A new social contract

The original purpose of social protection systems remains: to prevent

poverty, cover catastrophic losses, help households and markets manage

uncertainty, and ultimately provide a foundation for more efficient and

equitable economic outcomes. These objectives motivated the architects of

the "welfare state," as it has come to be known, and should both motivate

and guide efforts to keep social protection systems relevant and

responsive.

New systems are needed that serve the needs of all people, regardless of

how they engage in the market to make a living. These new policies must

also be more adaptable and resilient to dynamic economic, social, and

demographic forces. In other words, a new social contract is needed.

As we examine the changing nature of work (World Bank 2018), we must take a

closer look at how to better protect people and workers in the new economy.

These are some key findings:

Informality, the share of the population not participating in

traditional social insurance and related protections, is currently

about 80 percent of the labor force in developing economies.

This is a major bottleneck to extending protection. Most workers,

especially the poor, are engaged in informal sector activities with little

or no access to social protection. Given the endemic nature of this

challenge and minimal progress against it, most people would be better off

with a social protection system that does not depend on their work

situation.

Social assistance, which contributes to equity in societies, could be

enhanced.

There are several options. At one end of the spectrum is a means-tested

guaranteed minimum income program, which distributes cash to households,

with benefits gradually declining as income rises. At the other end is

universal basic income, with unconditional cash transfers to all,

independent of income or employment. Both are distributed monthly.

An intermediate option is a negative income tax—a way to provide money to

people below a certain income level—with a relatively high threshold and a

gradual withdrawal of benefits. Since a negative income tax is woven into

the tax declaration cycle, it tends to be paid annually. Another such

option could be a smaller guaranteed minimum income supplemented with other

programs, such as universal child allowances and social pensions. The cost

of such an arrangement depends on the level of benefit, scale of coverage,

and shape of the income distribution graph. But increasing robotization

could reduce fiscal constraints, and this type of benefit may become

important for social as well as economic stability.

For informal economies, greater ability to identify individuals and

households and monitor their consumption—if not income—opens new

possibilities at the nexus of universal basic income, negative income tax,

and guaranteed minimum income, or even a negative consumption tax.

Targeting would be based on proxy indicators for unobserved income from

special surveys and identified by linking administrative databases.

The notion of "progressive universalism" (Gentilini 2018) may help

guide expansion in ways that benefit the poor and vulnerable first.

The principle recognizes that universality in itself does not necessarily

make the poorest better-off than existing provisions. Hence, as countries

expand social protection toward universality, the most vulnerable should be

given priority, special attention, and adequate support.

In addition, the global architecture of social protection as set out by

United Nations Sustainable Development Goal 1.3 aims to "implement

nationally appropriate social protection systems and measures for all,

including floors." Similarly, strategic partnerships such as the

International Labour Organization–World Bank Universal Social Protection

Initiative help elevate universality as a strategic goal for countries and

organizations supporting them.

The key issue is the need for a more neutral policy stance than many

governments currently take with respect to the factors of production and to

where and how people work. Once basic protections are guaranteed, people

could upgrade their security with various progressively subsidized

programs—mandatory contributory insurance and savings plans where feasible

and an array of voluntary options where the state and markets can offer

them (Packard and others 2018).

The once politically convenient mingling of social objectives—risk pooling,

poverty elimination, and the pursuit of equality through wealth

redistribution—calls for more explicit distinction and different risk-sharing arrangements

and financing channels. To prevent people from falling into poverty, for

example, the largest and most effective risk pool is a country’s national

budget. Ideally, decisions about financing alternatives would follow

consideration of the appropriate policy instrument to deploy (risk pooling,

saving, or prevention) and the proportionate policy response given what is

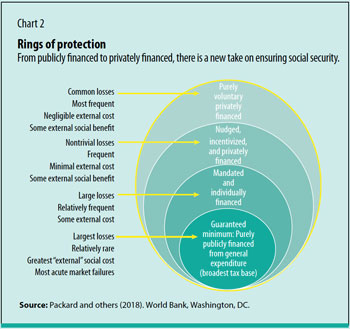

privately available. A stylized package of protection against losses from

livelihood shocks is illustrated in Chart 2.

The innermost core represents the guaranteed minimum support needed to

cover the most catastrophic losses with the greatest social costs—such as

livelihood disruption that plunges families into poverty—for which there

are no viable or effective market alternatives. Ideally, but not always,

these incidents are relatively rare. Interventions to cover more frequently

occurring, lower-loss events—for example, structural churn in the labor

market and retirement—but with obvious and substantial external social

benefits, could be included in this guaranteed minimum support program. In

the three remaining rings, responsibility for financing and provision

gradually shifts away from purely public resources and direct provision to

household or individual financing and market provision.