IMF Lending Case Study: Iceland

May 2019

Iceland was among the first countries hit by the financial tsunami of the global financial crisis. With assets 10 times the size of GDP and relying on aggressive foreign borrowing, Iceland’s banking system was extraordinarily large relative to the economy. When the Icelandic foreign exchange market and banks collapsed, the króna threatened to spiral out of control, dealing a blow to firms and households heavily indebted with foreign currency and inflation-indexed loans.

The IMF was called in, and within 10 days there was an agreement on a set of policy measures. The IMF-supported program of $2.1 billion remains among the largest relative to the size of the economy—18 percent of Iceland’s GDP, or 1,190 percent of Iceland’s quota in the IMF. The support and solidarity of other countries in the region made Iceland an example of the ability of the IMF’s seal of approval to catalyze broad international support.

Iceland took unorthodox measures to overcome the severe crisis. The program featured policies to rebuild confidence in the economy and garner the broadest political support:

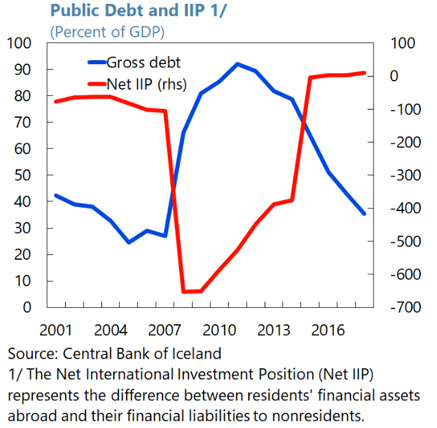

A decade after the crisis outbreak, Iceland has already experienced eight years of robust growth averaging close to 4 percent. The capital controls have largely been lifted, closing an important chapter in the country’s financial crisis saga. Iceland’s current account and budget have remained in surplus for several years. Its gross public debt has declined from 92 percent of GDP at its peak to 35 percent in 2018. Iceland now has more assets abroad than liabilities, a high level of foreign exchange reserves, and banks that are sound and well capitalized.