Poland adopted inflation targeting while they were making the transition from centrally planned to market economies. Several emerging market economies adopted inflation targeting after the 1997 crisis, which forced a number of countries to abandon fixed exchange rate pegs.

There are also a number of central banks in more advanced economies—including the European Central Bank and the US Federal Reserve—that have adopted many of the main elements of inflation targeting but do not officially call themselves inflation targeters. These central banks are committed to achieving low inflation, but some do not announce explicit numerical targets (there are exceptions, such as the United States, which explicitly adopted an inflation target of 2 percent in 2012) or have other objectives, such as promoting maximum employment and moderate long-term interest rates, in addition to stable prices.

On target?

It is difficult to distinguish between the specific impact of inflation targeting and the general impact of more far-reaching concurrent economic reforms. Nonetheless empirical evidence on the performance of inflation targeting is broadly, though not totally, supportive of the effectiveness of the framework in delivering low inflation, anchoring inflation expectations, and lowering inflation volatility. Moreover, these gains in inflation performance were achieved with no adverse effects on output and interest volatility.

Inflation targeters also seem to have been more resilient in turbulent environments. Recent studies have found that in emerging market economies, inflation targeting seems to have been more effective than alternative monetary policy frameworks in anchoring public inflation expectations. In some countries, notably in Latin America, the adoption of inflation targeting was accompanied by better fiscal policies. Often, it has also been accompanied by the enhancement of technical capacity in the central bank and improvement of macroeconomic data. Because inflation targeting also depends to a large extent on the interest rate channel to transmit monetary policy, some emerging market economies also took steps to strengthen and develop the financial sector. Thus, the monetary policy outcomes after the adoption of inflation targeting may reflect improved broader economic, not just monetary, policymaking.

Not a panacea

Inflation targeting has been successfully practiced in a growing number of countries over the past 20 years, and many more countries are moving toward this framework. Over time, inflation targeting has proved to be a flexible framework that has been resilient in changing circumstances, including during the recent global financial crisis. Individual countries, however, must assess their economies to determine whether inflation targeting is appropriate for them or if it can be tailored to suit their needs.

References

Hammond, Gill. 2011. “State of the Art of Inflation Targeting.” Centre for Central Banking Studies Handbook—No. 29. London: Bank of England.

Roger, Scott. 2010. “Inflation Targeting Turns 20.” Finance & Development. March: 46–49.